MARKET WATCH: What’s Happening? Policymakers are exploring the possibility of introducing “ultra-long” Treasury bonds. The potential benefits are vast. On the sell side, ultra-long bonds would allow the government to lock in low interest outlays for decades and to fund infrastructure with ankle-high hurdle rates. On the buy side, these debt instruments would enable institutional investors to match their long-term liabilities with long-term assets.

Our Take: Despite concerns about soft demand, ultra-long bonds may soon become a reality. With Boomers promising to further strain a federal budget already overburdened by entitlements, introducing long-term debt may be a smart “de-risking” strategy to help get us through the next few decades.

The U.S. Treasury Department prides itself for never allowing transient market conditions to dictate its borrowing habits. But a growing number of policy leaders, led by Treasury Secretary Steve Mnuchin (himself a former bond trader), argue that now is the time to try something new. It may be time, they say, to start issuing an “ultra-long” bond—defined as a bond with a maturity of greater than 30 years.

The drumbeat for ultra-long bonds began shortly after Election Day, when Mnuchin said that the new administration would look at extending the maturity on U.S. debt. Currently, the average maturity of all active U.S. government-issued bonds sits at just 4.6 years, meaning that in 2022, roughly half of this debt will have to be “rolled over” at new (and—gulp!—possibly higher) interest rates.

Then in April the Treasury Department asked primary bond dealers to assess the potential demand, pricing, and market for 40-, 50-, and 100-year bonds. More recently, department officials said that Mnuchin had set up an internal working group to explore the idea further.

Clearly, an ultra-long bond blueprint has been simmering just beneath the surface, even while the White House and Treasury continue to labor over health care and tax reform.

THE PROS OF ULTRA-LONG BONDS

So what exactly would an ultra-long bond accomplish? Why might this new Treasury innovation make sense?

Locking in low rates would shield U.S. taxpayers. The easiest argument in favor of ultra-long bonds is an extension of the argument for selling more of the 10- and 30-year bonds that we already issue—namely, that long-term rates are now so low that we can get a super deal for U.S. taxpayers by locking them in.

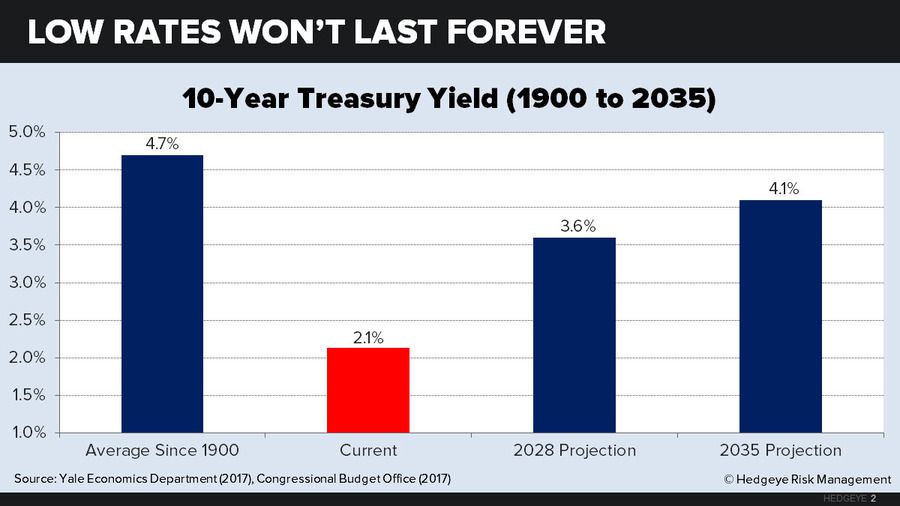

Consider first that the current 10-year Treasury yield is around 2.1%. Then consider that the average 10-year yield over the entire history of the United States (since 1790) has been around 5%—and much of that coincided with gold-standard protection against inflation. Since 1900, the average has been just a shade lower, at 4.7%.

It’s clear that today’s bargain-bin rates are not the historical norm. Nor will they likely stay this low for long: Looking ahead, the CBO’s latest projections forecast the 10-year yield to go back up to 3.6% by 2028 and 4.1% by 2035.

So from this perspective, borrowing heavily at today’s low rates—and locking them in for as long as possible—seems like a no brainer. Extending the average maturity on U.S. debt would safeguard taxpayers. Mnuchin himself hinted at this line of thinking when he explained his reasoning for wanting to pursue an ultra-long agenda: “[E]ventually we are going to have higher interest rates, and that’s something that this country is going to need to deal with.”

