With Citigroup repaying TARP and Abu Dhabi bailing out Dubai, markets are rallying across the board. The only green not on my screen is the NIKKEI 225, down small. The Tankan index (confidence among Japan’s largest manufacturers) rose the least since the economy emerged from its worst postwar recession as the strong YEN will erode profitability.

Last week the MACRO calendar dominated the news flow. On Friday the S&P finished higher by 0.4% on fairly quiet trading. On the MACRO front sovereign issues and TARP repayments seemed to be top of mind, but on the margin there were a number of positive issues. Last week the Dow rose 0.80%, S&P rose 0.04%, but the NASDAQ declined 0.18% and the Russell declined 0.40%.

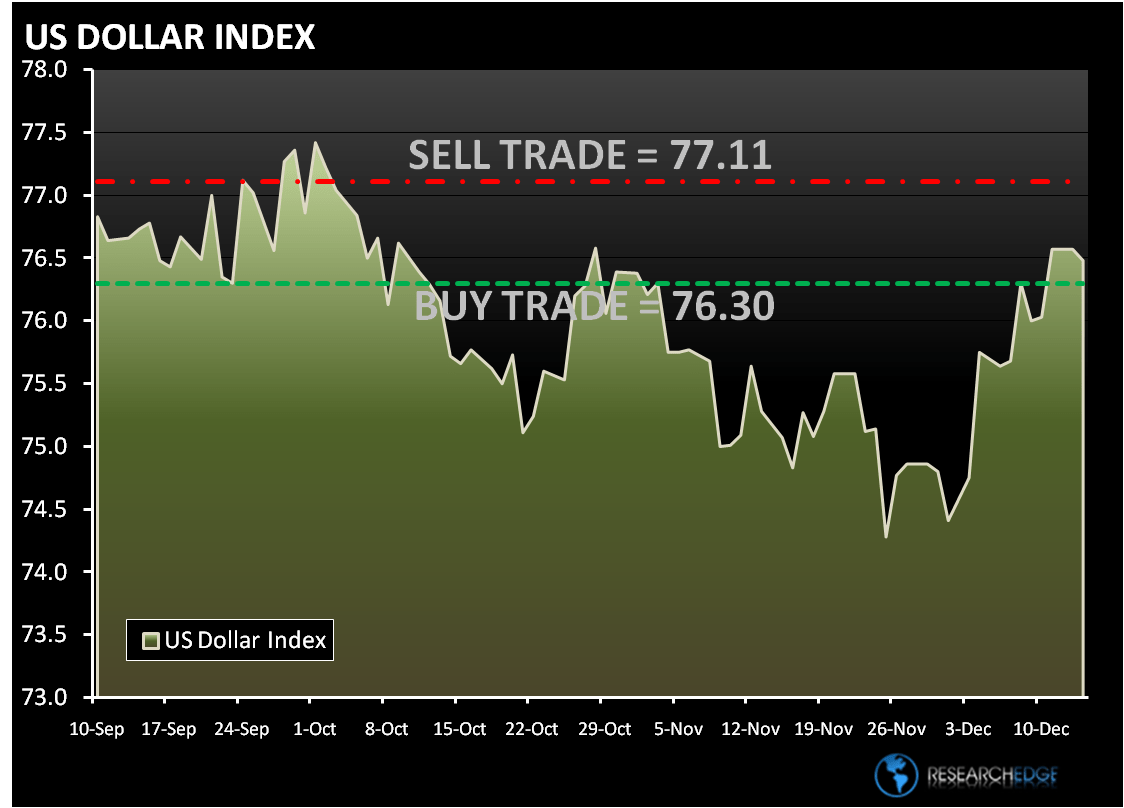

On Friday the Dollar index closed at 76.573 up 0.7% on the day. The Dollar index was up three of the five trading days last week.

The RECOVERY theme gained momentum with the better-than-expected increase in Chinese industrial production. In addition, the retail sales data and the U. of Michigan consumer sentiment data helped retail and Consumer discretionary stocks in general. The Consumer Discretionary (XLY) outperformed the S&P 500 by 210 basis points last week.

Better consumer sentiment and improved retail sales numbers are leading to a breakdown in the RISK trade. Positive MACRO data out of the US traditionally suggests the RISK trade will outperform. Right now we are seeing a strong dollar with stocks up, led by the low beta Utilities (XLU). The breakdown in the inverse relationship between the dollar and risky assets is new.

After falling early in the week, the retailers rallied strongly on Thursday and Friday. Better-than-expected November retail sales and December consumer sentiment data created a positive underlying tone for the group.

The notable underperformer on Friday was Technology (XLK) – the only sector to close down on Friday. After being a star performer for two weeks the Semis have now become a headwind with the SOX down 1%. BRCM was one of the weaker names in the group ahead of next Tuesday's analyst meeting. Elsewhere, telecom equipment names were mostly weaker with JDSU, TLAB and CIEN taking the group lower. Weaker-than-expected November NPD data weighed on most of the video game stocks, while the MOBILITY names were also under pressure.

