Our cartoonist Bob Rich captures the tenor on Wall Street every weekday in Hedgeye's widely-acclaimed Cartoon of the Day. Below are his five latest cartoons. We hope you enjoy his humor and wit as filtered through Hedgeye's market insights. Bob is on a much-deserved summer vacation. While he kicks back and relaxes, we're going into the Hedgeye Vault and highlighting some of his best work. (Click here to receive our daily cartoon for free.)

Enjoy!

1. The Land of Make-Believe (8/12/2016)

Central planners have the delusional idea that they can smooth economic gravity. That#BeliefSystem is breaking down.

2. We ❤ Gold (8/11/2016)

Gold is up 25% year-to-date.

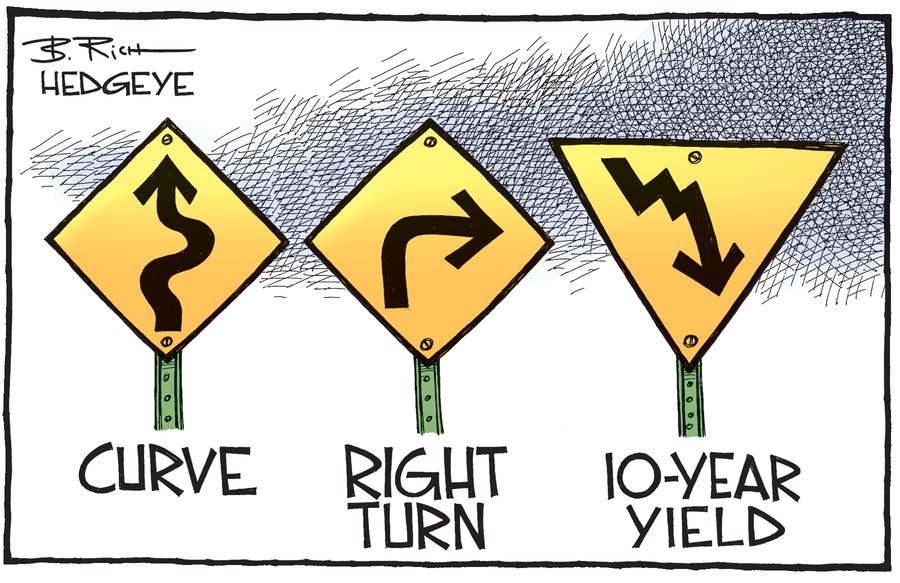

3. Sign of the Times (8/10/2016)

Ten-year yields, globally, were down across the board this morning. Got#GrowthSlowing?

4. Twilight Zone (8/9/2016)

One of our top three 3Q16 Macro Themes is #EuropeImploding.

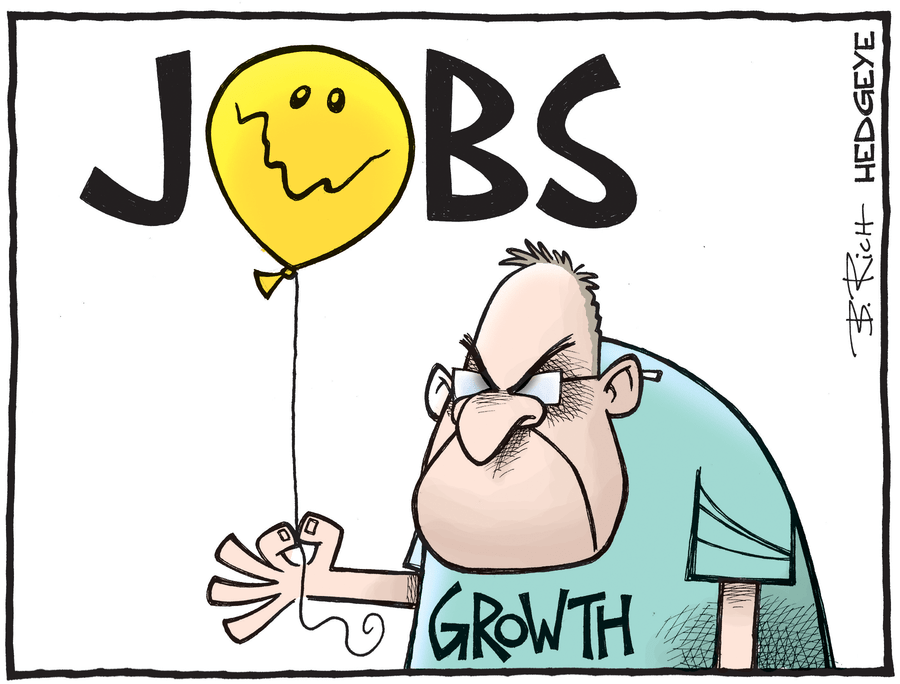

5. Employment Growth Slowing (8/8/2016)

While Wall Street trumpeted Friday's headline 255,000 jobs number as "good," the year-over-year rate of change continues to slow from 2.3% in February of 2015 to last week's reading of 1.72%.

Click here to receive our daily cartoon for free.