On the MACRO front we will be getting important data points as to the health of the consumer. Specifically, we are looking at data on Housing (existing home sales and Case Shiller), unemployment and consumer confidence.

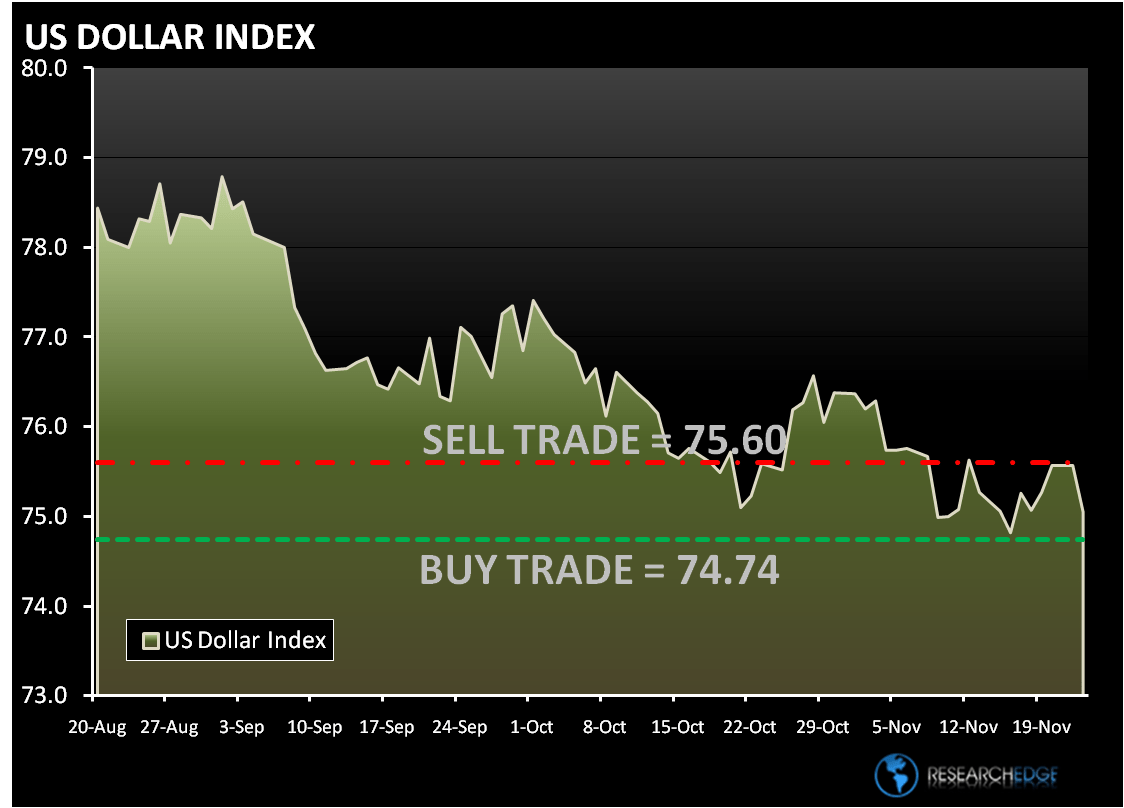

Last week the S&P declined for three consecutive days and the dollar index rose on Thursday and Friday. On Friday the S&P 500 declined 0.3% and finished the day off the worst levels of the day. Once again the headwinds were strong for the REFLATION/RECOVERY trade with the bounce in the dollar. The Dollar Index rose 0.48% on Friday.

The MACRO calendar was quiet on Friday, but there were some disappointing earnings in the Technology and Homebuilding groups. At 10am today we will be getting some housing data, with the Existing home sales trends. According to Bloomberg, sales of existing U.S. homes are expected to rise 2.3% from September to a 5.7 million annual rate.

The data flow over the past month does not support an upside surprise in existing home sales, so the chances that the consensus estimates are too aggressive are high. Last week mortgage applications declined 2.5% to the lowest level in 12 years. It was reported yesterday that mortgage delinquencies rose to a seasonally adjusted rate of 9.6% at the end of the 3Q09.

