Last Friday, the Labor Department reported that employers in the U.S. cut the fewest jobs in November since the recession began, and the unemployment rate fell to 10% from 10.2%. Shockingly, payrolls fell by 11,000 as compared with the median forecast for a 125,000 decline (in a Bloomberg News survey of economists). How could so many “smart” Economists be that far off? Maybe they are right and we need to look into the source of the data!

The data reported by the government is not supported by other independent data sources that would have suggested a greater jobs loss than the consensus estimate.

First, the Conference Board reported some conflicting trends in November with those claiming jobs are “hard to get” hitting 49.8%, an all time high for the index (up from 49.4% in October). On the other hand, it also reported that the labor market outlook was slightly less pessimistic. The November survey said that those anticipating MORE jobs in the months ahead DECLINED to 15.2% percent from 16.8%, but those expecting fewer jobs decreased to 23.1% from 26.1%. As an aside, the proportion of consumers expecting an increase in their incomes decreased to 10.0% from 10.7%.

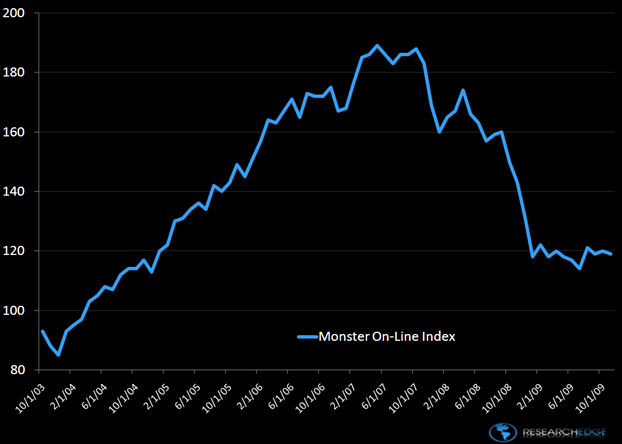

Second, according to the Monster Employment Index, the outlook on U.S. employment conditions WEAKENED in November. The Monster U.S. employment outlook index fell to 119 from 120 in October. The Monster index measures overall employee demand from online recruitment activity.

Third, the November ISM purchasing managers survey showed DETERIORATION in employment conditions. The November manufacturing survey saw the diffusion index drop to 50.8, down from 53.1 in October, which, in turn was up from 46.8 in September. A reading below 50.0 indicates outright jobs contraction.

It should also be noted that new claims for unemployment insurance have been declining over the past several months, but I don’t believe that that this data correlates perfectly to a turnaround in the employment picture. At best, we are seeing the beginning of a bottoming process, but the weakness in help-wanted advertising and other non-government data points confirm the downside pressures in hiring.

Is it true that people in Washington can make up the numbers? I thought they only did that in China! Is it true that the Bureau of Labor Statistics (BLS) has the ability to make the headline numbers look better than reality? Unfortunately, TRUST and WASHINGTON are two words that do not go together!

If this is at all true, it would help to explain why Federal Reserve Chairman Ben Bernanke said yesterday that the “U.S. economy faces formidable headwinds.” I would bet that the Chairman has inside information on the real numbers. I continue to be cautious on the CONSUMER going into 2010 and we are still short the XLY.

Howard Penney

Managing Director