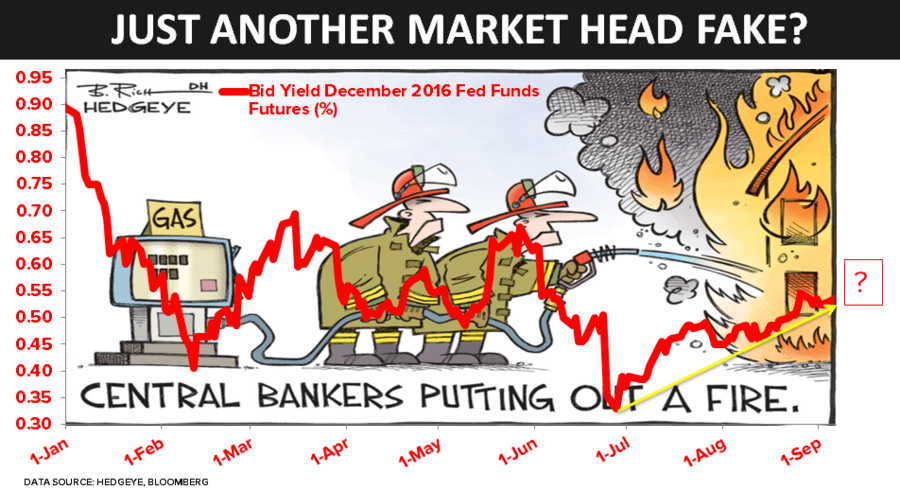

Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more.

...Yellen’s Fed is much shorter-term than that. If she does what the market is telling her to do right now (Fed Fund Futures dropped to 32% on a SEP hike), this will be her 6th pivot (hawkish-dovish-hawkish-dovish-hawkish-dovish), in 9 months.