Below are analyst updates on our thirteen current high-conviction long and short ideas. We will send Hedgeye CEO Keith McCullough's refreshed levels for each in a separate email.

Please note we removed the U.S. Dollar (UUP) and Red Robin (RRGB) from the long side and added Cerner (CERN) to the short side of Investing Ideas this week.

IDEAS UPDATES

EXAS

Click here to read our analyst's original report.

We recently updated our Exact Sciences (EXAS) Cologuard-Tracker that monitors the number of providers prescribing Cologuard on a monthly basis, which is a key driver in our model. As of the beginning of June, our tracker is projecting more than 11K sequential provider adds in 2Q17 which translates into ~$51.5M in sales compared to consensus of $49.6M. Google Trends activity for Cologuard in the U.S. supports our tracker, projecting greater than 11K provider adds in the quarter. Additionally, we believe Cologuard's test per provider ratio and average selling price (ASP) will continue their upward trajectory, providing additional leverage to the business model as the benefits of guideline inclusions and commercial coverage decisions materialize. Lastly, we expect repeat test orders to drive increased test volume in the back half of 2017, with more meaningful upside in 2018.

We continue to see upside from here as short interest remains elevated at 22.5% and our sales numbers are above consensus' for the remainder of 2017.

TWX

Click here to read our original analysis on why we think the AT&T/Time Warner (TWX) deal will be approved. Below is the most recent update from Telecom & Media Policy analyst Paul Glenchur:

Earlier this week, in a letter to Attorney General Jeff Sessions, a handful of Senate Democrats attacked the AT&T-Time Warner (T-TWX) deal. Criticism of the deal from the likes of Senators Al Franken, Elizabeth Warren and Bernie Sanders should be expected. But leading Senate Judiciary Democrats did not sign the letter, suggesting that industry opponents of the deal are struggling to establish momentum in their efforts to derail the transaction.

The substance of the letter raises nothing new. It trots out the standard complaints that AT&T will favor Time Warner content across its various distribution platforms and discriminate against unaffiliated programming. It discusses net neutrality concerns and possible negative impacts on over-the-top online video providers if Time Warner content is withheld from these emerging yet "fragile" competitors. It also complains that compliance with deal conditions is difficult to monitor and enforce.

Although deal opponents hope this new round of criticism will stir things up, we believe the letter will be discounted as a conventional political attack with little to no impact on Justice Department deliberations.

Initially, Capitol Hill input is largely ignored by antitrust enforcers. They understand lawmaker letters that criticize or oppose deals mostly issue for political reasons and at the request of key constituents, adding very little to the core antitrust analysis of a particular merger.

WMT

Click here to read our analyst's original report.

No update on Wal-Mart (WMT) for this week's Investing Ideas but Hedgeye Retail analyst Brian McGough reiterates his long call on the company.

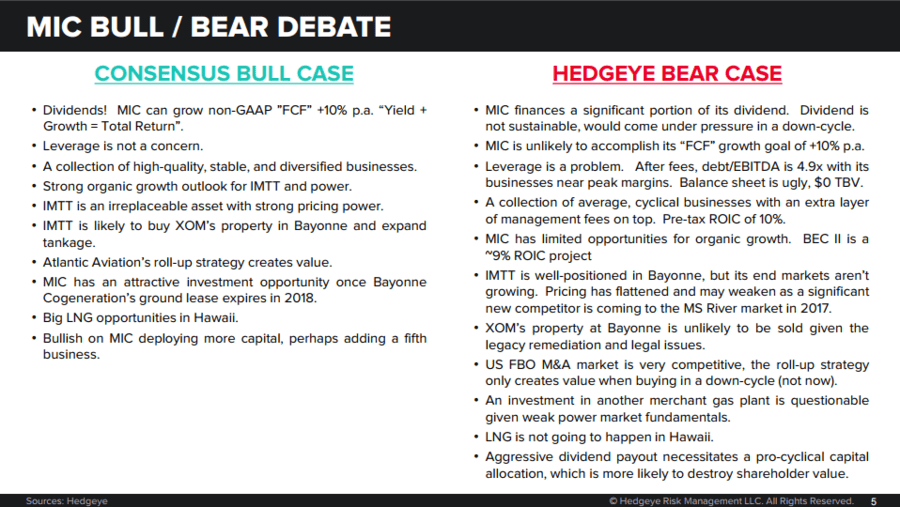

MIC

Click here to read our analyst's original report.

