Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye U.S. Macro analyst Christian Drake. Click here to learn more.

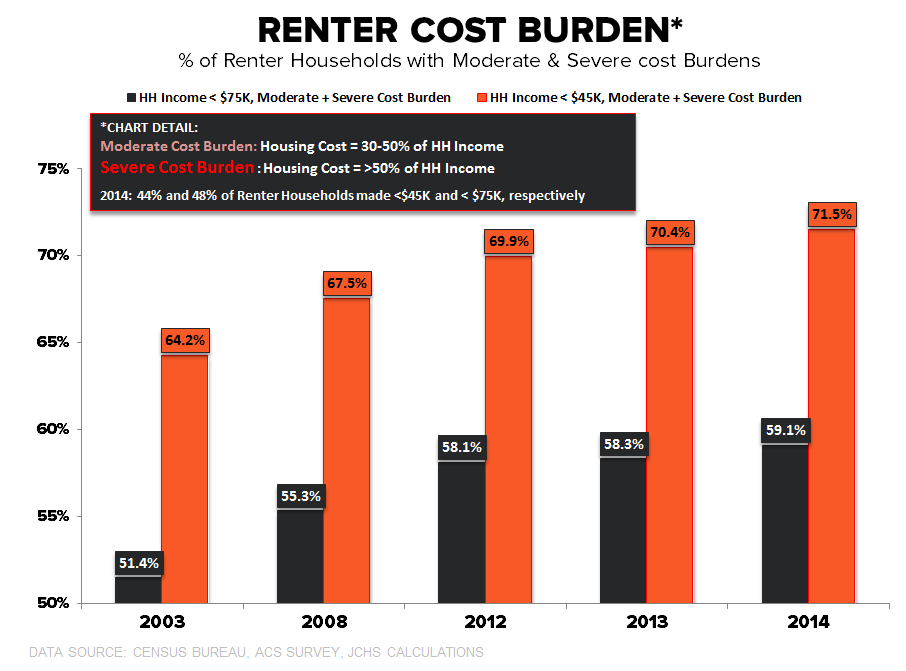

"... As can be seen in the Chart of the Day below, almost half of all renter households make less than $75K so the incidence of moderate and severe cost burdens is the prevailing reality for over 20 million households.

And as housing’s share of wallet grows, capacity for other discretionary consumption declines proportionally. Indeed, severely cost burdened households spend more on transportation costs and significantly less on Food, Healthcare and retirement savings."