Locking in low rates may even be self-validating. To help the taxpayer by assuming long-term rates will rise is, as traders would say, a directional bet on the market. Betting against the market is always iffy. But there may be another, less-risky argument in favor of ultra-longs.

By locking in the interest cost on a significant share of the federal debt, the Treasury could ensure the stability of interest outlays even in the event of a future crisis that sends short-term rates soaring. This insurance could itself “de-risk” the national debt and bring down long-term rates.

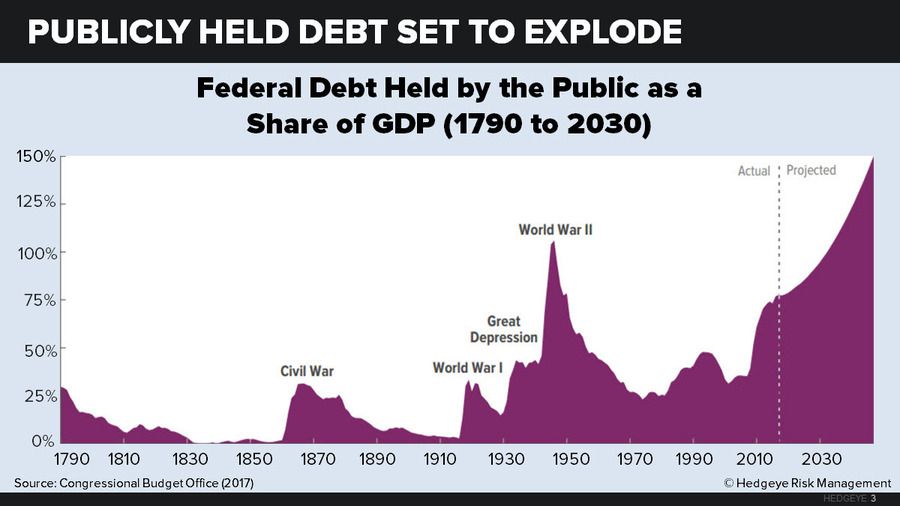

And yes, the possibility of fiscal crisis may soon spook the market. Here we should keep in mind another CBO projection: By 2047, U.S. public-held debt is expected to grow six-fold (from $14 trillion to $87 trillion), rising to a staggering 150% of GDP. This rise is driven almost entirely by population aging. It incorporates fairly optimistic productivity assumptions. And it does not include any tax-cut magic figured in by GOP House leaders or by OMB director Mick Mulvaney. It is, in other words, a best-case scenario.

The federal government could match its long-term liabilities with long-term assets. Still another argument in favor of ultra-longs derives from an old axiom of financial theory: You can always maximize efficiency and minimize cost by matching the duration of assets and liabilities. On the public side, the federal government doesn’t currently have many tangible assets with a known duration. But it is considering investing a lot in such assets in the near future. American voters favor a Marshall-plan size effort to repair and expand America’s infrastructure, and the three most popular presidential candidates in 2016—Trump above all—emphatically agreed.

Bottom line: A low-yielding 100-year Treasury bond might be an ideal way to fund a 100-year bridge or harbor. And Trump suggests there are about $1 trillion of such bridges and harbors. In a recent interview with CNBC, economic advisor Gary Cohn himself acknowledged that low interest rates provide an “enormous opportunity” to fund infrastructure using long-term bonds.

A couple of roadblocks here: For one, Cohn’s comments clash with the administration’s plan to encourage private-sector spending on infrastructure using tax incentives. And the share of the budget devoted to infrastructure may be significantly smaller than the $1 trillion figure that Trump has repeatedly quoted. The president’s preliminary budget proposes just $200 billion in new infrastructure outlays—and may even neutralize these with offsetting cuts to Amtrak, highways, and the Army Corps of Engineers.

So let’s just say that ultra longs make new infrastructure possible at lower cost and leave it at that.

The private sector could match its long-term liabilities with long-term assets. On the private side, there is an even larger demand for long-term duration matching. Many institutional investors, especially life insurers and pension plans, have a fiduciary responsibility to match their large 40- and 50-year liabilities with equivalent assets. The fact that they currently can’t do so traps them in a perverse rollover cycle of buying more shorter-term bonds as their yields fall (even as their prices rise) to sustain yields in out years.

This problem is particularly acute in Europe, where insurance companies make up 40% of the region’s total sovereign long bond purchases—and need to purchase more even when the yields go sub-zero. (The share of U.S. Treasuries held by U.S. insurers is much lower, around 12%, since these bonds are coveted by investors across the globe.)