This slide below lays out the bull-bear debate on Macquarie Infrastructure (MIC). We continue to believe we're on the right side of this one.

RLGY

Click here to read our analyst's original report.

Below is an update on the U.S. housing market and Realogy (RLGY) from our Housing team:

The NAR reported that Existing Home sales for May increased +1.1% M/M (consensus estimate was -0.4%) and accelerated to +2.7% YoY as demand reflated back towards cycle highs at 5.62 MM units SAAR. On an NSA basis, volume increased +24.2% M/M, marking the largest sequential May increase in the history of the series.

The inventory of existing homes for sale continues to be tight (1.92mn units, 4.19 months of supply) and this is one of the factors that is driving home price appreciation upwards.

In fact, the median home price increased across all four census regions in May. The Midwestern region increased +7.3% Y/Y to $203.9K, the Western region increased +6.9% Y/Y to $368.8K, the Southern region increased +5.3% Y/Y to $221.9K, and the Northeastern region increased +4.7% Y/Y to $281.3K.

DE

Click here to read our analyst's original report.

Below is an excerpt from an institutional research note written by our Industrials team on Deere (DE):

Margins Did Stabilize TTM, Improve In F2Q17 Quarter: The short view faces a challenge from one bit data in the 10-Q, namely U.S. & Canada operating margin improvement. The Equipment operations generated operating profit of, conveniently, ~$1,111. The pre-tax SiteOne gain was $176 mil, taking the adjusted Equipment operating profit to ~$935. Profit outside of the U.S. and Canada drove most of the profit gain, but even backing this out, home court operating income gained from $457 mil to $545 mil on lower revenue. That’s good for ~250bps of margin expansion. Not bad, but also pretty small and likely unsustainable.

GEL

Click here to to read our analyst's original report.

Hedgeye Energy analyst Kevin Kaiser produced this slide on Genesis Energy (GEL) when he first rolled out his short call in October of 2015 but the GEL short thesis still holds. Check out the bulls versus bears debate. We continue to think we're on the right side of this one.

SNAP

Click here to read our analyst's original report.

Hedgeye Internet & Media analyst Hesham Shaaban recently presented Top Short Idea Snap (SNAP) highlighting his view that the company will underperform expectations through 1H 2018. Shaaban is now more confident that consensus is overshooting the positive in the story – SNAP’s near-term revenue growth prospects.

We think SNAP has already captured the low hanging fruit with high penetration of the younger demographics in NA/Europe and incremental penetration that will be tougher to come by given technological hurdles internationally and a much older remaining total addressable market (TAM). User adoption is slowing domestically, and the monetization story, while potentially interesting, is not nearly as much as the highly-touted ARPU differential b/w SNAP and FB would suggest.

The reason why FB's ARPU is multiples higher is because Instragram revenues are included and its users are considerably more engaged that SNAP users (4x hours on avg.), however we think domestic Rev/User Hour is the better benchmark to assess monetization potential where the FB – SNAP gap at 2.5x is not as wide. Closing that delta will take some time since SNAP's reported usage metrics suggest its users live on the left side of the app, which creates fewer monetization opportunities.

Consensus is expecting SNAP’s growth to nearly double by 3Q17; a level of growth TWTR has never pulled off despite greater scale and overly aggressive monetization tactics. Meanwhile, current 2018 expectations implies SNAP closes this monetization gap and our concern is that it’s anchored on banker reports since the company has yet to provide guidance. We think long-term revenue prospects are limited given the headwinds facing SNAP’s Daily Avg.

