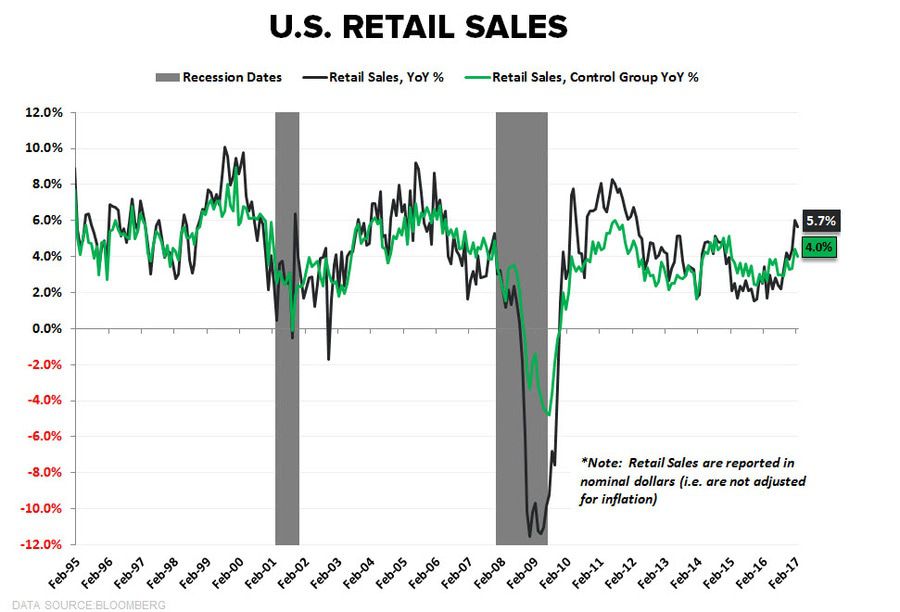

From a trending perspective (3 months or more), both US Retail Sales (+5.7% y/y) and CPI (+2.7% y/y = 61 month high) are straight up and to the right vs. where they were at the cycle lows of Q2/Q3 of 2016.

Reiterating our US #GrowthAccelerating call ... because the data continues to.