For the Balance of the week the MACRO calendar heats up with Initial Jobless claims today and Retail sales and the U. of Michigan consumer confidence on Friday. The consensus has the December preliminary confidence reading improving to 68.8 from 67.4. I don’t see how that is possible.

The S&P 500 finished higher by 0.4% on light volume yesterday. Looking at yesterday’s sector performance it was difficult to find any obvious theme running thru the market. The Materials (XLB - proxy for the RECOVERY trade) was the best performing sector, up 1.2%. Two other sectors that benefited from the RECOVERY trade, Energy (XLE) and Consumer Discretionary (XLY), were the worst performing sectors.

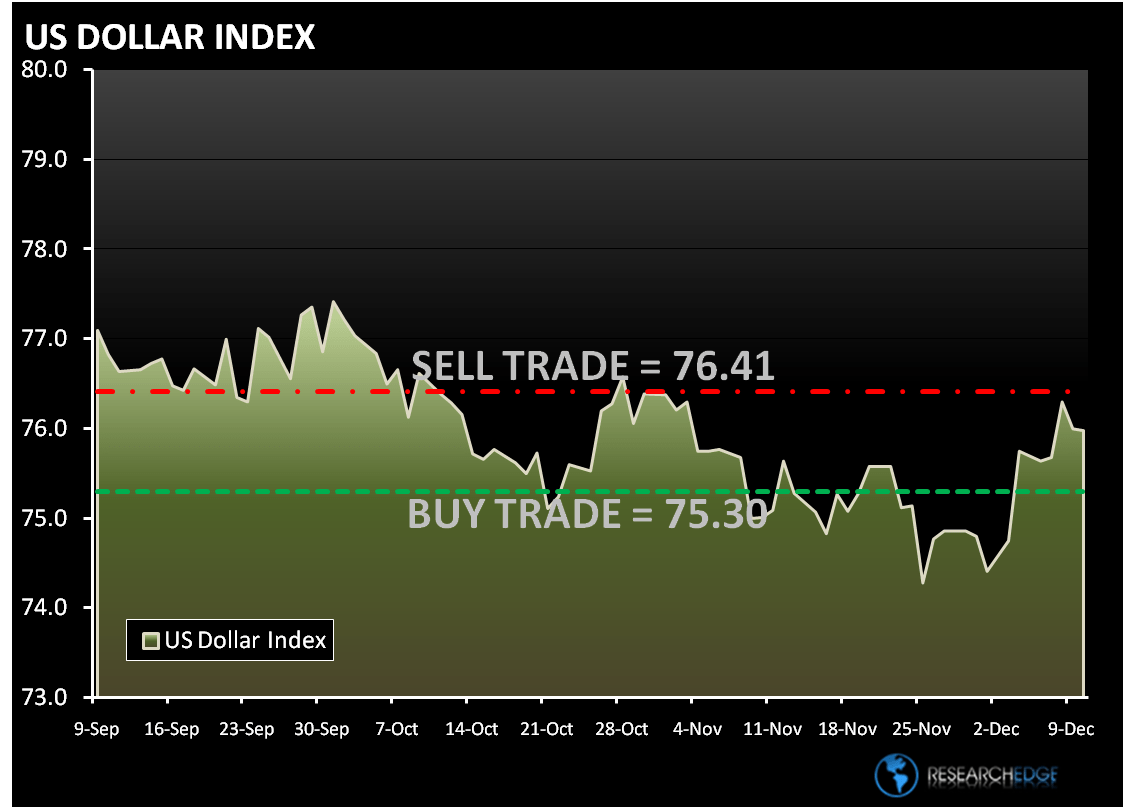

One problem the market is continuing to deal with is less appetite for the RISK, with recent sovereign concerns surrounding Dubai and Greece. While there does not appear to be any real current threat for meaningful contagion, uncertainties prevail. The takeaway from this is DOLLAR bullish!

The MACRO calendar had an upside surprise with the unexpected increase in wholesale inventories; wholesale inventories rose 0.3% month to month (the first increase since August of 2008) and a net positive for Q4 GDP growth. Consensus expectations were for a 0.5% decline. Increases in petroleum and farm products, which were largely driven by higher prices, were responsible for the bulk of the upside. Also, there was the largest increase in mortgage applications since 2-Oct.

For the fourth straight day managed care stocks moved higher (HMO +0.5%) on news that Senate Democrats reached a tentative deal to scrap a pure-play public option from its healthcare reform legislation.

