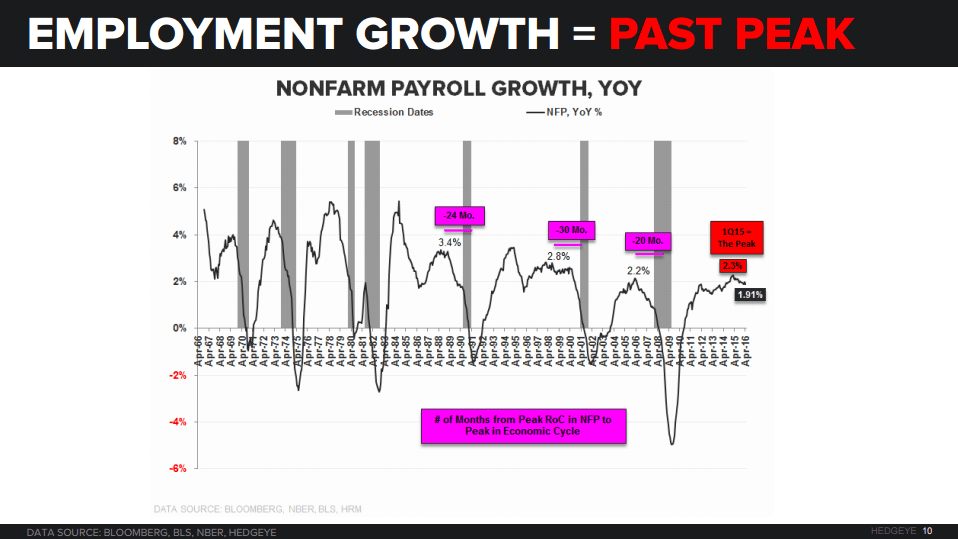

Despite financial media headlines trumpeting "Everything You Need To Know" about today's jobs report, the Old Wall media missed the most obvious story of all. Digging a tiny bit deeper reveals the real story. Job growth peaked in Febraury 2015. It's been all downhill ever since.

Sure, we all know job growth slowed to 160,000, well below the 200,000 number Wall Street economists were predicting.

Blah, blah, blah...

Digging just a tiny bit deeper reveals the actual story.

Job growth peaked in Febraury 2015. It's been all downhill ever since.

Here's the detailed breakdown:

And finally, a message from our outspoken CEO Keith McCullough. What you should have owned heading into today's #LateCycle Jobs Report.