The Hedgeye Macro team has been predicting dour U.S. economic growth for over a year. Our contrarian economic call has been pretty close to spot on. Meanwhile, this #GrowthSlowing reality has consistently confounded Wall Street consensus.

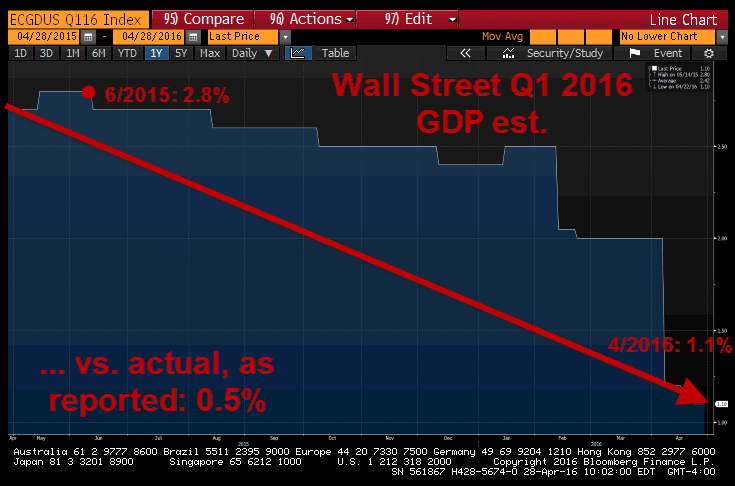

As you can see in the chart below, Wall Street economists were predicting almost 3% growth for Q1 2016 last April.

To be clear, Old Wall consensus was forced to ratchet back its inflated estimate to 2.5% in February 2016 ... all the way down to 1.1% most recently. Of course, the initial Q1 GDP reading today came in at 0.5%. That surprised even us to the downside, as we have been predicting 1%.

Will this slowdown persist?

Wall Street doesn't think so. The consensus estimate for Q2 2016 is a (drum roll please)...

2.3%

Meanwhile, here at Hedgeye we're predicting 0.3%.

Who do you believe?

Watch Hedgeye Senior Macro analyst Darius Dale explain why we're so bearish in the video below: