Below are analyst updates on our fifteen current high-conviction long and short ideas. We will send Hedgeye CEO Keith McCullough's refreshed levels for each in separate email.

Please note that we removed HCA Holdings (HCA) from the short side and Corning (GLW) from the long side this week and added Red Rocks Resorts (RRR) to the long side of Investing Ideas.

IDEAS UPDATES

UUP | XLU

On the data front, we’ll hit on the jobs report for May, income and spending data from earlier this week, and also manufacturing ISMs from Thursday. We also outline our views on real growth within the context of our Q2 Macro theme: #Reflation’s Rollover.

Jobs Report: Don’t worry about nailing the number here. As we’ve always said, rate-of-change matters most with the monthly non-farm payrolls report…

The May NFP comp was the easiest of the present mini-cycle at +43K (last May). Non-Farm payrolls only needed to increase +44K on Friday to accelerate year-over-year – calling out positive rate of change was a high probability bet, and we like high probability bets at Hedgeye.

Here's the breakdown of the report:

-

Headline print 138K = +7bps of acceleration in YoY growth to 1.58% YoY

-

Private prints +147K = +11bps of acceleration in YoY growth to +1.77% YoY (gov’t hiring weak … hiring freeze apparently having some measure of impact)

-

Wage Growth = Flat at +2.5% YoY

-

Aggregate Hours … Flat sequentially at +1.71% YoY, continuing Trend Acceleration

Income & Spending: Real Consumption and Income were both strong M/M in April in the face of a higher deflator and March was revised higher – a prior upward revision means that the rate-of-change comp effect is higher. The positive revision to March, of course, dampened the reported April gain. Both decelerated modestly on a Y/Y basis.

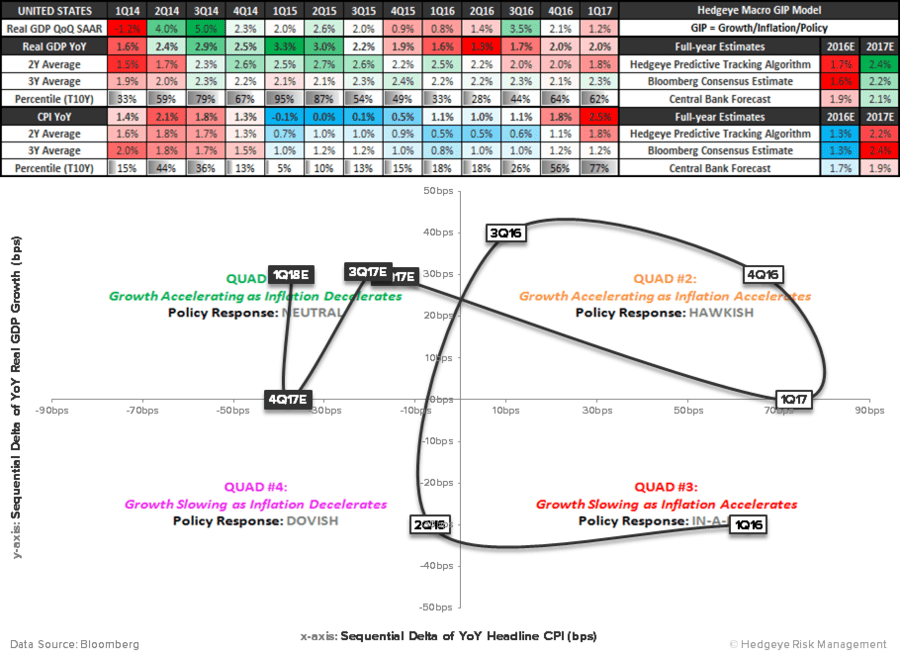

Income growth (& likely consumption by extension) should accelerate alongside the labor data in May. Comps (employment, Income, savings rate) get tougher after May. With Tuesday’s soft PCE data our Q2 GDP forecast ticked down to +2.30% YoY/+2.43% QoQ SAAR, but as can be seen in the GIP snapshot below, the overall growth accelerating theme remains intact for the balance of 2017.

ISM Manufacturing: The headline number ticked up as employment rose. New Orders tested a 60-level again. Export orders remain supportive of a favorable outlook for Net Exports Prices fall -8pts as Reflation’s Rollover continues its pervasive manifestation - All-in-all positive on the margin.

The main takeaway with regard to long-term growth and currency strength is that U.S. data continues to signal a Quad 1 environment for the next 3 quarters. An important snapshot of our GIP model is included below with this sequencing in real growth (Quad 1 = Growth accelerating as Inflation Decelerates).

Part of the sequencing in the shift from Quad 2 in Q1 to Quad 1 for the remainder of the year is that inflation decelerates to get there. Our #Reflation's Rollover call is likely taking down the inflation expectations component for both USD and rates – this has put short-term pressure on our long dollar (UUP), short utilities (XLU) call.

