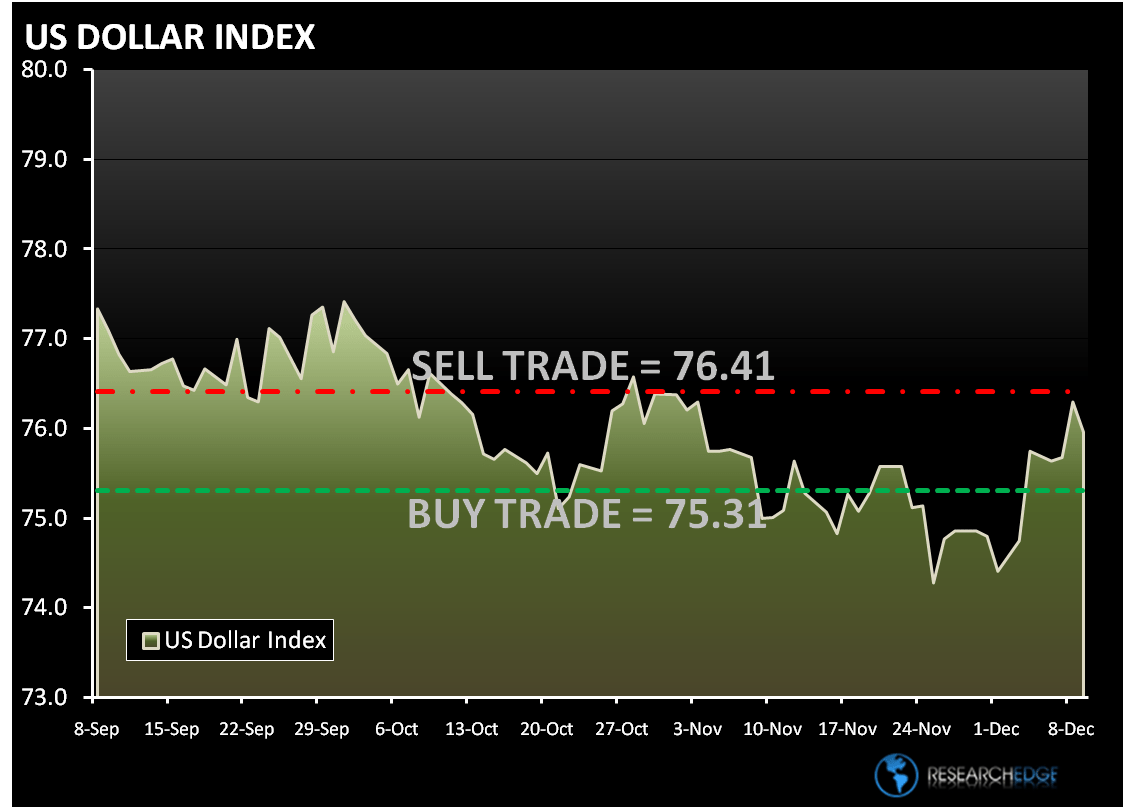

Yesterday, I wrote “on Monday there was no follow thru from the big move in the dollar on Friday.” Well, we got the follow thru we needed to from the Dollar index (DXY) yesterday. The DOLLAR index closed today at 76.19, up 0.6% on the day; over the last three trading days the DXY is up 2.1%.

The S&P 500 finished 1% lower on Tuesday, weighed down by the increased risk aversion resulting from renewed concerns surrounding both Dubai and sovereign credit ratings. The biggest impact of the risk aversion trade can be felt in the commodities and commodity stocks. The Energy (XLE) and Materials (XLB) were the two worst performing sectors yesterday. Increased sovereign concerns were highlighted by Fitch downgrading Greece's ratings to BBB+ and Moody's said that deteriorating public finances in the US and UK may “test the Aaa boundaries.” Thanks for that!

There was an interesting divergence in the SAFETY trade as the Consumer Discretionary (XLY -0.8%) outperformed the Consumer Staples (XLP -1.1%). The grocers presented the biggest drag for the sector as SVU (8.7%), SWY (6.8%) and KR (11.9%) sold off following weaker-than-expected Q3 results and reduced F09 guidance from KR. Reynolds American was another notable underperformer trading down 4.3% on the day.

