The U.S. stock market is within spitting distance of all-time highs.

Which begs the question: Can the market go higher? You bet.

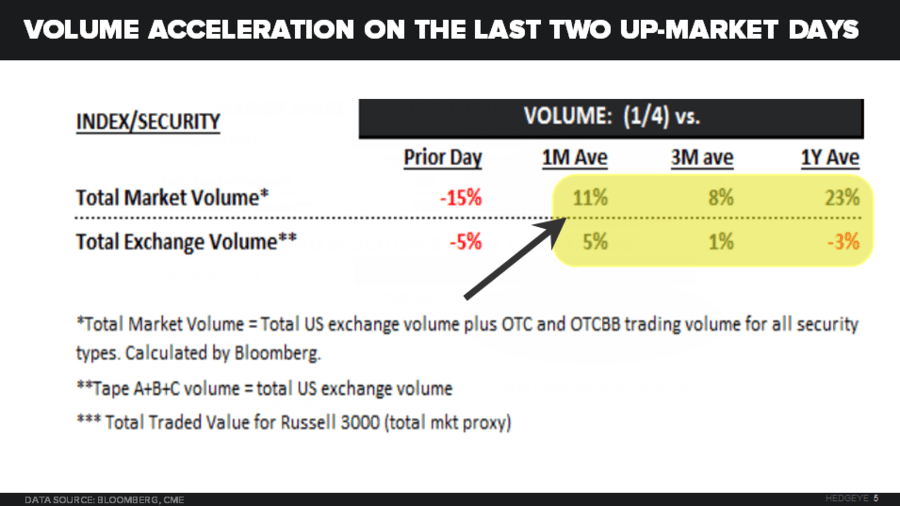

As you can see in the Chart of the Day below (from today's Early Look), equity market volume (the number of shares traded on U.S. stock exchanges) yesterday was up +11% versus its 1-month average and up 8% versus the 3-month average. The S&P 500 was up +0.6% yesterday. This follows increasing volume in Tuesday trading as well, when the market was up 0.85%. Here's the volume scorecard on that move higher:

- Trading volume (1/3) vs. 1-month average: +30%

- Trading volume (1/3) vs. 3-month average: +26%

What Accelerating Volume Means For Stocks

Think of accelerating volume (on up days) as a vote of confidence that the market can head higher. It's simple. If more investors are buying as the stock market heads higher that's bullish. Conversely, if volume accelerates on down days that means investors are selling in droves. That is very bad and very bearish signal.

Consider what happened during a two particularly trying weeks at the end of October and early November in which stocks fell -3%. Volume was consistently accelerating as investors headed for the door. On November 1st and 2nd, volume was up almost 20% versus the one-month average as stocks dropped -0.6% on both days.

Bottom Line

We're a far cry from those dismal days today. The U.S. economy is growing, stocks are heading higher and volume is accelerating. All of this bodes well for equities. We don't see an end to the 9-year bull market just yet.