I was not a big believer that restaurant stocks would post strong performance in 4Q09 when comparisons “were easy” – demand is just not there. While many analysts have suggested that the decline in capacity was a net positive for the industry, the decline in visits has been enough to offset it (and then some) so there is really no net improvement in trends for the industry.

In 2008, the restaurant industry faced both declining demand and historically high input costs (the double-edged sword). The big story in 2009 has been that margins have benefitted from dramatically lower food costs and a rationalization of individual business models, despite no recovery in top-line trends. In 2010, I am not yet a believer of the demand-recovery story and the cost cutting story will be in the rear view mirror, as will the lower food cost story. In that respect, the underlying themes in 2010 may not be too different from 2008; though the magnitude of commodity inflation may not be as great and the decline in demand not as surprising.

Demand Trends

I see no real shift in 2010 in the consumption-led recession that the restaurant industry faces. Employment issues, access to credit and increased savings (or debt reduction efforts by consumers) will continue to put incremental pressure on traffic trends and average check.

According to NPD's CREST data, traffic declined across all restaurant segments for the quarter ending September 2009. Total industry traffic declined 4% YOY in 3Q09. By segment, visits to QSR declined 4% and Casual Dining visits were down 5%.

Casual dining same-store sales growth, as measured by Malcolm Knapp, continues to get worse on a 2-year average basis as we move through 2009 (outside of July, when operators, on average, posted their biggest declines year-to-date). QSR demand trends have fallen off more significantly in recent months, leading JACK management to say in a presentation last week that it now appears that consumers are trading out of the restaurant segment rather than trading down to QSR.

Margin Trends

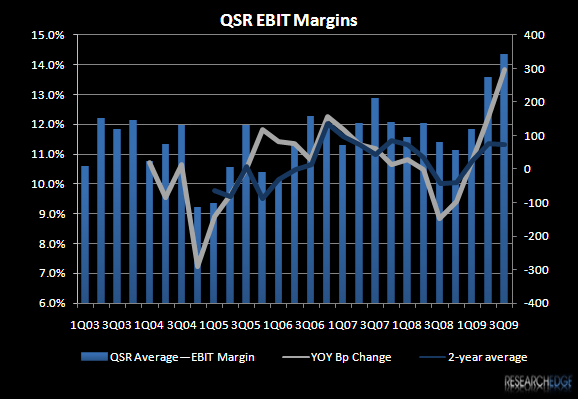

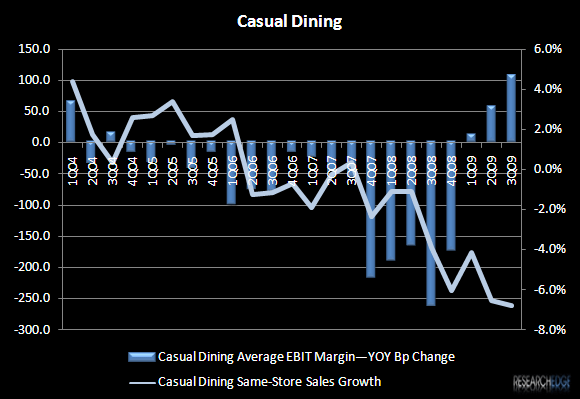

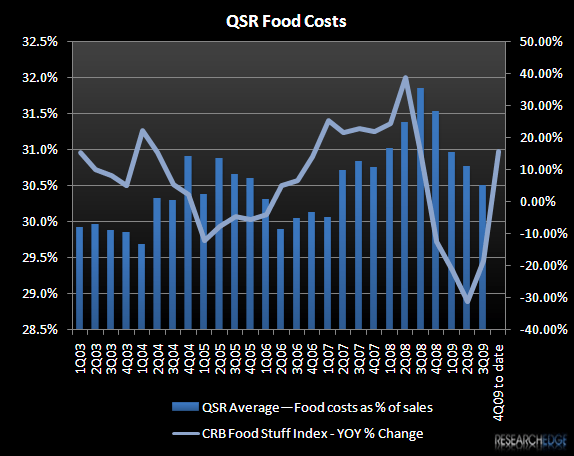

I have been saying for some time now that the trajectory of margins in 2009 is not sustainable without a pick-up in top-line trends. As you can see in the charts below, both QSR and casual dining margins have moved higher in 2009 after declining for most of 2008 for QSR and for a much longer period of time for casual dining. Specifically, 1Q09 marked the first time the casual dining operators on average grew margins since 3Q04. The two food cost charts below also show that both the QSR and casual dining sectors have benefitted tremendously from favorable YOY commodity costs in 2009 as food costs combined with labor costs account for about 60% of restaurant companies’ operating expenses.