Now that QUAD 1 has settled in, we expect utilities to underperform other sectors (they always have historically by a wide margin in QUAD 1) and the relatively more positive set-up in the U.S. economy, especially next to Europe which will be in Quad 4, to be supportive of long-term dollar strength.

TWX

Click here to read our original analysis on why we think the AT&T/Time Warner (TWX) deal will be approved. Below is an update from Telecom analyst Paul Glenchur:

This week, at an industry conference, Time Warner’s CEO Jeff Bewkes reaffirmed his expectation the Justice Department will not take action against the proposed AT&T-Time Warner deal.

Meanwhile, the Senate Judiciary Committee is scheduled to vote out the nomination of Maken Delrahim to head the Justice Department’s Antitrust Division. The vote should take place next week, probably June 8. We expect no significant obstacles to his confirmation, and anticipate he will soon take office and begin the final evaluation process regarding the antitrust issues affecting the deal. Late last year, in an academic capacity, Mr. Delrahim indicated that he did not believe there would be major obstacles to closing this vertical transaction.

The career staff of the Antitrust Division has conducted a thorough investigation of issues that could raise concerns. Mr. Delrahim and his leadership team will make the final call regarding the Justice Department’s approach and whether litigation would be justified. At this point, the FCC has not taken a formal role in reviewing the merger and is not a regulatory obstacle to approval.

We continue to believe the deal is likely to avoid litigation in federal court and should ultimately win approval before the end of the year.

MIC

Click here to read our analyst's original report.

No update on Macquarie Infrastructure Corp (MIC) for this week's Investing Ideas but below is the overview of the short thesis which Hedgeye Energy analyst Kevin Kaiser reiterates.

WMT

Click here to read our analyst's original report.

Last week Amazon opened its FreshPickup locations to the public (Prime Members) for the first time. There is only two locations so far outside of Seattle.

Interestingly, Wal-Mart (WMT) has been doing grocery pickup for more than a year, and accelerated expansion with an announcement exactly a year ago when it was already serving 13 markets.

Also, this week Wal-Mart announced it is testing a program to use employees as delivery drivers for online orders on their way home from work.

The point is that Wal-Mart’s physical store presence serves as an advantage as it tries to figure out how to blend brick and mortar shopping with digital commerce. Now it’s investing in e-commerce assets at an unprecedented rate. The battle in the ‘omni-channel’ mass market space is quickly becoming a 2 horse race.

We’re not saying that Wal-Mart will beat Amazon, but both are and will continue to leave Target in the dust, and there can be two winners here for a very long time if they play the right strategy.

CFG

Click here to read our analyst's original report.

The balance sheet optimization initiative at Citizens Financial Group (CFG) continues to manifest itself through a visibly shifting loan composition, sourcing of funds, and higher spread between interest-earning assets and interest-bearing liabilities. CFG is adjusting its funding mix to achieve greater stability and better match the duration of its assets through an increase in long-term funding.

In the most recent quarter, CFG's net interest margin increased +10 bps YoY and +6 bps QoQ, largely attributable to an improved funding mix and asset pricing from CFG's continued balance sheet optimization strategies. We can see that CFG remains on the track toward mean-reversion as it continues to make efficiency gains. In turn, efficiency gains and an improved funding/asset mix have been realized through CFG's steady income growth.

EXAS

Click here to read our analyst's original report.

UnitedHealthcare (UNH) recently released updated coverage determination guidelines for preventative care services which included Cologuard and cited the latest United States Preventative Task Force (USPSTF) guidelines in June of 2016. This positive coverage decision, effective July 1, 2017, is consistent with our thesis that guideline inclusions will drive commercial adoption. UNH is the largest managed care provider in the United States and provides insurance for ~45M people in the US.

Exact Sciences (EXAS) management has been adamant about contracting at or above the current Medicare rate and mentioned that it takes about one year from the time of a positive coverage decision to the time they receive a contracted rate with a payor. Assuming this, even if EXAS receives a contracted rate that is lower than the current Medicare rate of $512.43, UNH's contracted rate would not negatively impact Cologuard's PAMA rate until 2021.

IVZ

Click here to read our analyst's original report.

Recently, we outlined the rationale for a long position in Invesco (IVZ). The company is exposed to the exponential growth rate in ETFs year-to-date, with industry fund raising at +$134 billion in the first 3 months, over 4x the industry's asset growth in 1Q2016.

Invesco benefits from these trends through its ownership of the 4th biggest passive franchise in Powershares which has disproportionate market share in "smart beta" ETF products which have an average realization rate of 0.45% versus "plain vanilla" ETFs at a 0.22% fee.

KATE

No update on Kate Spade (KATE) for this week's Investing Ideas but Hedgeye Retail analyst Brian McGough reiterates his long call on the company.

RLGY

Click here to read our analyst's original report.

