Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more.

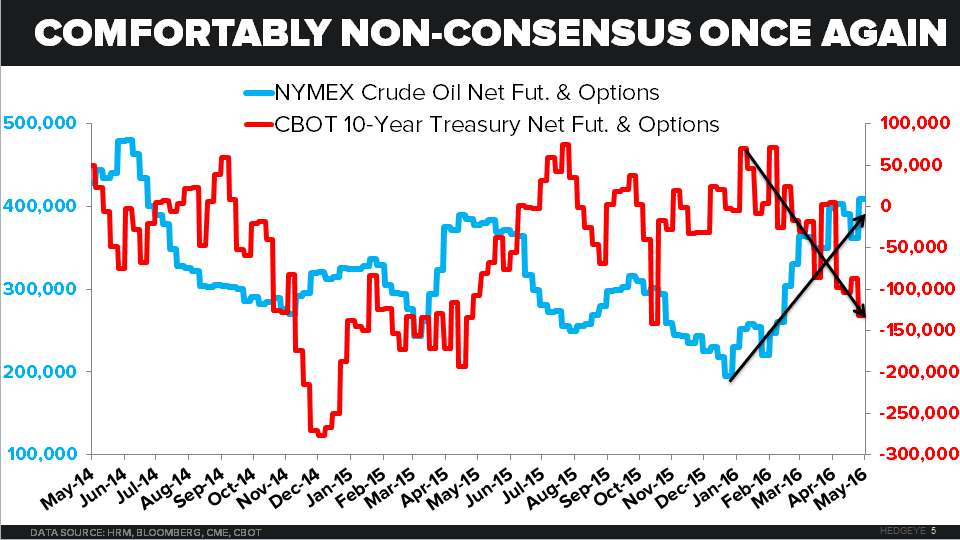

"Another reason not to worry (be happy) if you have Hedgeye’s macro view, is that the crowd still doesn’t agree with us. Here’s what Consensus Macro positioning looks like from a CFTC futures and options perspective:

- SP500 (Index + E-mini) net LONG position of +9,630 contracts = +1.83x 1YR z-score

- Crude Oil net LONG position of +408,569 contracts = +1.93x 1YR z-score

- 10YR Treasury net SHORT position of -131,565 contracts = -2.33x 1YR z-score

For those of you who are new to following us, we measure current macro positioning across multiple durations relative to where the positioning has been in the past. Anything plus or minus 2x tends to be a great contrarian indicator."