Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more.

"... So if they the British don’t exit… and:

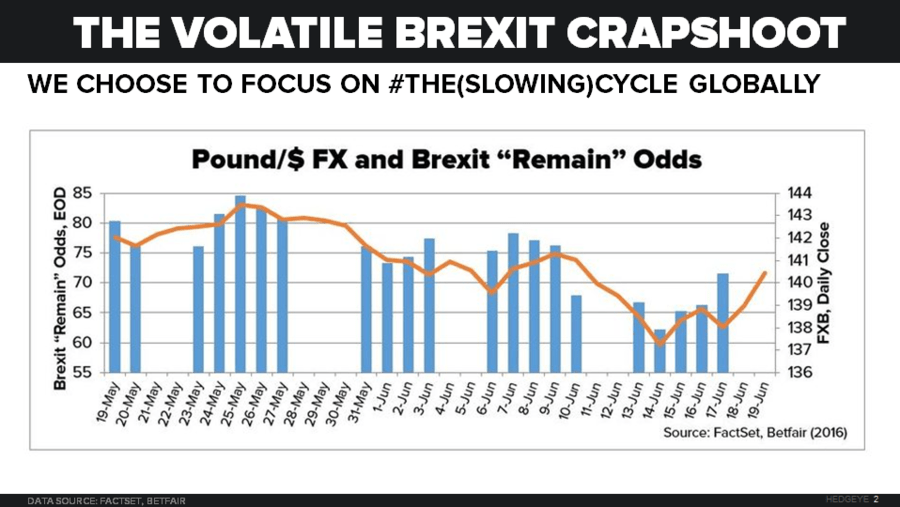

- The British Pound ramps right back to where it’s been multiple times this year ($1.46-1.47)

- The FTSE rips right back to intermediate-term @Hedgeye TREND resistance of 6335

- All equity markets worldwide go straight up …

What could possibly go wrong?

Nothing, obviously. Until the causal factor (worldwide cyclical and secular #GrowthSlowing) on why most things political that are American, Chinese, European, Japanese, etc. aren’t dying starts to get reported again, that is…"