Below are our analysts’ new updates on our fifteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this.

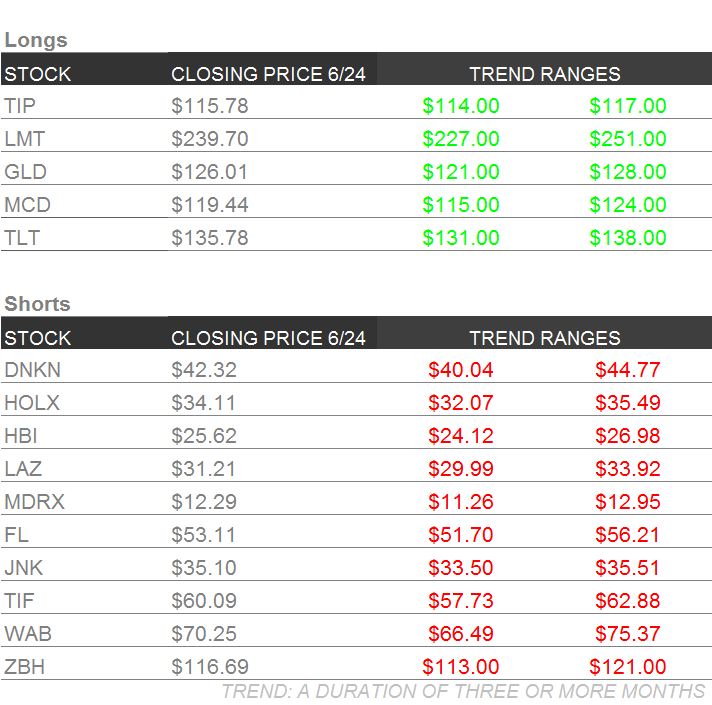

Please note that we added iShares Barclays TIPS Bond Fund (TIP) and Lockheed Martin Corporation (LMT) to the long side of Investing Ideas and removed Deere & Company (DE) from the short side. Hedgeye Potomac Senior Defense Policy Advisor LtGen Emerson "Emo" Gardner USMC Ret. will send out a full report outlining our high-conviction long thesis next week. Please see below Hedgeye CEO Keith McCullough's refreshed levels for our high-conviction Investing Ideas.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

TIP | TLT | GLD | JNK

To view our analyst's original report on Junk Bonds click here, here for TIPs and here for Gold.

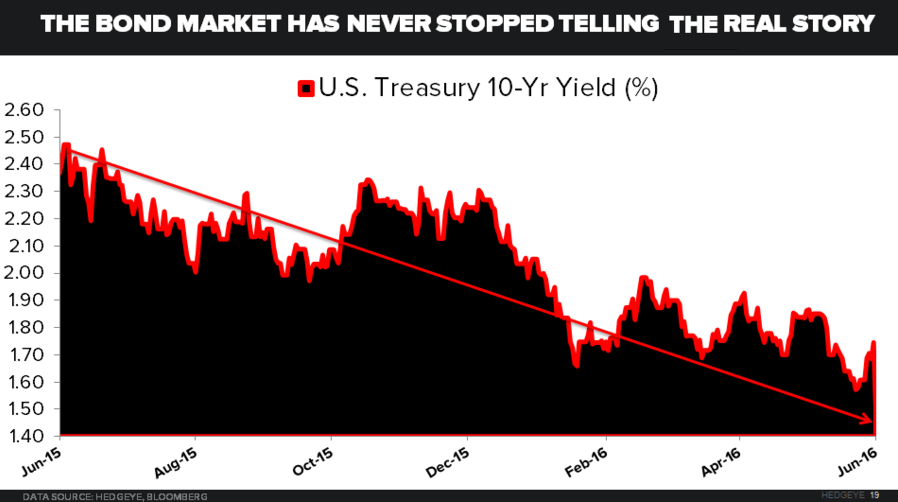

We caught a lot of flak for not being long the S&P 500 during the melt-up to cycle high forward multiples despite keeping one of the most alpha generating equity positions of the year in being long Utilities (XLU) and short Financials (XLF) for a majority of 2016.

