Regional markets laid an egg in November with same store revenue down 7%, and that’s without the gas headwind.

We estimate that same store revenue in the regional markets declined 7% in November (only LA and MS haven’t reported). November 2009 did contain one fewer Saturday but the comparison (-4%) wasn’t exactly difficult. Combining October (one extra Saturday) and November yields a y-o-y decline of 4%.

Given October’s decent performance, many analysts are undoubtedly disappointed. Other consumer sectors fared better in November – retail sales were surprisingly strong – which furthers the trend of gaming underperformance. Gaming continues to face a combination of soft discretionary spending and a declining share of the discretionary wallet (see our 10/19 note “THE DOUBLE PCE WHAMMY TO GAMING”).

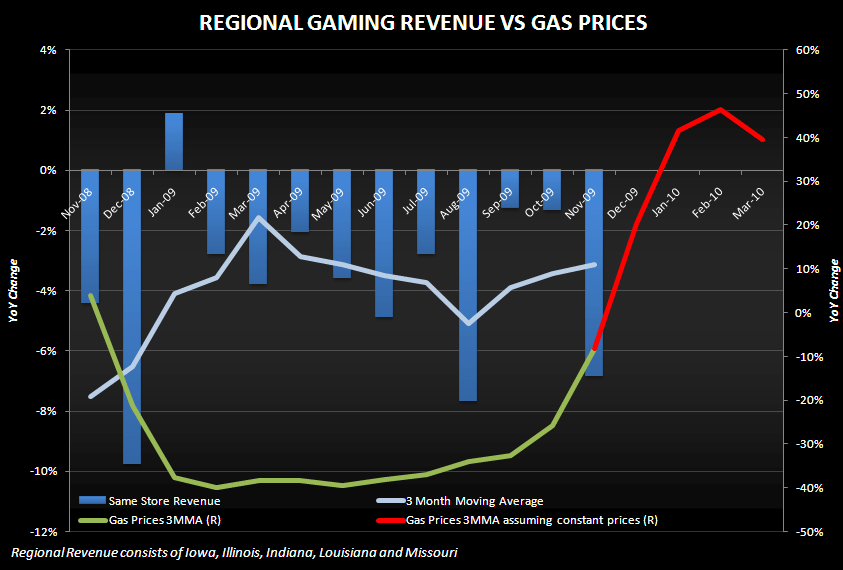

Add a third negative factor to the mix: gas prices. As shown on the following chart, y-o-y gas prices will be up significantly in December and this headwind will persist through the first quarter at least. Changes (y-o-y) in gas prices have historically been a statistically significant driver of gaming regional gaming revenues. That’s bad news for the regional gamers already facing other headwinds.

What does this mean for the stocks? The regional gaming stocks have underperformed the market as can be seen below. The stocks are not overly expensive but 2010 numbers probably need to come in. Until they do, it’s hard to make a strong bull case for the group.