In the past month, we witnessed the DJIA holding above 10,000, President Obama’s new strategy for the war on terror, a "less bad" unemployment rate at 10.0%, and more than enough holiday commercials!

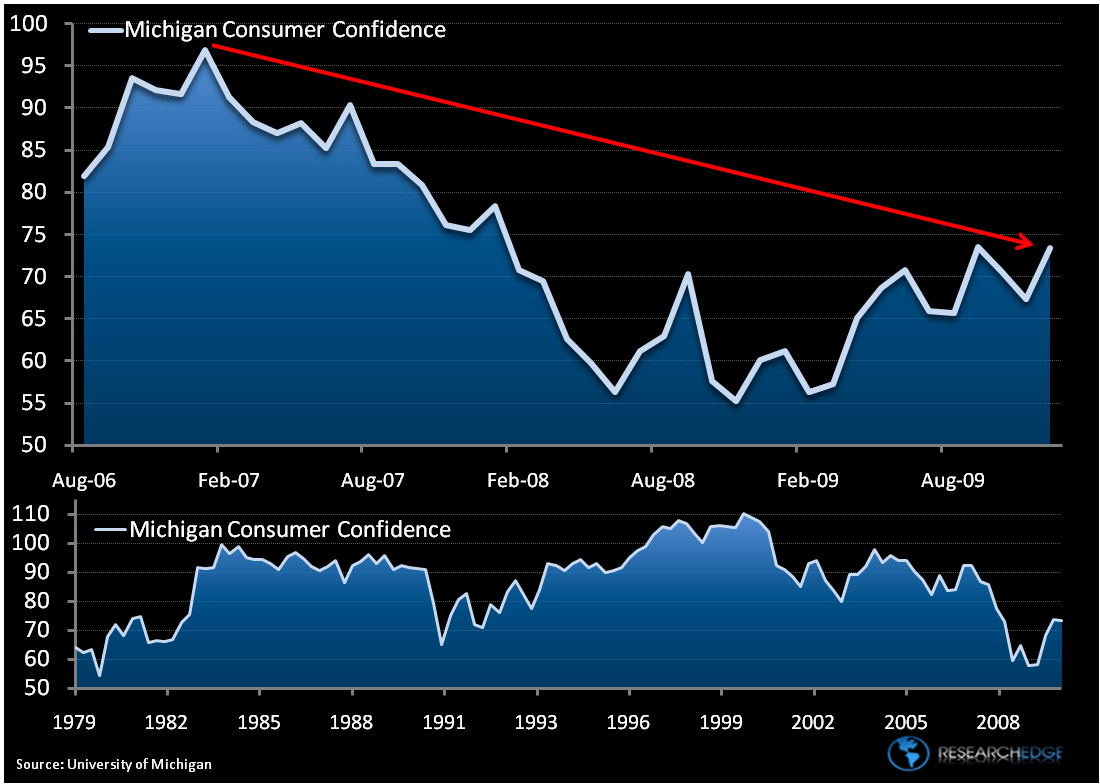

Surprisingly, confidence among U.S. consumers increased in December for the first time in three months. However, current sentiment remains well below indices from more prosperous times.

The Reuters/University of Michigan preliminary index of consumer sentiment rose to 73.4 in December, from 67.4 in November. The December figure exceeds the average of 65.0 for the first nine months of the year.

Contradicting some of my thoughts earlier in the week, the U of Michigan’s measure of CURRENT CONDITIONS (which reflects a slightly better job market) jumped to 79.1, from 68.8 in November and is the highest level since March 2008. The index of EXPECTATIONS index also increased to 69.7 from 66.5 last month.

As you can see from the chart below, confidence clearly appears to be settling in at a higher level. This is just a preliminary number from the U. of Michigan survey, and the final number will likely be lower, but that is less important.

Better consumer sentiment and improved retail sales numbers are leading to a breakdown in the RISK trade. Positive MACRO data out of the US traditionally suggests the RISK trade will outperform. Right now we are seeing a strong dollar with stocks up, led by the low beta Utilities (XLU).

The breakdown in the inverse relationship between the dollar and risky assets is NEW.

Howard Penney

Managing Director