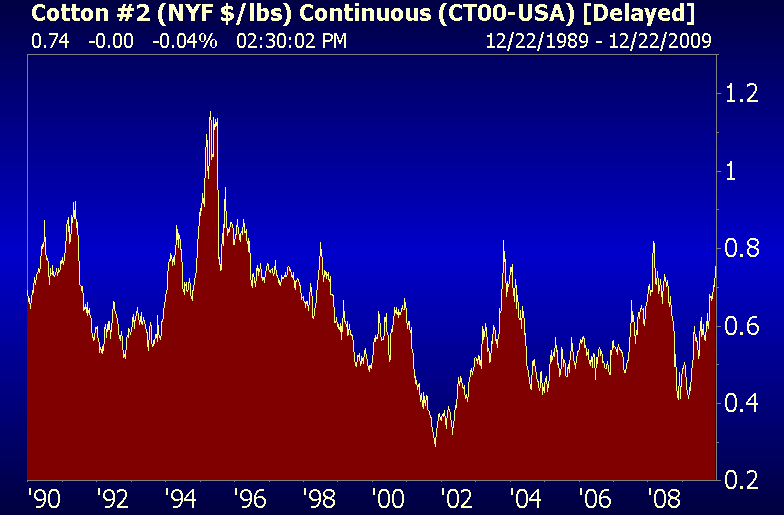

Cotton is back up to $0.76/lb after following the market up from the March 9th lows, though with a more notable 90% move off the bottom. Definitely not a good event for most components of the apparel/footwear supply chain, especially given that petro-based inputs are clocking similar gains. On a combined basis, these two represent roughly 20-25% of the underlying cost of goods sold for most apparel/footwear units at retail. This gets more pronounced as we get closer to the point of origination as opposed to consumption (i.e. it is near 50% of COGS for a wholesaler, and 75% for a bricks, mortar, and sweat manufacturer). We can argue six ways til Sunday about who bears the cost of this, but 1) it won't be the consumer, and 2) the fact is that it is a suck of capital out of the supply chain.

Here's Keith's take on cotton prices based his factor models.

KM: In my model I have the DJ UBS cotton index and the BAL (ipath etf)… BAL literally just broke its TRADE line at 36.40; bullish TREND line all the way down at $34.39… looks like a lot of the emerging markets actually.

Earlier today someone pointed to a 10-year chart and made the case as to how unlikely it was that we breach new highs (implying that the ride is over). I wonder if people made that case in the early 1990s before cotton raced up to a $1.15 peak? Something to watch as the year draws to a close.