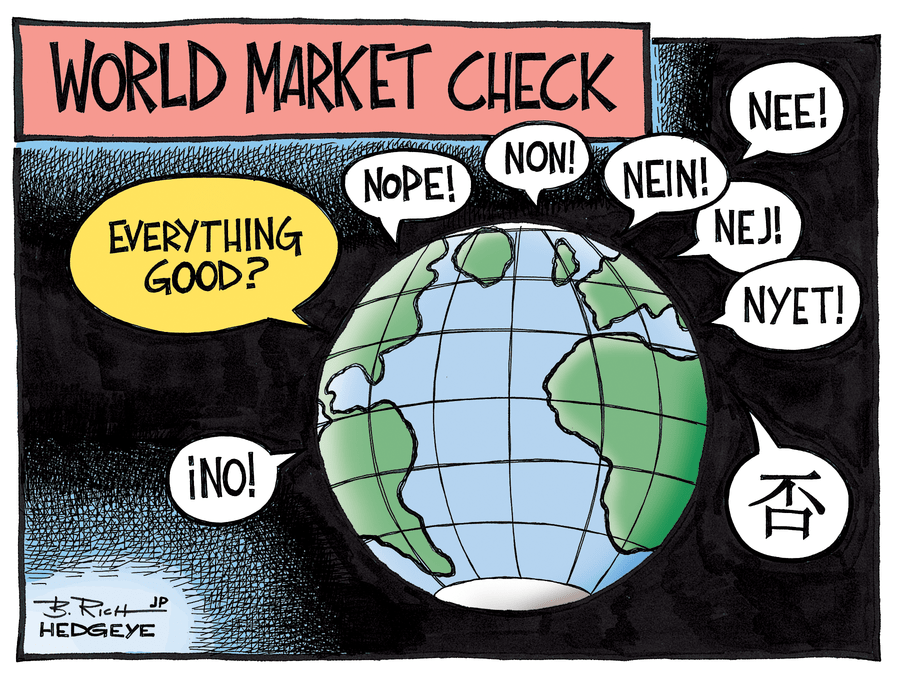

As the hopes and whims of investors swing wildly through markets, these delusions become increasingly disconnected from economic reality.

A case study in delusion: Japan. "No need and no possibility for helicopter money," BOJ head Haruhiko Kuroda said in a BBC Radio 4 program that was broadcast Thursday. “At this moment, the Bank of Japan has three options with quantitative and qualitative easing with negative interest rates."

The Yen jumped 1.1% on the news. Now the WSJ reports this broadcast was recorded in June and FX markets backed off.

This is all getting rather silly...

We reiterate today that the supposed catalyst "helicopter money or bust" is not a risk management process. Here's analysis from Hedgeye CEO Keith McCullough in a note sent to subscribers earlier today:

"Heli-Ben money hits a wall with Kuroda saying “no need or possibility for helicopter money” – doesn’t that suck. Reiterating short Nikkei as the Yen just popped +1.1% on that after failing to break-down through 108 vs. No support for Nikkei to 14,993."

While We're on Central planning nonsense...

ECB head Mario Draghi kept rates on hold today but had a number of innocuous things to say about the Euro-area economy, like this gem:

"Headwinds to economic recovery in euro area include outcome of UK referendum and other geopolitical uncertainties."

And then Draghi suggested that a "public backstop" would be "very useful" to help struggling European banks. Furthermore, Draghi added that the bad debts in Italy’s banking sector are a “very big problem.” Italian bank UniCredit popped 4% on the news (after falling more than -60% in the past year) along with other bank related stocks pushing the FTSE MIB index up marginally today.

McCullough dissects the latest out of Europe:

"Protracted recession pending in Europe? What’s the catalyst to get Italy, France, etc. out of one? Reiterating the short call on both European Equities (Germany, Spain, and Italy… in that order) and the Euro vs. USD (Italian stocks haven’t joined the helicopter party, -0.3% this am and -30% vs. where you could have bought them at this time last year)."

It's getting ugly out there...

"Turkey's president has declared a state of emergency for three months following Friday night's failed army coup," the BBC reports. "The emergency allows the president and cabinet to bypass parliament when drafting new laws and to restrict or suspend rights and freedoms." (For more analysis on what to expect out of Turkey, check out Hedgeye Potomac National Security analyst LTG Dan Christman USA Ret. "What Comes Next After The Failed Coup In Turkey.")

In COMMODITIES MARKETS...

The #StrongDollar ravaging continues.

Meanwhile, Here at home...

Equity markets are within spitting distance of all-time highs. But, as we've pointed out before, the recent stock market rallies have come on declining total market volume. Not good.

In these uncertain times, What do you buy?

On pullbacks... Gold (GLD), which has developed a seemingly antithetical correlation of 0.9 to the U.S. dollar over the last 30-days. Note: Gold has been working all year (and remains a Hedgeye Long call):

As our outspoken CEO Keith McCullough is fond of saying, "Risk happens slowly at first, then all at once."