Don't believe that the global economy is slowing?

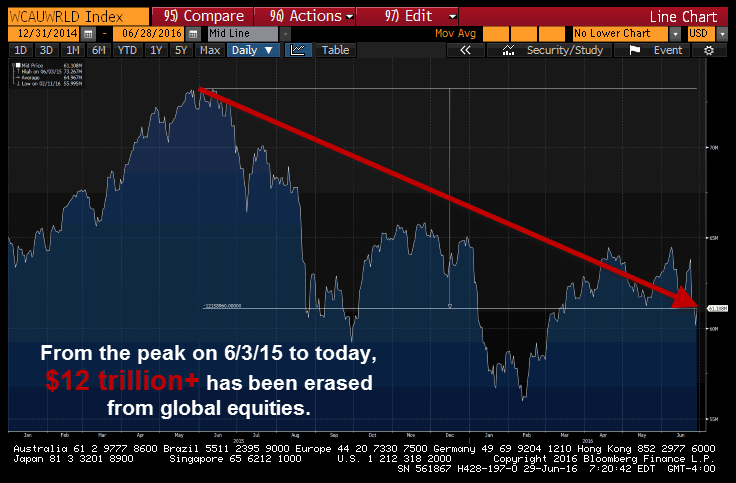

Since peaking last June, global equities have lost $12 trillion in market cap as of this morning. Take a look below at the Bloomberg World Exchange Market Capitalization index.

Yep. That's a 19.9% decline...one hair away from full-blown crash mode.

Here's a look at select equity markets around the globe and their drawdowns since then:

What's the big message here?

For starters, global demand hasn't bottomed ... and the outlook remains unequivocally bearish.