The issue: Where to find a risk-free 40- or 50-year asset? The solution: The U.S. Treasury creates one. The need is especially acute today when so many firms are terminating their defined-benefit plans and trying to “de-risk” their remaining liabilities (sometimes by paying an insurance company to take them over). But without a risk-free ultra-long bond, there’s always out-year interest-rate risk. Many private investors would pay a premium to shed that risk.

It bears mentioning that most state and local pensions probably won’t be clamoring for more long-term debt anytime soon. Why? Like life insurers and company pensions, these pensions have long-term liabilities that should be matched with long-term assets. But most state and local plans face such massive shortfalls that no such matching is possible—at any conceivable yield. Every single state pension is underfunded by at least $19,000 per household, and many of the nation’s worst-off plans face the prospect of either gutting payouts or going insolvent. In fact, many pension plans are moving to ever-riskier and shorter-term asset classes (including leveraged equity funds) in an attempt to make up lost ground. (See: “America’s Pension Battle Heats Up.”)

THE CONS OF ULTRA-LONG BONDS

To be sure, ultra-long bonds pose risks.

The most obvious risk is that issuing more long-term debt would push up the long end of the yield curve. And that gives many economists pause. After all, if it was quantitative easing that pulled us out of recession, do we really want to reverse the flow and engage in “quantitative tightening”? Or, if you want to go back to an older Fed policy tradition (inaugurated back in the early 1960s when Chubby Checker led the hit parade), if an “operation twist” stimulates the economy by flattening the yield curve, do we really want an “operation untwist” that steepens it?

The second-biggest topic discussed at the Federal Reserve these days (right behind the timing of hiking the fed funds rate) is how and when the Fed will begin offloading its balance sheet back to the public. Is there truly enough demand out there for new long and ultra-long debt instruments such that the U.S. Treasury could sizably reduce its interest-rate risk—without burdening the global economy with higher long-term rates?

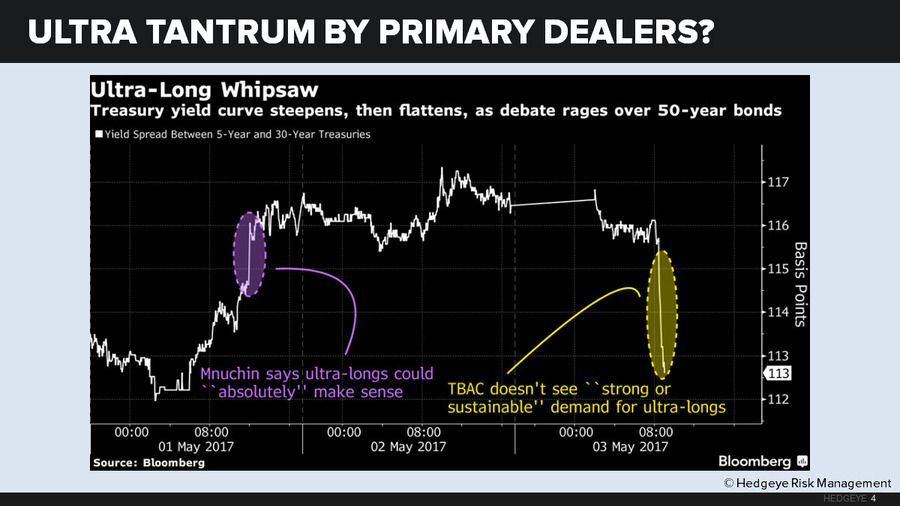

Organizations from Credit Suisse to the Treasury Borrowing Advisory Committee (TBAC) say no, there probably isn’t. The TBAC, dominated by primary dealers who probably don’t want the hassle and risk of handling a whole new instrument type, cautions that the investor demand is not sufficient to justify ultra longs in any large quantity. As if to underline their point, the 30-year to 5-year spread widened on May 1 after Mnuchin voiced his support for ultras and then shrank on May 3 after the TBAC debunked the idea.

Are dealers just being peevish? Possibly.

Keep in mind that steepening the long end of the yield curve in tandem with short-term hikes is in fact the primary purpose of unwinding the Fed’s balance sheet. If the Fed chooses to stall on one, it could choose to stall on the other. Alternatively, the Fed could work with Treasury to slow its unwinding to the extent that ultra longs begin to grow the average maturity of publicly held federal debt.

It is often suggested that investors may fear the long duration of ultra longs, which makes them highly sensitive to interest moves. True, but these ultras would also feature great positive convexity, which means their upside (as rates fall) would exceed their downside (as rates rise).

