Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more.

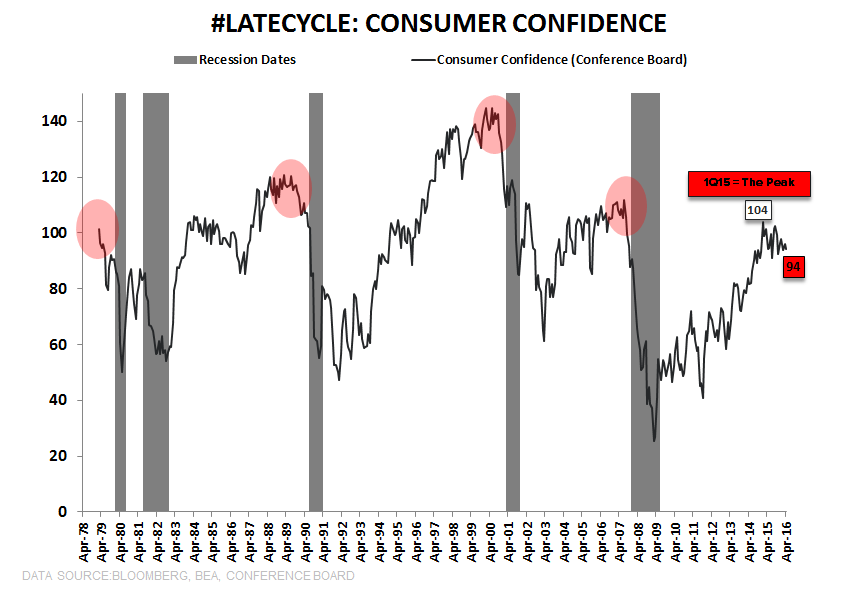

"... While most Americans don’t own stock market funds and Fed fueled “reflation” indexes anymore (yeah, the 2000 and 2008 cycle peaks did leave some crazy people cautious), a lot of Americans own single stocks like AAPL, NFLX, and GOOGL.

That’s why I think it’s going to be a lot harder to stop Consumer Confidence from doing what it always does after the economic, profit, and stock/credit market cycle peaks. See Chart of The Day – it takes the elevator up during the cycle, then it crashes."