Below are our analysts’ new updates on our ten current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this.

Please note that we removed Zimmer Biomet (ZBH) from the short side of Investing Ideas this week. We will send Hedgeye CEO Keith McCullough's refreshed levels for our high-conviction Investing Ideas in a seperate email.

IDEAS UPDATES

TLT | GLD | UUP

To view our analyst's original report on PowerShares DB US Dollar Index Bullish Fund click here and here for Gold.

We often get the pushback that "investors are bearish on the broader equity markets" and "the long-bond is now a crowded trade with little valuation upside." As Keith we wrote in our top-3 macro themes on Thursday morning, “long-term yields continue to track the rate of change in long-term GROWTH – get growth right, and I think you’ll get the UST 10-30yr right; from here to 1.63% is a good spot to be buying long-term bonds and their safe-yield proxies.”

Industrial production and capacity utilization data realized early in the week points to a continued deceleration in those respective growth rates. We haven’t been shy to call this an industrial recession.

The YoY growth rate in industrial production ticked up +20bps sequentially to -0.5%, holding in contraction territory for the 11th consecutive month. The growth rate is still slowing on a trending basis off the late-2014 peak, while commensurately accelerating on a trending basis off the late-2015 trough.

Capacity Utilization ticked up +50bps m/m to 75.9% in JUL, but the trending deceleration remains intact.

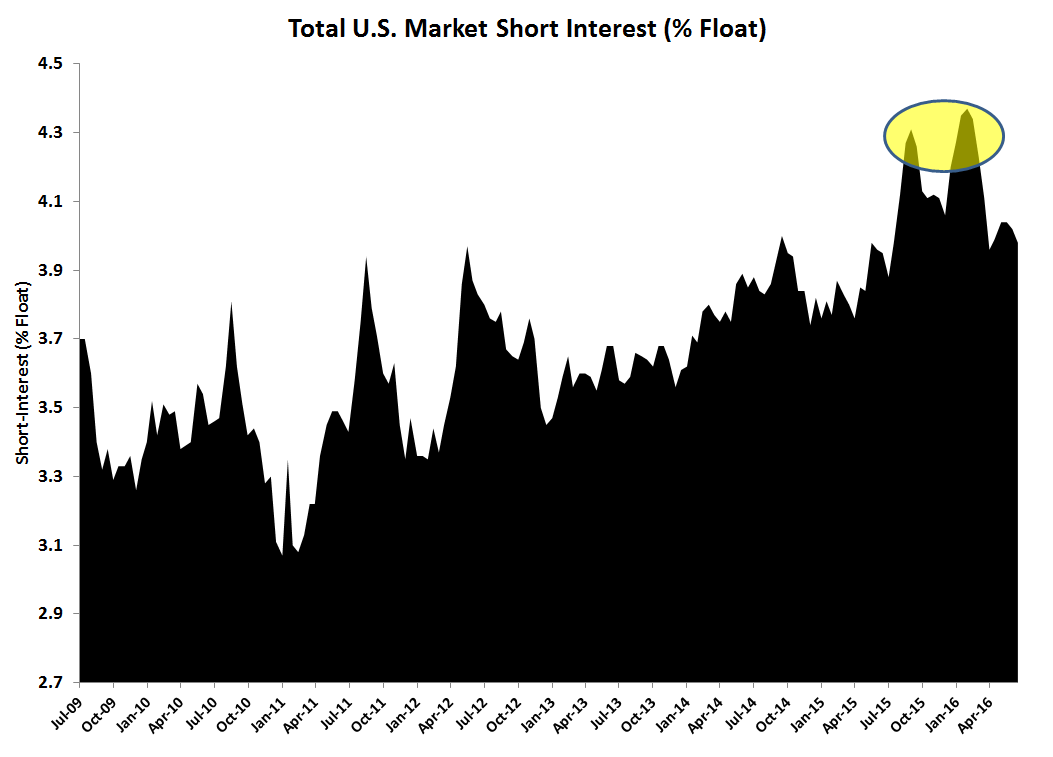

And as for the commentary that everyone is bearish on the S&P which is why it can’t move lower, well, everyone is not bearish on the S&P. It’s much more important to study how investors are actually positioned over listening to qualitative opinion.

Total U.S. market short-interest has been cut by 13% from the February lows and S&P net futures and options positioning (index+e-minis), while it’s been cut the last few weeks, is still +1.7x extended on a TTM z-score basis – this as we’re testing record low 2014 levels across various volatility metrics. Again, we’re much more comfortable with our #GrowthSlowing call over capitulating to market beta at all-time highs.

HBI

To view our analyst's original report on Hanesbrands click here.