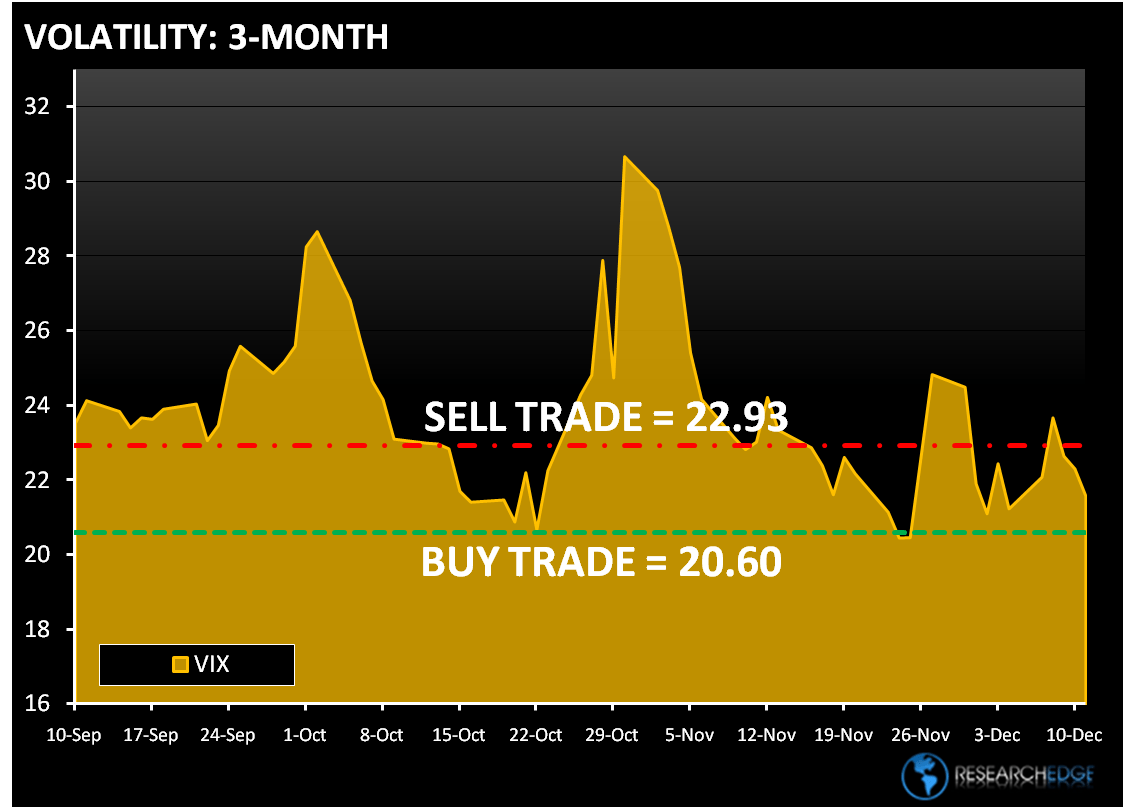

From a risk management standpoint, the ranges for the S&P 500, the Dollar Index and the VIX are seen in the charts below. The range for the S&P 500 is 17 points or 1.0% upside and 1.0% downside. At the time of writing the major market futures are trading slightly higher.

