Got #Deflation?

That's the latest macro market read through, explaining why equity markets in Australia and Russia puked and the 10yr Treasury yield headed lower. In other words, it was a classic Dollar Up, Rates Down day.

Where do we go from here?

Is the evolving trend #Deflation or #Reflation? That's the question of the month...

On an immediate-term trade basis, yesterday's selloff triggered oversold in a number of shorts in Real-Time Alerts. Here's additional insight via Hedgeye CEO Keith McCullough in a note sent to subscribers earlier today:

"U.S. Treasury 10yr yield at 1.57%. Yep. Closing in on 2015 lows but rates are oversold ahead of Yellen’s 4th pivot (hawkish to dovish to hawkish to dovish) in 6 months as #EmploymentSlowing becomes obvious."

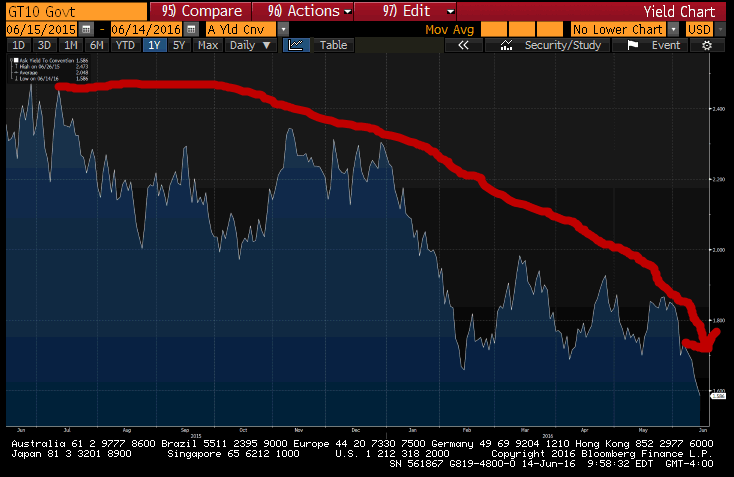

Take a look at a chart of the tumbling 10yr Treasury yield. (Note: At the start of 2016, the 10yr Treasury yield was 2.25%.)

Click to enlarge.

Meanwhile in equity markets...

"Dollar Up, Rates Down – that is the #Deflation Risk On – and that’s a big reason for the oversold signal in Global Equities this morning – Reflation sensitive countries (Russia -3%, Australia -2%) and Reflation Risk sector exposures have corrected, hard, from our USD oversold (Energy Overbought) signal last week."

Next catalyst in the #Reflation vs. #Deflation debate? Fed head Janet Yellen will give an update on the FOMC's latest thinking on Wednesday...

It's perverse, but it's reality. The Fed's pivots from hawkish to dovish throughout the year have perpetuated either reflation or deflation.