The biggest drag on the XLY was McDonald’s, which reported softer-than-expected November same-store sales. Media names were the best performers in the XLY with GCI and IPG up 6.4% and 5.3%, respectively.

The Industrials underperformed the S&P 500 by 0.5%, despite better-than expected earnings from FDX. The company said that it expects fiscal Q2 EPS of $1.10, compared with prior guidance of $0.65-$0.95 and consensus of $0.85. Stronger volumes out of Asia were the primary drivers of the improved outlook. Surprisingly, UPS finished down 0.2% on the day.

The XLV also outperformed as the managed care group outperformed with the HMOs +0.7%; up for a third straight day. The group benefitted from continued reports downplaying the likelihood of the inclusion of a pure-play public option in the Senate version of healthcare reform legislation.

Technology (XLK) slightly outperformed the S&P 500 closing down 0.9% on the day. The XLK benefited from the semiconductors with the SOX +0.1%. The index has rallied nearly 9% over the last seven sessions. Yesterday’s performance benefited from XLNX, which raised its December quarter revenue and gross margin guidance. The company cited broad-based strength across all of its end-market categories and geographies.

From a risk management standpoint, the ranges for the S&P 500, the Dollar Index and the VIX are seen in the charts below. Today the range for the S&P 500 is 1% upside and 0.5% downside. At the time of writing the major market futures are trading slightly higher.

Crude oil is trading above $73 a barrel, arresting a five-day decline. The American Petroleum Institute said crude inventories fell by 5.82 million barrels last week. The U.S. Energy Department will release its weekly report today in Washington. The Research Edge Quant models have the following levels for OIL – buy Trade (72.59) and Sell Trade (77.92).

