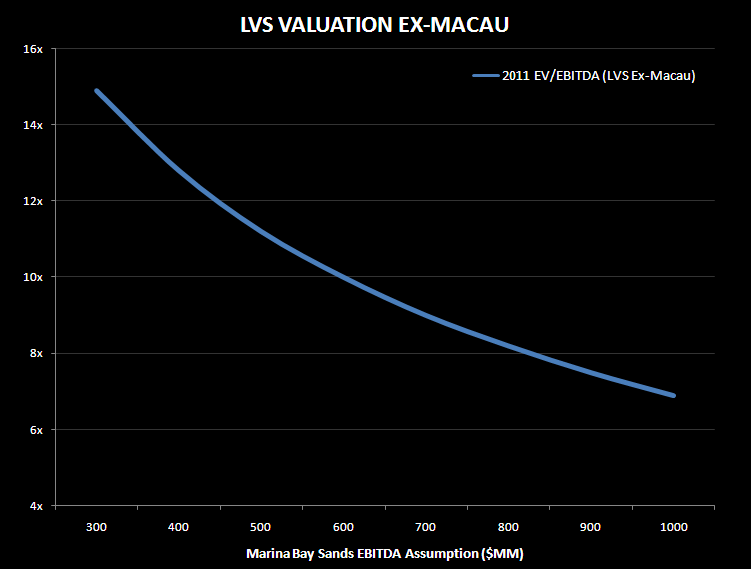

With Sands China priced, it all comes down to your Singapore assumption. EBITDA above $600 million drives the LVS ex-Macau below 10x 2011 EV/EBITDA.

Sands China priced, not surprisingly, at the low end of the range. At $1.34 per share (HK$10.38 on the Hong Kong Stock Exchange) and without the green shoe, total proceeds were $2.5 billion. Now that we have an idea at what the market values the LVS Macau operations, we can back out the implied value of "what's left" in the LVS empire - namely the US operations and, of course, the wild card that is Sands Marina in Singapore.

We think that there are two ways to look at LVS once Sands China has a publicly traded float:

- Backing out the minority interest in Sands China that LVS doesn't own - calculating the implied value of US operations + Marina Bay Sands + 70% of Sands China

- Backing out all the entire value of Sands China and seeing what the implied value for just the US and Singapore piece

At $16.35, LVS is trading at 11.6x 2011 EV/EBITDA and 9.7x 2012 EV/EBITDA. We need to look past 2010 because Marina Bay Singapore will not contribute EBITDA for a full year and Lots 5&6 in Macau won't contribute at all. The valuation actually looks attractive, especially considering that part of the valuation is in Macau where LVS pays no corporate taxes on gaming profits (at least for now). The debatable valuation range on the US operations is probably tight (8-10x). On the other hand, there is a lot of uncertainty surrounding Singapore since many of the gaming regulations have yet to be established and the government has made it pretty clear that they are more interested in attracting general tourism dollars rather than creating a new gaming mecca.

As we wrote about in "LVS: CREDIT OPTIONS AND OUTCOMES" on 2/28/09, it's hard to make an argument that there is much value in the US operations. So the value of "what's left" at LVS largely hinges on your opinion of how much EBITDA Marina Bay Sands can generate. If you believe that Marina Bay Sands can generate north of $600MM EBITDA, the implied stub valuation is not too expensive at 10x 2011E EBITDA.

For us, $600MM is the pivot EBITDA for Singapore. Getting LVS ex-Macau at under 10x 2011 EV/EBITDA begins to look attractive. We are currently projecting over $700 million of EBITDA for Singapore although we must admit we don't feel overly confident in that number. We remain concerned with the potential slow ramp of the business given the high likelihood of a low junket presence.