With the Pound getting pounded and the U.S. dollar rallying, below is an afternoon currency market checkup with a breakdown of the big movers in macro markets. Much is changing and investors are just now beginning to hold unelected bureaucrats to account for their ineffectual policies.

The obvious callout is the post-Brexit Tumble in the pound...

Hedgeye CEO Keith McCullough in a note to subscribers this morning:

"POUND – continues to crash, down another -3.4% vs. USD to $1.32 – signaling immediate-term TRADE oversold, finally – but this crash and the bearish TREND break-down in EUR/USD keeps the super-cycle (bullish) call for USD intact. There’s #Deflation risk in that."

The pound is down -12% versus the pre-Brexit vote high against the U.S. dollar:

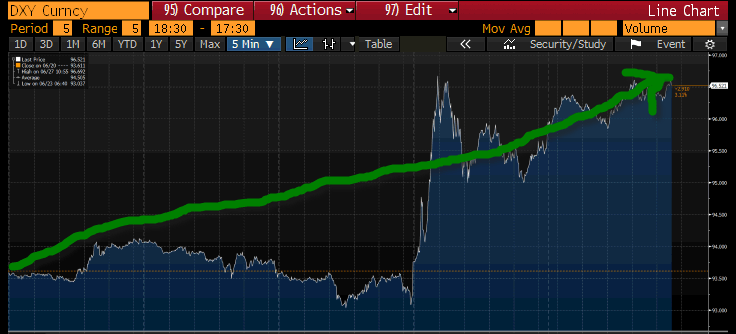

Meanwhile, the U.S. dollar index is up +3.2%, over the last five days, as investors flee European assets:

... That's also why the EURUSD is down -3.6% on the dollar strength:

What may be the most significant callout of the year, in currency markets, is Yen strength, a move in direct opposition to Japanese central planners' intent. The USDJPY cross is down -15% year-to-date, despite the BOJ's best efforts. In fact, Japanese government and BOJ officials met today to discuss how best to counteract Yen strength.

What's happening in Japan is perhaps most emblematic of our Q2 Macro Theme, outlining the breakdown in the central planning #BeliefSystem.

It's happening all over the world.

Bottom line: The jig is up. Investors are losing faith in central planners' schemes.