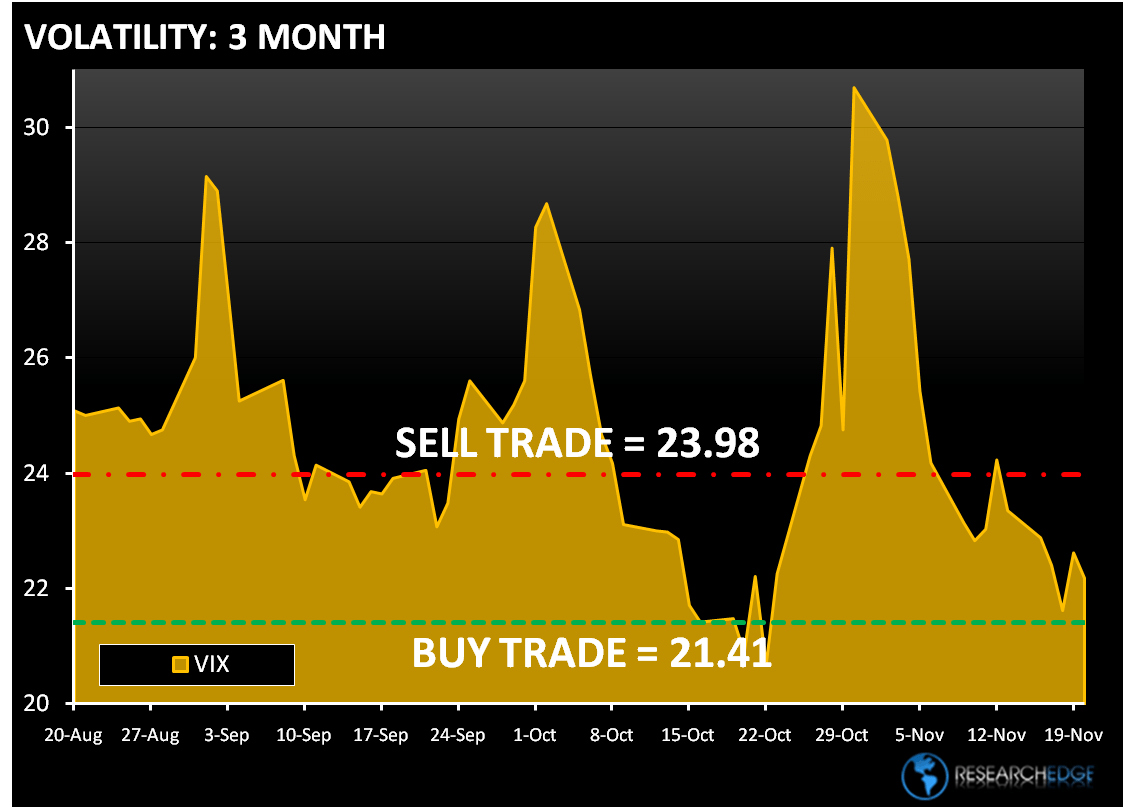

On Friday, the VIX declined 1.9% and 5.0% over the past week.

Three sectors increased on Friday – Healthcare (XLV), Utilities (XLU) and Consumer Staples (XLP). The best performing sector was Healthcare, up 0.7%. Healthcare was the beneficiary of a rotation into low BETA defensive sectors of the market. On Friday the big upside came from the pharma group.

The worst performing sectors were Energy (XLE), Financials (XLF) and Consumer Discretionary (XLY). Last week was a tough one for sectors with leverage to the global RECOVERY theme. Both Financials and Energy are the only two sectors broken on the TRADE duration. The Energy (XLE) was the worst performer today as another bounce in the dollar weighed on commodities and commodity equities. December crude on Friday settled ($0.63) at $76.83 a barrel.

The Consumer Discretionary (XLY) underperformed relative to the broader market, as Housing and Media stocks weighed on the ETF. The worst performing Media names were Gannett and CBS Corporation. The Oprah news clearly was influencing the performance of CBS on Friday.

Next to Energy the Financials are significantly underperforming. Over the past month the XLF is down 3.8%, while the XLE is down 4.7%. The Banking sector has generally led the group lower and put in a mixed performance on Friday. Although, once constant is the high RISK groups such as the mortgage insurers and the GSEs continue to underperform.

From a risk management standpoint, the ranges for the S&P 500, USD Index and the VIX are seen in the charts below. The range for the S&P 500 is 36 points or 2% upside and 1% downside. At the time of writing the major market futures are poised to open to the upside.

Howard Penney

Managing Director