Although food costs as a percentage of sales have continued to move lower on a YOY basis, the trend for food costs is already moving higher as evidenced by the CRB Food Stuff Index (also shown below), which bottomed in 2Q09. For the casual dining names on average, the change in food costs as a percentage of sales on a 2-year average basis appears to have already bottomed in 2Q09; though costs are still coming down YOY.

The decline in absolute commodity costs, however, is not the only factor to consider when looking at food costs as a percentage of sales. Also impacting these numbers is the prevalence of industry discounting. Without such discounting, these food costs as a percentage of sales would likely be lower. I would argue that lower food costs in 2009 have afforded restaurant companies the opportunity to take promotional activity to a new level in a desperate move to stave off traffic losses. The real question in 2010 is what the impact on margins will be if this discounting continues when food costs move higher. And, if rising costs force companies to rethink their discounting tactics, what will happen to demand?

I maintain that margins will again be the big story in 2010; though I do not expect them to move in the same direction as 2009. Demand will remain soft and food costs are likely to move higher. And, the commodity headwind in 2010 will only complicate the fact that most companies will be lapping the bulk of cost saving initiatives they took in late 2008/early 2009.

Food Costs Trends

When it comes down to understanding the dirty details on food costs, the timing is slightly different for each individual company due to long-term contracts. Regardless of the timing and length of contracts by company, it does not change the fact that we will be hearing about higher food costs in 1Q10.

Beginning in 2010, the dagger in the back of the restaurant industry could result from declining food production and a more rational food processing industry. In November, global food costs jumped 7%; the most since February 2008. So far in 2009, farm price inflation has lagged behind prices for copper, gold and oil. The big MACRO question is will the global economic recovery, especially in emerging markets, spur an increase in demand for food and thus, drive commodity prices higher?

In an inflationary environment, the agricultural commodities and related stocks will be the biggest beneficiaries. On the margin, restaurant companies will be the biggest losers; the marginal restaurant concepts will be hit the hardest. I’m thinking about smaller companies in the very crowded Bar and Grill segment, like RT and CHUX, who do not have the same level of purchasing power as that of their larger competitors.

As a result of the combined impact of lower herd sizes and low inventories in a number of grains markets, the prospect of food inflation in 2010 cannot be ruled out.

Pork and Poultry processors are reducing herd size

After two-years of losing money, pork farmers have cut the herd size to the smallest level since the USDA started collecting data in 1964. As a result, wholesale-pork prices are up 27% this year. While this may already seem dramatic, the CEO of Smithfield Foods believes that “further liquidation is needed." 2010 projections include another 4% cut to herd size. As an aside, I’m not naive to the fact that Smithfield Foods has a big economic incentive to convince competitors to reduce production.

The same holds true for the poultry industry. In 2009, broiler production decreased for the first time since 1975; the USDA is estimating a 3% decline in 2009. Currently, the USDA is forecasting a 1% production increase in 2010. However, there is a chance that production could decline again in 2010 for the following reasons: (1) the continuation of volatility in feed costs, (2) uncertainty of maintaining exports to the two largest markets - China and Russia, (3) a sluggish economic recovery in the United States and globally, and (4) continued reluctance on the part of banks to lend money.

The key segment to watch in 2010 is wholesale chicken wing prices. Currently, wing prices surpass boneless/skinless breast meat prices. The ever-growing consumer demand for buffalo-style wings is putting increased pressure on a relatively fixed supply of wings. As the boneless wings trend continues, it will help ease the price pressure on bone-in wings while adding marginally to the demand for breast meat. I continue to be very cautious on BWLD going into 2010.

Milk Supplies are tight

In 2010, higher milk and cheese prices are almost a given. In 2009, dairy farmers have been reducing their herd size, too. Currently, domestic dairy production is down 8.2% in 2009. According to the USDA, the price of nonfat dry milk, used in baking products and baby formula, will rise to an average of $1.275 a pound next year from 92 cents, and cheese will increase 28%. Also, the USDA thinks processed and fluid milk will jump 31% to $16.75 per 100 pound.

Corn prices and Federal mandates

Corn prices began to decline in 2008 when it became apparent that flooding in the Midwest had not devastated the corn crop and that farmers would harvest another large crop in 2009. Fast forward to today and the USDA is projecting that the US will need more corn in the coming months than will be harvested; the implications are that we are beginning to draw down on reserve stocks. The likelihood that we could face a repeat of 2008 increases as the federal mandate for corn-based ethanol keeps increasing.