CAKE

Click here to read our analyst's original report.

“I think that you can identify specific situations if it were weather or construction. But that, the mall traffic for us in A-locations, and most instances, is still doing very strong,” (Matthew Clark, SVP of Finance and Strategy, 1Q17 Earnings Call)

Well there you have it…straight from the horse’s mouth.

Approximately one month after repeatedly stating that they are seeing absolutely no effects at Cheesecake Factory (CAKE) units, as it relates to slowing mall traffic, CAKE pre-announced a significant same-store sales miss this morning for 2Q17 (-1% vs Consensus Metrix +1.6%). With the stock down ~10% in morning trading, it is clear that many were taking the management team at their word, especially given how they repeatedly pushed back when questioned on the effects of mall traffic on their 1Q17 earnings call. As we have harped on before, CAKE has seen declining traffic for 17 of the last 18 quarters, and on a two-year stack basis, traffic has been down 13 of the last 14 quarters.

RRR

Click here to read our analyst's original report.

We think the Las Vegas locals market could be the best performing casino market in the country over the next 3-5 years. We are starting to see what appears to be somewhat of a locals renaissance. This bodes well for Red Rock Resorts (RRR) which derives most of its EBITDA in the LV locals market. Add in a potential value creating real estate transaction, and this 2018 and beyond story is quite compelling.

KATE

No update on Kate Spade (KATE) for this week’s Investing Ideas but Hedgeye Retail analyst Brian McGough reiterates his long call on the company.

TSLA

Our Industrials team recently presented New Top Short Tesla (TSLA) after stalking the name for quite some time. Sentiment on TSLA is overwhelmingly positive at a time where we see significant roadblocks to success.

There is a ‘First Loser Disadvantage’ wherein late entrants to EVs will still be eligible for federal tax credits, placing TSLA at a disadvantage to new products from powerful competitors. Credit expiration should start to impact orders going forward.

TSLA has even introduced discount credits in addition to existing tax credits, suggesting slack demand for the S and X models even with little current competition. Further consider the sample of success – there are high barriers to entry in autos with zero new US automakers in decades, zero new capital equipment companies in established markets, zero product introductions without problems expect ‘growing pains,’ and zero experience in non-luxury.

We also see a number of near-term catalysts:

- Model S sales have slowed (maybe X too);

- Story stocks tend to underperform as perfect story converts to messy reality;

- The tax credit is dropping to $3,750 for US orders; and

- The reflexive challenge of a share price decline.

Tesla’s narrative is not positioned for downshift in growth outlook – and we see these catalysts starting right away. Orders are likely to reflect Tesla’s changed circumstance in 2H17, with entry likely to be fairly continuous. TSLA faces a minefield of downside catalysts over the next 4 to 8 quarters as it emerges from a period of comparative stability.

If Tesla even survives to profitability, it would be an exceptional accomplishment.

CERN

"Part of being prudent, from a short selling perspective, is understanding the macro market setup," McCullough writes. "You can have the best "bottom-up" analysis of a company in the world. Unless you have a company specific immediate-term catalyst, macro market timing matters, big time. After a massive ramp for Healthcare stocks this week, we're presented with much better entry points for our Best SELL Ideas in the space. One of those ideas is Cerner (CERN)."

Hedgeye Healthcare Sector Head Tom Tobin and Analyst Andrew Freedman held a conference call on the company this week with the following summary:

"We remain convinced Cerner will not be able to grow new client bookings (~30% of total bookings) over a multi-year duration due to a saturated EHR market with limited replacement opportunity. Cerner's inability to grow new client bookings has materially negative implications for their licensed software and services model where 80% of same contract revenue can disappear after year 3 of an installation and the associated capital payments. With new client bookings down in 2016 for the first time in a decade and revenue from strong 2015 bookings rolling off, we expect Cerner's revenue trajectory to face mounting downward pressure from 2018-2020."