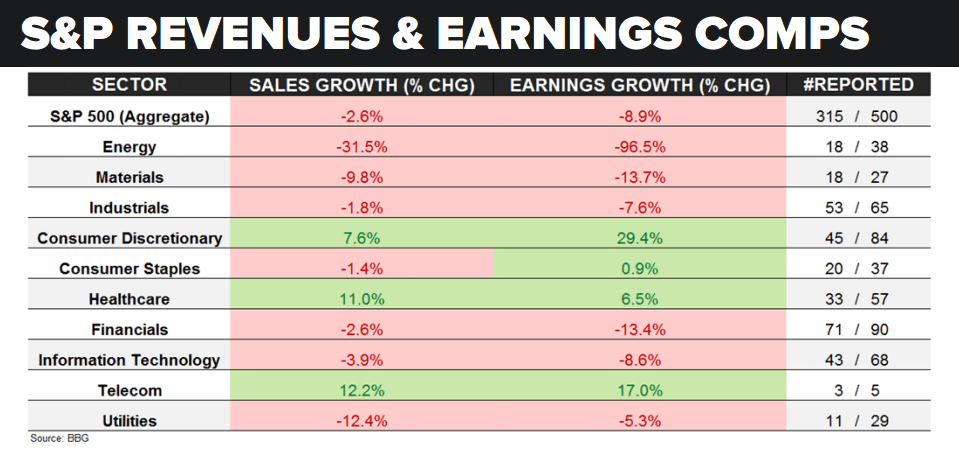

For Q1 Earnings Season to-date, 315 of the 500 companies in the S&P 500 have reported results:

- Aggregate SALES growth is down -2.6% year-over-year = worst level of the season so far;

- Aggregate EPS growth is down -8.9% year-over-year = worst level of the season so far;

- Industrials and Financials have EPS down -7.6% and -13.4% year-over-year, respectively;

- Energy earnings are down -96.5% year-over-year