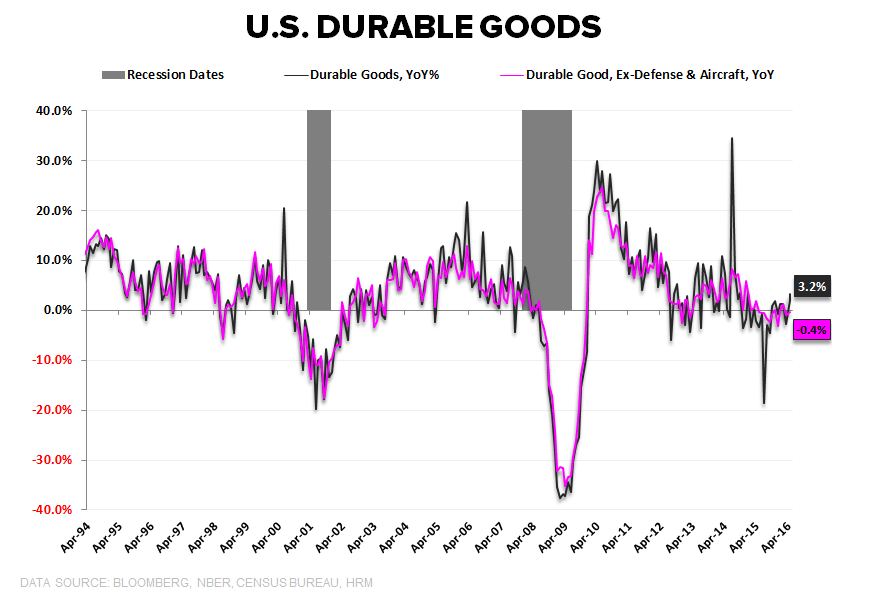

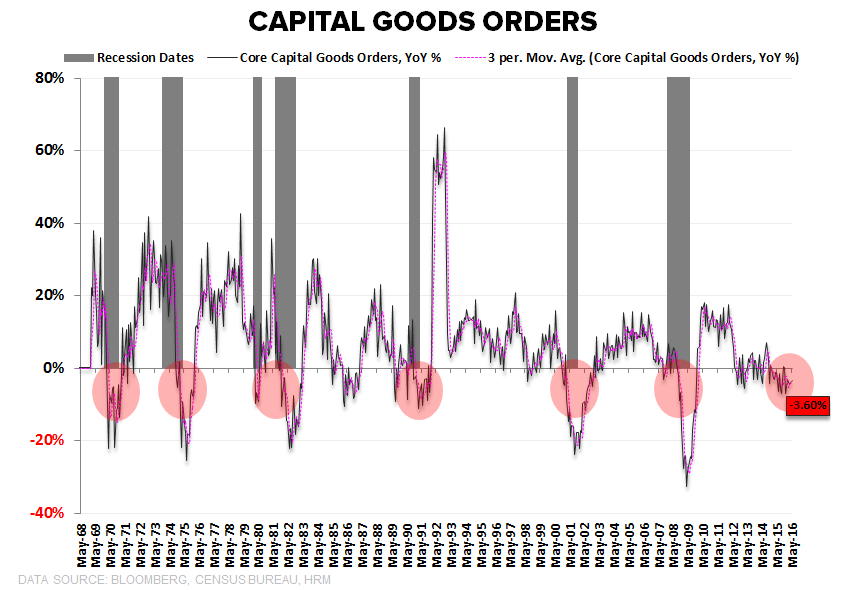

Looking at other markets (yes there are other markets), maybe being long the Long Bond (TLT) for almost two years and sitting long of Gold (GLD) was too boring for some people, but when you look at the chart below, you have to ask yourself what you’re buying in broader equity indices with an ongoing earnings and cyclical slowdown. The second quarter of 2016 is setting up as the 5th consecutive quarter of Y/Y earnings declines for the S&P 500, the longest streak since the quarter ending in Q3 2009.

Employment and consumption has already rolled and Friday’s durable and capital goods prints confirmed that the industrial recession is ongoing. We realize Brexit was the dominant headline and it was yet another reason to steer clear of risk assets instead of rolling the bones on open the envelope risk.

So again, looking at the chart below, can we grow into this multiple, which is at a cycle high and a level not seen since the tech bubble? Unlikely, given the current economic set-up, which is why we have avoided high beta growth names trading at unrealistic multiples and opted for good ole’ TLT. There is a time to buy growth, but not when our cyclical view continues to be confirmed.

In Great Britain, the people voted for freedom and not for the broken promises that central planners can bend and smooth economic gravity. The #BeliefSystem is breaking down and despite the fact that every central banker around the world was out Friday talking about “stepping in.”

As we’ve mentioned, the bond market has gotten the #GrowthSlowing call right all along:

We added Treasury Inflation-Protected Securities (TIP) to Investing Ideas this week for a couple of reasons:

- We want to be long of continued growth decelerating and inflation picking up from a GIP modeling perspective into the back half of 2016. TIPS are a great way to play both of these views along with our GLD (reflation) and TLT (growth slowing) positions

- The policy response globally will continue to be, currency devaluation and monetary easing with the intent to create inflation, and we take their commitment to this very seriously

Enjoy your weekend and sleep soundly with your Gold…

MCD

To view our analyst's original report on McDonald's click here.