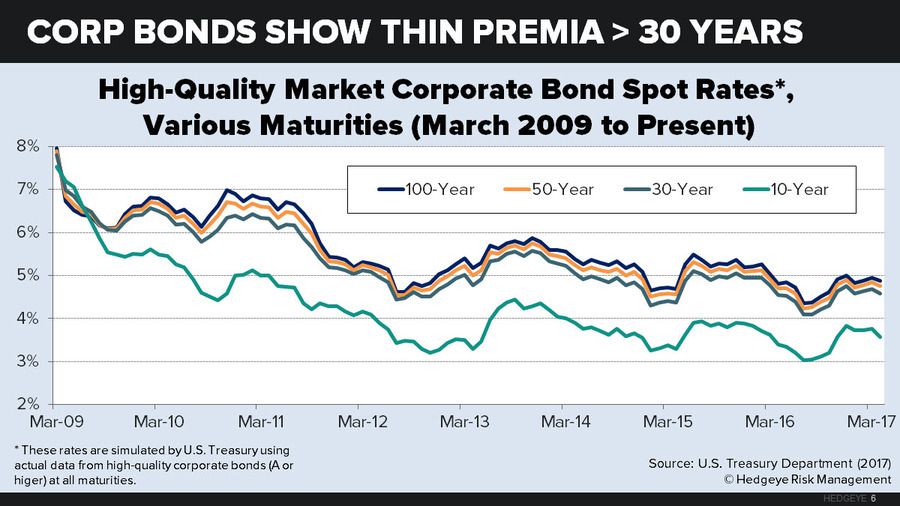

The TBAC cautions that the global volume of ultras is too small to give any assurance that a large Treasury issue would succeed. True again, but to the extent that we have any U.S. data on private-sector ultras, they currently show very thin premia over 30 years. At the very least, it suggests that a deep demand may appear.

ZOOMING OUT ON ULTRA-LONGS

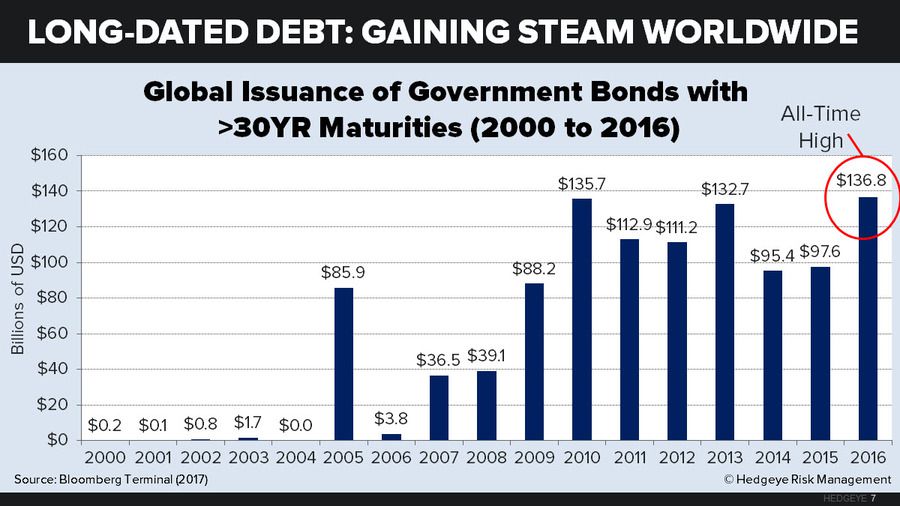

In any case, the United States is not alone in exploring the benefits of ultra-longs. We are in fact late to the party. The total value of sovereign bonds issued worldwide with maturities longer than 30 years has spiked since the Great Recession, hitting an all-time high of $137 billion in 2016.

Nations that have started issuing a 50-year bond in recent years include Canada (with a 3.0% yield), Italy (2.9%), Britain (2.6%), and France (1.9%). Meanwhile, Mexico (4.2%), Ireland (2.4%), and Belgium (2.3%) have issued 100-year bonds. Mexico, perhaps hearing some murmuring about the long-term stability of the peso, denominated its bonds in euros—which is reassuring, depending on what you think the odds are that people will even remember the euro by the year 2115!

Of all these nations, Britain stands out as the undisputed ultra-long champion. The average maturity of active British government-issued bonds stands at a whopping 13.4 years, far above the rest of the developed world, likely due to the rising amount of negative-yielding Eurozone debt that has investors scrambling to find yield. So while the U.S. today stands on the low side of debt maturity, Britain stands on the high side.

