Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye U.S. Macro Analyst Christian Drake. Click here to learn more.

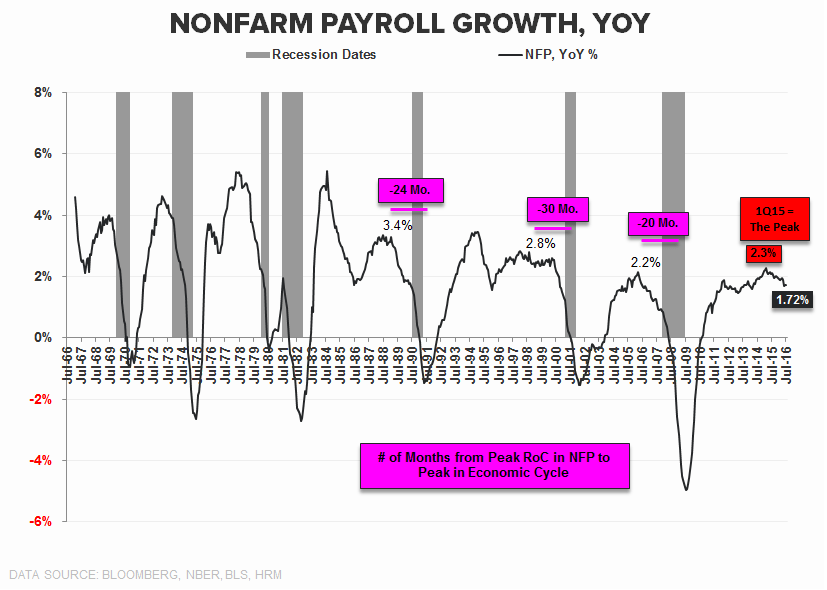

"...From a rate of change perspective, payroll growth will continue to slow from here.

The why is relatively straightforward:

- Employment growth is hostage to the law of large numbers and as the base gets bigger, an accelerating growth rate implies an ever increasing number of jobs. On an NFP base of 145M, the numbers get unreasonable quickly (i.e. you start needing to add 700K … 900K … >1M workers net on monthly basis to maintain the growth curve).

- Diminished slack and a tighter labor market. As the expansion matures and labor supply tightens, there are simply less people to hire and more competition."