No update on McDonald's (MCD) this week but Hedgeye Restaurants analyst Howard Penney reiterates his long call.

DNKN

To view our analyst's original report on Dunkin Brands click here.

Dunkin Brands (DNKN) management spoke at the Jefferies conference this week and it raised concerns (among bulls) about how the top line is trending. Paul Carbone, DNKN CFO stated, “I don’t think the competitive environment is getting any tougher or more difficult. I don’t think it’s letting up. I don’t think it is going to let up.” He went on to say, “If we look over time [at competitors], gas and convenience are becoming a much bigger option for the consumer.”

“The consumer has a lot of places to go to and a lot of choices and I think that’s going to continue. And I think what people are realizing, certainly the convenience stores, is they can discount coffee and still make a significant margin on it just because of the margin makeup of beverage.”

This opening remark by Paul was overly bearish, and although DNKN was already trading down in the early part of the session, his commentary propelled the stock down for the remainder of the day, ending down -2.8%. Paul continued to say that he believes competition in general is a bigger headwind than how the consumer feels. Said in another way, their biggest headwind is somewhat out of their control, which is what other people that sell coffee do to grow their business.

Towards the end of his remarks, Paul spoke briefly on their decision to remove bundles. The main reasons continue to be menu simplification, and some price lift. Paul said they continue to get great feedback from franchisees and consumers, we aren’t believers yet, time will tell if it’s truly a well-accepted move.

WAB

To view our analyst's original report on Wabtec click here.

No update on Wabtech (WAB) this week but Hedgeye Industrials analyst Jay Van Sciver reiterates his short call.

ZBH

To view our analyst's original report on Zimmer Biomet click here.

It will be interesting to see if the BREXIT matters to consensus estimates across our Healthcare universe. We’ve clearly been passing through a period of optimism about growth in the medical economy across our client contacts, who have been highlighting the positive commentary (likely ignoring the negative) that they’ve been hearing from companies and sellside analysts. While Zimmer Biomet (ZBH) put up a good Q1 revenue number, the total increase in revenue estimates extends well out to 2019.

Meanwhile, slowing/declining economic data such as Durable Goods, Employment, and temporary employment, as well as slowing healthcare series such as Healthcare Job Openings, Medicaid enrollment, Obamacare enrollment, suggest more downside than upside risk this year and beyond. Historically, the data suggests sellside sentiment and estimates are tied tightly to stock price movement on a lag. ZBH is hardly down today on the massive disruption caused by the Brexit, but there is a credible case that falling stock prices and rising volatility, on top of slowing economic data, might be the catalyst for real downward pressure in demand. Clearly the optimism baked into the shares is high, which means the downside risk is high as well.

HBI

To view our analyst's original report on Hanesbrands click here.

As Hanesbrands (HBI) has been making its latest acquisitions, the debt level has been increasing. This is a divergence compared to Maidenform and DBA, where leverage has actually declined in the years those deals closed.

In 1Q16 HBI borrowed about $740mm against its revolver and used a significant portion to buyback stock. In May, to fund the acquisitions, the company issued three new bond series and increased debt another $560mm.

Given the downside we see in both organic growth and margins, increasing leverage at this point in the economic cycle isn’t proper risk management.

MDRX

To view our analyst's original report on Allscripts click here.

With one week left in 2Q16, we have yet to get any new press released deals or contract renewal/expansion announcements from Allscripts (MDRX). This is surprising as Q2/Q4 tend to be the strongest bookings quarter. While deals can often be pushed all the way to the last day of the quarter, the trend so far is not looking good from a bookings perspective. In fact, if we don’t get something by the end of next week, it would be the first quarter in the last 5-years where there have been no announced deals.

This supports our view that the HCIT market is slowing post-stimulus and that replacement activity is accruing to the top vendors in the space, specifically Epic and Cerner in Inpatient and athenahealth and eClinicalWorks in ambulatory. We also believe that much of the replacement activity in 2015 was driven by the sunset of McKesson’s Horizon EHR, which is an opportunity that is quickly drying up.

Unless management completely changed their philosophy around press releasing new deals (highly unlikely), we think that bookings have to be a concern for management and also for those long the stock given a tough prior-year comparison and consensus estimates that call for 10% sequential growth in bookings.

TIF

To view our analyst's original report on Tiffany click here.

Tiffany (TIF) has missed revenue expectations in 5 of the last 8 quarters. In addition to weakening demand for Tiffany product, a significant driver is overly optimistic sales expectations from management via guidance.