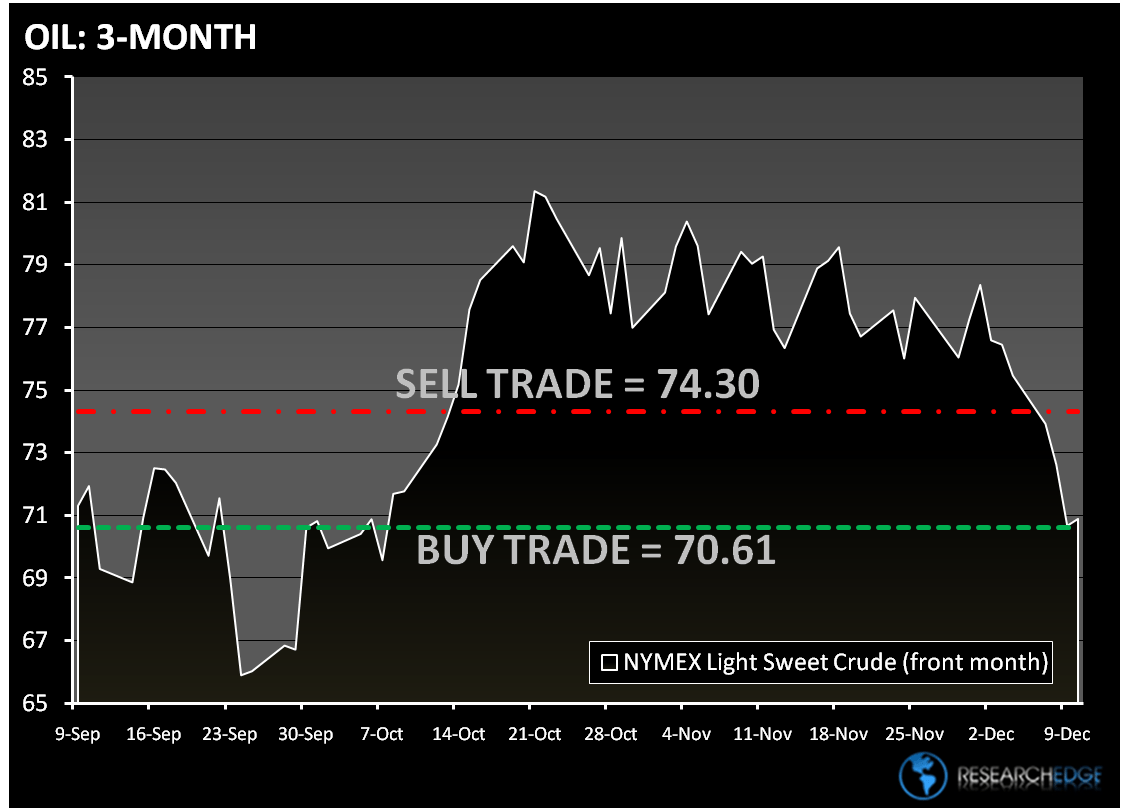

OIL is trying to tell us something! Oil Crude for January delivery settled at a two-month low of $70.67, down 2.7%. Oil is now down six days in a row, declining 7.8%. While the recent bounce in the dollar has been a headwind for crude, bearish inventory data seemed to be the big driver of yesterday’s decline.

Tech outperformed the broader market yesterday despite a muted reaction to the upbeat mid-quarter update from TXN. The star in Technology continues to be the SOX, which finished higher for an eighth straight day and eleven of the past twelve. The MOBILITY sector also did well with RIMM and AAPL up 4.9% and 4.2%, respectively.

A major reason for Consumer Discretionary underperforming yesterday was the Retail sector; the S&P Retail Index declined 0.7% on the day. The top three contributors to the decline in the XLY were Amazon, Nike and Target. It appears the market is starting to take notice that Nike’s big investment in Tiger Woods might not help them in 2010.

From a risk management standpoint, the ranges for the S&P 500, the Dollar Index and the VIX are seen in the charts below. The range for the S&P 500 is 25 points or 1.5% upside and 1.0% downside. At the time of writing the major market futures are trading slightly higher.

In early trading today, crude oil is trading near two-month lows on supply and demand issues. The Research Edge Quant models have the following levels for OIL – buy Trade (70.61) and Sell Trade (74.30).

In London Gold declined for the fifth time in six days, dropping 0.5% to $1,123 an ounce. The Research Edge Quant models have the following levels for GOLD – buy Trade (1,113) and Sell Trade (1,144).

Copper fell for a sixth day in London, the longest losing streak in a year. The culprit is the supply and demand issues. The Research Edge Quant models have the following levels for COPPER – buy Trade (3.09) and Sell Trade (3.26).

Howard Penney

Managing Director