Cotton prices have fallen over the last couple weeks from the YTD highs at the beginning of August. We should reiterate that our short call on Hanesbrands (HBI) is not based on higher cotton prices, but rather we think it's a company that is facing negative organic growth, at peak utilization, with peak margins, which is being forced to find additional growth via increasingly risky businesses at higher and higher multiples.

At HBI, cotton makes up 7% of COGS. The company hedges cotton out 6-9 months with the goal of providing time to adjust selling prices as much as possible to accommodate the input cost change. Including hedging and production process it takes about 4-5 quarters for price fluctuations to flow through to the P&L.

For HBI a 10% move in cotton price is about a 50bps impact to gross margin, or a 4% EPS impact. At a minimum we do not think cotton will head materially lower, which means the tailwind the industry has had for the past 3 years is gone.

LAZ

To view our analyst's original report on Lazard click here.

No update on Lazard (LAZ) this week but Hedgeye Financials analyst Jonathan Casteleyn reiterates his short call.

TIF

To view our analyst's original report on Tiffany click here.

Tiffany (TIF) reports earnings on Thursday August 25th. Yes, expectations are low, as is current sentiment in the market, but we think before the year is out we will see another reset to earnings expectations. This is what we know for certain headed into Thursday’s print.

- Comparable sales growth will be negative which will make the 7th straight quarter with negative comps.

- Earnings growth will be negative making 6 quarters in a row.

- Management will not raise guidance as there is a material 2nd half acceleration baked into the current plan.

As the core fundamentals continue to deteriorate, and we haven’t seen a clear plan from management in order to change the course of current trends. Not to mention we sit at the tail end of the economic cycle with luxury spending going negative for the first time in 5 years. At 19x unhittable earnings expectations, we’re still riding this on the short side.

LMT

To view our analyst's original report on Lockheed Martin click here.

Lockheed Martin (LMT) was down a hefty 4% this week ($254 per share from $265) primarily because of disappointment with Tuesday’s finalization of the numbers from the Reverse Morris Trust spinoff of its lower margin IT division to Leidos: Lockheed will end up repurchasing only 9.4M shares of stock versus projected 10M.

Investors should note that Friday’s price puts the stock back where it was exactly one month ago (+17% YTD) meaning that last month’s run up owed a lot to street expectations of the spinoff. Fundamentally, the main drivers of Lockheed’s revenue remain in place, if not improved. The F35 continues on its development track with the Navy version completing its final at sea development period.

The government released another $1B towards the Lot 9 production of 57 aircraft (now well over 50% complete) reducing LMT’s cash exposure used to keep suppliers going, pending conclusion of the now one-year-old negotiations for a final contract. Final contract terms are critical since the deal is to cover both Lot 9 and 10 and will become a basis for the approaching longer term block and multiyear contracts.

FL

To view our analyst's original report on Foot Locker click here.

Foot Locker (FL) reported earnings this week and ultimately delivered a great quarter, beating on the top and bottom lines. The near term results do not change our long term view on FL which is predicated upon an unsustainable financial model, and a mismatch between how much FL needs to spend on both the P&L (SG&A) and on PP&E to drive the business now that the retail distribution paradigm is changing for the first time in 40yrs. Specifically, Nike has been spending on building up a world-class e-commerce model for the better part of 8-years – basically this whole economic cycle – and we’re now starting to see the fruits of Nike’s investment, while FL must now compete with a partner who accounts for 70%+ of its business.

On the quarter itself, the revenue outperformance was particularly impressive for FL with the comp accelerating 180bps against a tougher compare. With the comp rate running negative as of the May call, this made for the biggest intra quarter comp acceleration during this economic cycle. The acceleration in the business in 2Q makes the Double Digits Full Year EPS guidance much more hittable, though we think the current Street numbers are a bit of a stretch.

On the negative side, we would note that the leverage in this model is looking less and less attractive. Meaning even when beating expectations like the company did on Friday, the margin upside has all but dried up, demonstrated by SG&A deleverage on a 5% comp. FL leveraged the 4.7% comp into 5% revenue growth and 6% EBIT growth. EPS was up 11% aided by the 4% y/y share count reduction.

WAB

To view our analyst's original report on Wabtec click here.

While the bull story continues to pin its hopes on an acquisition of a French manufacturing company (which we still think the deal will not go through in its current form) Wabtec's (WAB) high-margin aftermarket business is continuing to deteriorate as equipment continues to be pulled into storage. Add in weak rail volumes, poor railcar and locomotive orders and we continue to expect 2016 EPS ex-Faiveley below $4/share as the company’s core freight market enters a multi-year downturn.

HOLX

To view our analyst's original report on Hologic click here.

No update on Hologic (HOLX) this week but Hedgeye Healthcare analyst Tom Tobin reiterates his short call.