At the same time the Street has been very wrong on gross margins. Margins have only missed twice and actually beat expectations by about 150bps in each of the last 2 quarters. The general rule of thumb in retail is that you can have at least one of these fundamentals perform well. You either sell fewer items, but at full price which boosts margins at the expense of sales, or you can sell a lot of items by cutting price which boosts sales at the expense of margins.

Tiffany however, because of its luxury brand tilt, won’t directly play the cutting game. Unfortunately, it means you don’t have control over the top line and can lose a lot of fixed cost leverage when demand slows, as it has been lately.

We think earnings expectations remain too high over the next 12-18 months, and expect to see more misses on the revenue line as Tiffany demand remains weak and the US consumer continues to slow. Margins are likely to stay relatively healthy, but earnings will surprise to the downside.

LAZ

To view our analyst's original report on Lazard click here.

Lazard (LAZ) shares were down -10.7% Friday following the referendum of the United Kingdom's membership of the European Union. Hedgeye Financials analyst Jonathan Casteleyn has been warning about the Brexit risk embedded in the shares for a while now. Here's his LAZ update from Investing Ideas on April 30th:

"Furthermore, Lazard has one of the largest industry exposures to European activity and with the June 23rd BREXIT vote on the docket, there is a dearth of current deal making until corporate boards understand whether Great Britain will remain an EU industrial member. Both the M&A business and the firm’s asset management business continue to operate near peak margins which means there will be plenty of downside compression as activity continues to dry up. The stock is still highly recommended by most analysts that cover the stock and we are one of the only firms with a cautious view on shares."

On the broader LAZ thesis, Hedgeye CEO Keith McCullough wrote in Real-Time Alerts this week:

"Here are 3 reasons why Casteleyn remains The Bear on Lazard:

- The M&A cycle peaked last year, in our view, and historically new restructuring revenue takes 2 years to offset M&A losses

- The asset management business is working on a slightly better quarter solely on market appreciation, as our data outlines no organic growth in 2Q16 thus far

- LAZ shares remain a value trap. Consensus estimates need a substantial haircut and financials won't comp up for at least the balance of 2016"

FL

To view our analyst's original report on Foot Locker click here.

A specific pressure point on SG&A for Foot Locker (FL) is wages. Management handles the "Are you seeing wage pressure?" question by describing the commission piece of store employee compensation which brings employees well above the minimum wage.

Consider the following:

- We just completed an inflationary period when wages grew minimally. The chart below shows the spread in footwear PCE growth - Average wages, and SG&A leverage that FL has recognized. The point is that leverage of labor costs is easy when footwear ASP and sales are growing rapidly and wage growth is stagnant. It won’t be easy when market wages grow and footwear sales slow.

- FL's employee commissions are derived from sales performance. The company has been posting mid to high single digit comparable sales growth for several years. We're sure employees are pleased with their compensation in that environment. But what happens when comps slow to low single digits or flat, like they did in 1Q. Will employees still be pleased with that compensation level as retail market wage averages are rising.

- Wal-Mart is putting wage pressure on the industry. We don’t think its enough to say it doesn't matter 'our' average wage is higher. An FL employee probably expects to make a certain % more than a Wal-Mart employee. When they see people making more for doing the same job the always did at WMT, the reaction would be to expect the same at FL.

We think SG&A rate hit its trough in 2015 and as that reverts back to more reasonable levels, it will be a significant negative lever on earnings.

HOLX

To view our analyst's original report on Hologic click here.

Here are the key takeaways on Hologic (HOLX) from our original stock report:

- While there are other elements of Hologic’s business, historical regression analysis shows that forward multiple is most dependent on the growth rate in the Breast Health (42% of sales) business or 3D Tomography sales. Simply put, get Breast Health growth right and get the stock right.

- Over the intermediate term, we see little that can drive further upside to the stock, outside of an acquisition (which is a risk to our thesis). While we expect growth to continue to come under pressure, our call for -30% downside is likely to play out over the next 12-18 months.

- Slowing 3D Tomo Adoption – Hologic stopped disclosing penetration for 3D mammography, providing the last unit counts and market share in September 2015. For the September 2015 period, the company disclosed 28% penetration into their installed base. Our s-curve for 3D indicates share was 32.4% as of 9/27/2015, which agrees with HOLX management statements.

- #ACATaper – While more difficult to quantify, we believe the Affordable Care Act was a tailwind to HOLX’s diagnostic business. After years of being uninsured, new enrollees were top consumers of diagnostic tests that Hologic offers, such as HPV and PAP. That customer base is now slowing.

- We expect most of our downside to be realized over a 12-18 month time period, as the gap between our Breast Health estimates and consensus widens over the course of 2017.