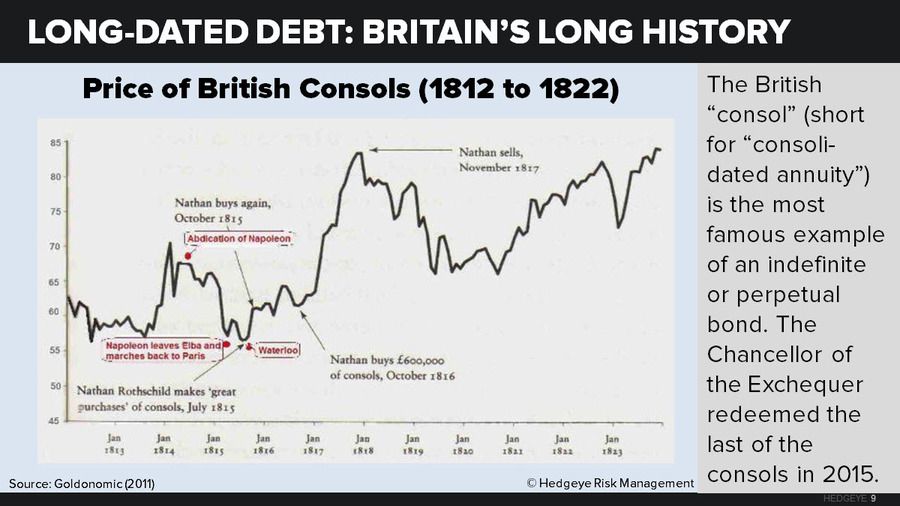

Britain, in fact, is one of the few countries with a history of issuing bonds (known as “perpetuals” or “consoles”) that have no maturity date at all—i.e., infinite-maturity bonds. Britain recently redeemed the consoles that financed the Napoleonic Wars. Indeed, until World War I, Britain—the world’s preeminent financial center—issued little public debt other than consoles.

The consol in practice behaves very much like other ultra-long bonds in that nearly all of its present value resides in the coupons. After all, at a 4% discount rate, 86% of the par value is wiped out after 50 years and 98% after 100 years. After that, going from 100 to 1,000 or to infinity—that is, to 100%—hardly matters.

Most investors have heard the famous “buy the rumor, sell the story” stories about how Nathan Rothschild made a fortune for his family just before and after Waterloo. What was he buying and selling? That’s right: British consoles.

Clearly, plenty of countries have concluded that ultra-longs are worth it.

Likewise, some corporate mainstays within the United States have experimented with ultra-long bonds. Norfolk Southern issued a 100-year “century bond” back in 2011, and is the last company to do so. Other railroads have floated century bonds in the past, including Illinois Central (in 1996) and Northern Pacific (in 1947). (Historically, there are a few U.S. railroads that have issued 1,000-year bonds.)

In fact, big names such as Motorola, Federal Express, Ford, Caterpillar, and JC Penney all went ultra-long with a 100-year bond back in 1997—while Coca-Cola and Walt Disney did so in 1993.

WHAT THE FUTURE HOLDS

Though much of Wall Street remains skeptical of ultra-long bonds, the tailwinds pushing them forward may be irresistible. If they do come to fruition, which duration is the most likely?

We would argue that a 50-year note makes the most sense. Government officials may be hesitant to introduce a 40-year bond that could easily cannibalize demand for 30-year Treasuries, which constitutes the current gold standard for long-term debt. Even the TBAC agrees that a 50-year zero coupon could get some real traction.

A 100-year bond, on the other hand, veers the widest from the Treasury Department’s pattern of “regular and predictable” issuance. It also greatly exceeds the duration needed by most private buyers. Or, at the very least, it will be demanded mostly by institutions that have no intention of buying and selling—raising liquidity issues and possibly giving rise to unpredictable price fluctuations.

It’s important to remember that the government’s pursuit of ultra-long bonds is not simply a response to favorable macroeconomic conditions. History teaches us that governments turn to longer-term debt instruments not just when interest rates are currently low, but also when they face massive upcoming liabilities.

When prospects are sunnier, governments tend to shed their longer-term debt. In fact, one of the reasons why the U.S. Treasury discontinued the 30-year bond back in 2002 (before restarting it in 2006) was because policymakers didn’t see any big liabilities on the horizon. (They must have missed the massive Boomer cohorts bearing down on them.)

Given the demographic reality now upon us—of slower growth and rising benefit costs—the discussion of ultra-longs is certainly timely. While we’re not facing the Napoleonic Wars, we may be facing the fiscal equivalent thereof.