Here's an update on Realogy (RLGY) from Housing analyst Josh Steiner:

The Not so Good:

Pending Home Sales declined -1.3% sequentially and -3.4% year-over-year in April, completing the Terrible Trifecta (NHS, EHS, PHS) of negative distortion pervading demand based series across the housing complex to start 2Q.

The simple conclusion to all of this is that reported demand in April was negatively distorted by the floating Easter holiday and should reflate in May as the effect resolves. Tight supply will continue to constrain the upside in volume growth but the April data understate the underlying reality which we believe remains one of trudging improvement rather than negative inflection.

Now for some good news:

In prior weeks, we have noted that the trend in high end real estate volume comports with the broader rebound in luxury spending nationwide. High ticket discretionary consumption (pleasure boats, aircraft, jewelry and watches - our proxy for the state of luxury consumerism) has grown +5.5% thus far in 2017, a notable acceleration off of 2016's post-recession low watermark of 1% growth.

We see the recent uptick in luxury discretionary spending as positive for the high end housing market, and Realogy specifically.

DE

Below is a note written earlier this week by Hedgeye CEO Keith McCullough on why we still don't like Deere (DE):

Looking for overvalued stocks that my analysts don't like that are at the top-end of the risk range?

Look no further than Deere (DE) which we've been nimble signaling on in Real-time Alerts so far. For those of you who haven’t done it for 19 years, the art of short selling is this - don't lose money.

This deal DE announced this week caught my eye. Why now? Well, here's Jay Van Sciver's view:

"I think it signals that they didn’t get the pop in commodity prices they needed, see a further downcycle coming. It mirrors WAB + Faiveley – it is even a privately held European company. It adds a whole new business line to DE, making it more complicated to analyze. Pretty classic move. We STILL haven’t gotten the 10-Q, which has all the useful data in it. One of the longest quarterly report-to-filing delays we have seen. My guess is that the credit data continued to get worse."

Short green,

KM

GEL

Fair Value ~$15/unit, Short Thesis Intact......We continue to like Genesis Energy (GEL) on the short side for its high valuation, super-aggressive non-GAAP accounting, high leverage, and low quality asset base and management team. GEL is a slow-moving train wreck that may be able to hang in through 2018 as GoM crude volumes continue to grind higher, but we think that ultimately the Company will be forced to reduce the distribution and the stock will trade to fair value, which we estimate to be ~$15/unit based on our DCF.

SNAP

We sat out the 1Q print since we didn't have much reason to be there. Mgmt already told the street that it wasn't providing guidance, so the only play on the print was on the quarter itself, and we don't have any edge on the quarters yet.

We chose to use the 1Q print as a sniff test instead. We suspected that the seasonal decline in 1Q revenue that mgmt flagged in its S-1 could have been a headfake. If so, Snap (SNAP) could have have been a +$30 stock at this point. However, the fact that it wasn't gives us more confidence that consensus is overshooting SNAP's near-term revenue growth prospects, which we previously viewed as the only real positive in the story.

CAKE

On Cheesecake Factory (CAKE) most recent earnings call management was pressed hard on mall traffic, but did not budge. They repeatedly stated that the Company is seeing absolutely no effects at Cheesecake units, as it relates to slowing mall traffic.

Nonetheless, we suppose that this leaves room for interpretation, given the fact that mall traffic is at historic lows, and 90% of Cheesecake units are located in or in close proximity to malls, but the Company is reportedly feeling no effects.

With CAKE traffic down -2.3% in 1Q17 (and down -1.4% on a two-year average basis) and no mention of the Company’s four year traffic decline in the business review portion of the earnings call, we, and many others, would like to know what the long-term plans are to reverse these traffic trends.

RRR

Below is a brief note from Hedgeye CEO Keith McCullough explaining why we added Red Rock Resorts (RRR) to Investing Ideas:

"Remember, the winner in Reflation's Rollover is real (inflation adjusted) consumption.

So, on the other side of shorting "reflation" ideas, we'll keep telling you to allocate assets to real-consumption growth assets like US Tech and Consumer Discretionary.

Long rich people? We like that too; especially people who are feeling rich at casinos!

One of Todd Jordan's favorite US Gaming stocks is still Red Rock Resorts (RRR). Here's his latest update on the Las Vegas Locals market:

"We are currently in the midst of an LV locals refresh study and continue to come across compelling data points that suggest the local economy remains on a solid footing. Evidence of such strength is well publicized in the media via the typical indicators: home prices, wages, job growth, etc. In addition to the strength in those indicators, we’ve come across additional datasets that supports continued growth in the locals gaming sector.

Driver’s license surrenders, a proxy for immigration to Clark County has improved over the last 18 months and is now growing in the high single digit range – slightly ahead of historical averages. Additionally, total gasoline demand (# of gallons sold per month) has finally surpassed its prior cycle peak and is finally growing at its normal expansionary run rate.

Long term, RRR should be the primary beneficiary of the increasingly favorable supply/demand environment in the LV locals market."