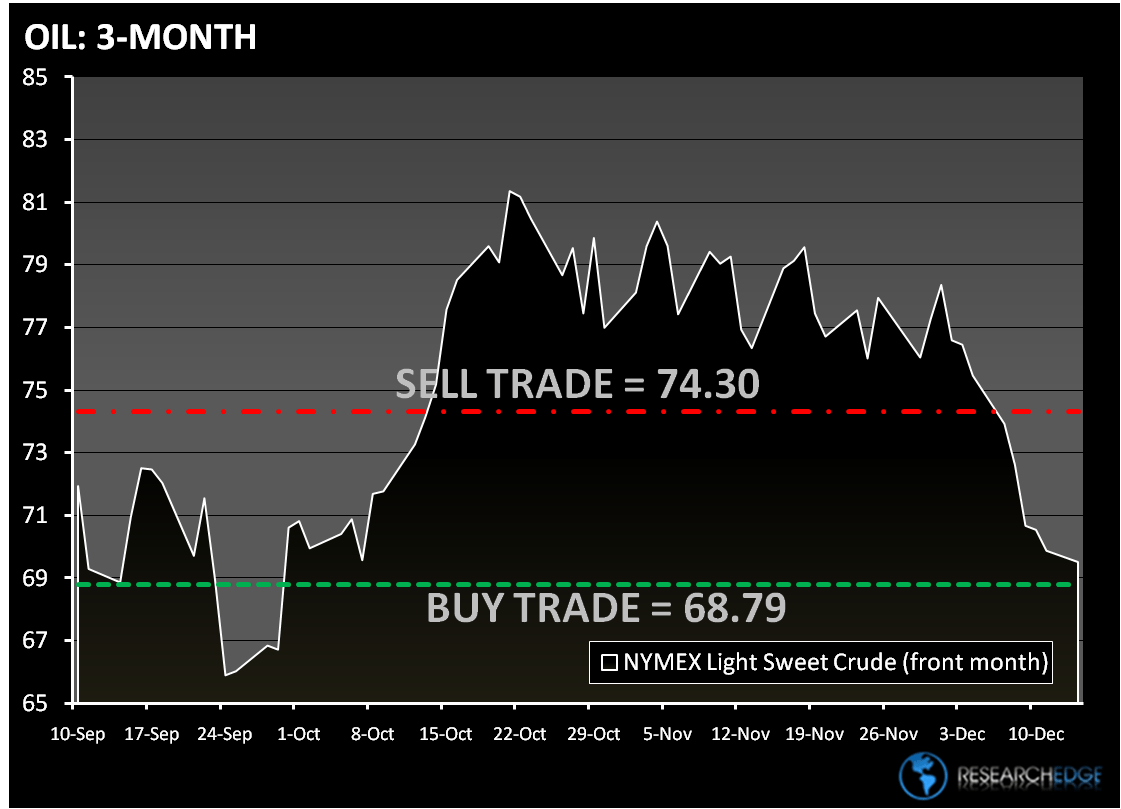

In early trading today, crude oil is trading lower for the ninth day, and is poised for the longest decline since July 2001. Declining on supply and demand issues crude is now down 15% since October 21 – the year-to-date high. The Research Edge Quant models have the following levels for OIL – buy Trade (68.79) and Sell Trade (74.30).

In London Gold is trading basically unchanged. The Research Edge Quant models have the following levels for GOLD – buy Trade (1,090) and Sell Trade (1,147).

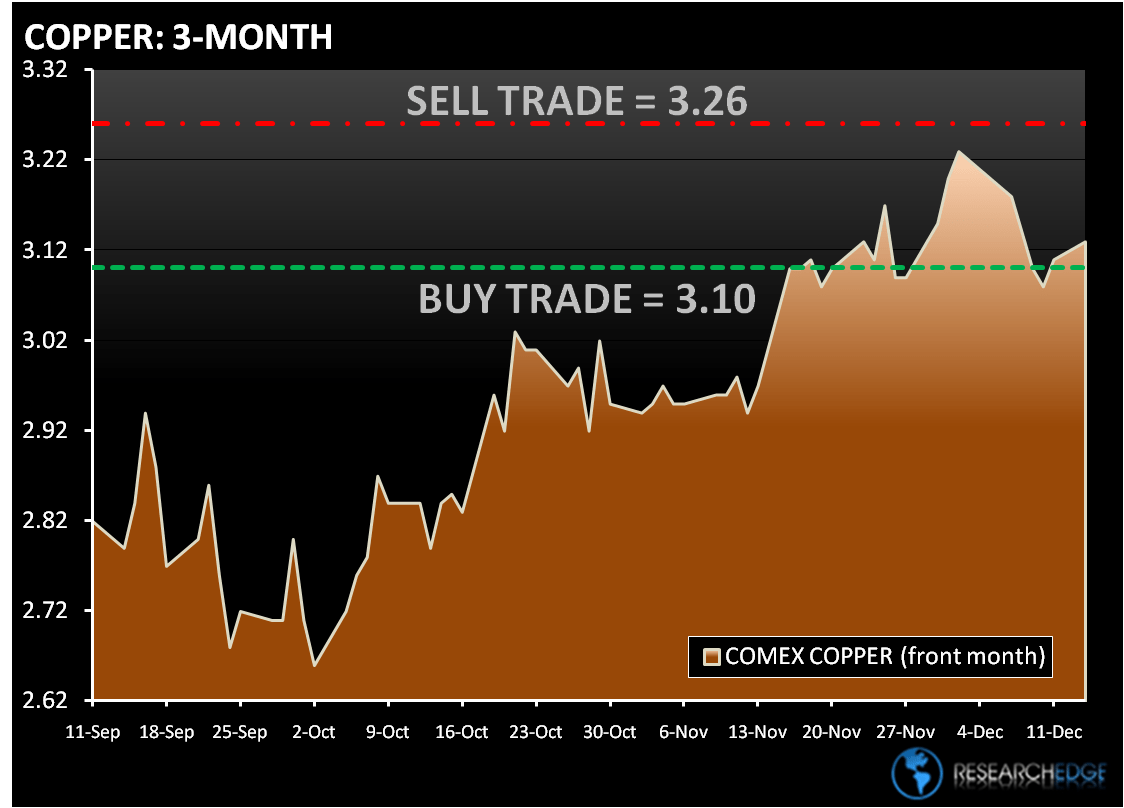

Copper is up for a second day with dollar down and optimism that demand from China will be strong. The Research Edge Quant models have the following levels for COPPER – buy Trade (3.10) and Sell Trade (3.26).

Howard W. Penney

Managing Director