Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more.

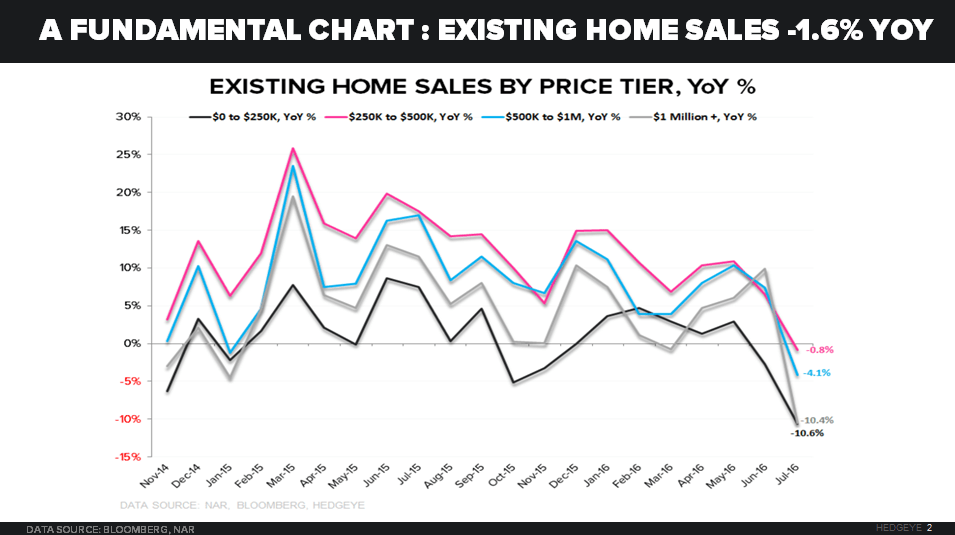

"... Notwithstanding the noise (Old Wall’s Media trumpeted New Home Sales like the Return of The Jedi, and barely mentioned #GrowthSlowing in Existing ones) I have a few contextual points to make about US Housing:

A) Existing Home Sales make up 90% of the US Housing market (vs. New Homes at 10%)

B) A -1.6% year-over-year decline is the slowest rate of change in 23 months"