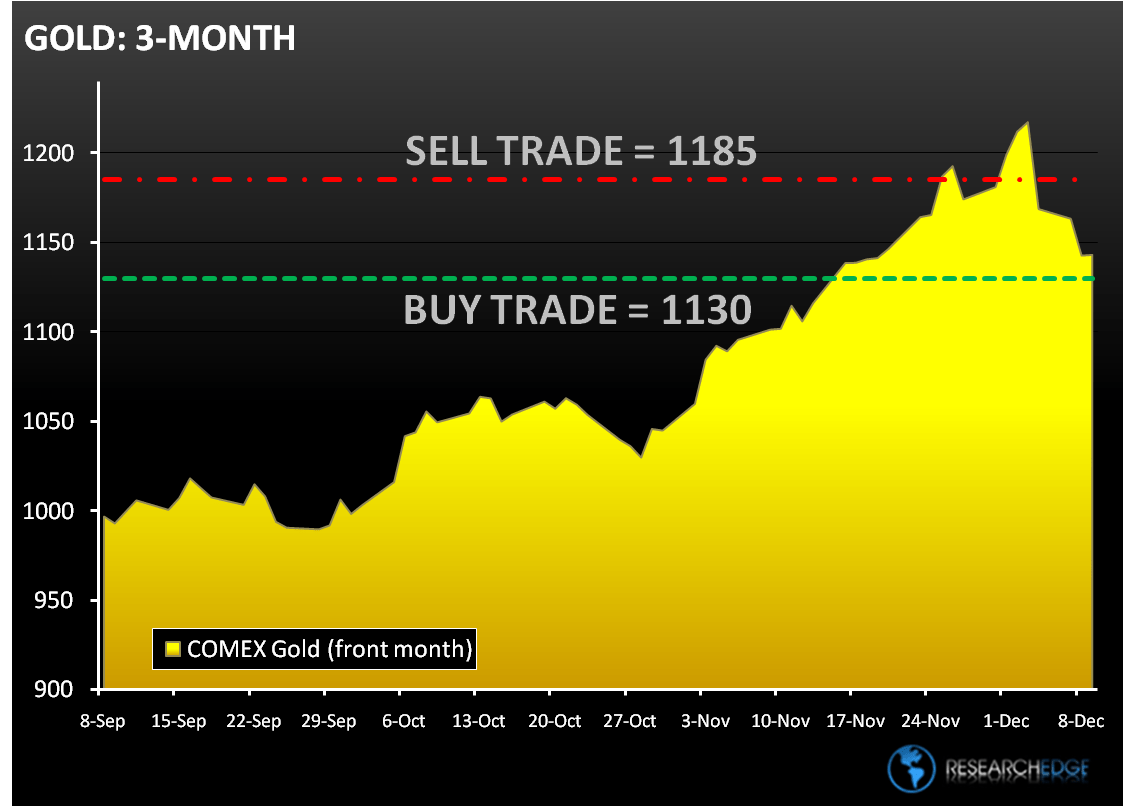

Gold for February delivery declined for a fourth day, dropping as much as 1.3 percent to $1,128.70 an ounce in New York. The Research Edge Quant models have the following levels for GOLD – buy Trade (1,130) and Sell Trade (1,185).

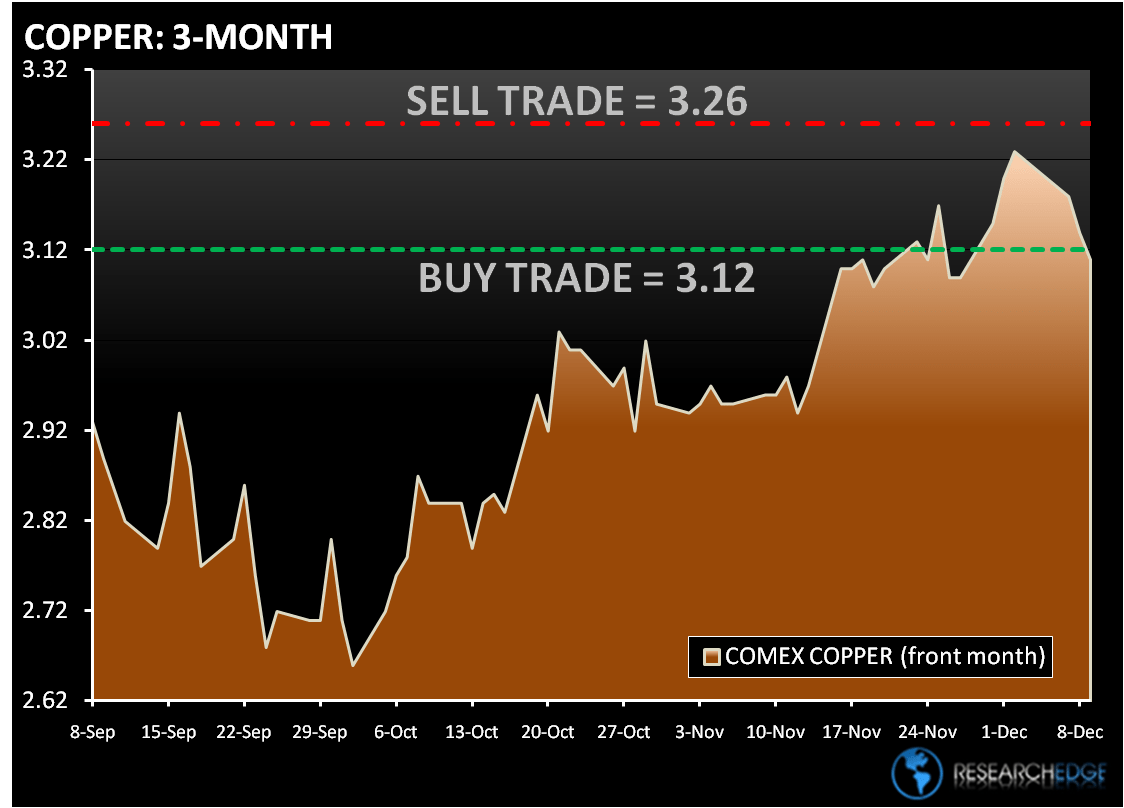

Copper fell for a fifth day in London, posting the longest losing streak since July. Japan’s economy grew less than expected in the third quarter and concern about Greece’s ability to meet debt commitments. The Research Edge Quant models have the following levels for COPPER – buy Trade (3.12) and Sell Trade (3.26).

Howard W. Penney

Managing Director