Editor's Note: In this complimentary edition of About Everything, Hedgeye Demography Sector Head Neil Howe discusses why consumer spending on home improvement is outstripping GDP growth and the key demographic trends behind this shift.

WHAT’S HAPPENING

Three years ago, in a report called “The Boom in Home Remodeling,” I predicted that this was an industry about to take off. Now, it is airborne. Total spending on home improvement, well above $300 billion (and perhaps hitting an all-time high in 2016), continues to grow faster than GDP.

What’s more amazing is that the industry has expanded in the face of a crumbling housing market. Residential construction spending plunged a whopping 60 percent from peak to trough during the Great Recession. Home improvement spending’s fall? Just 13 percent.

In housing, single-family homes (not multi-units) have lagged the most in recent years. But in home improvement, single-family is the faster horse.

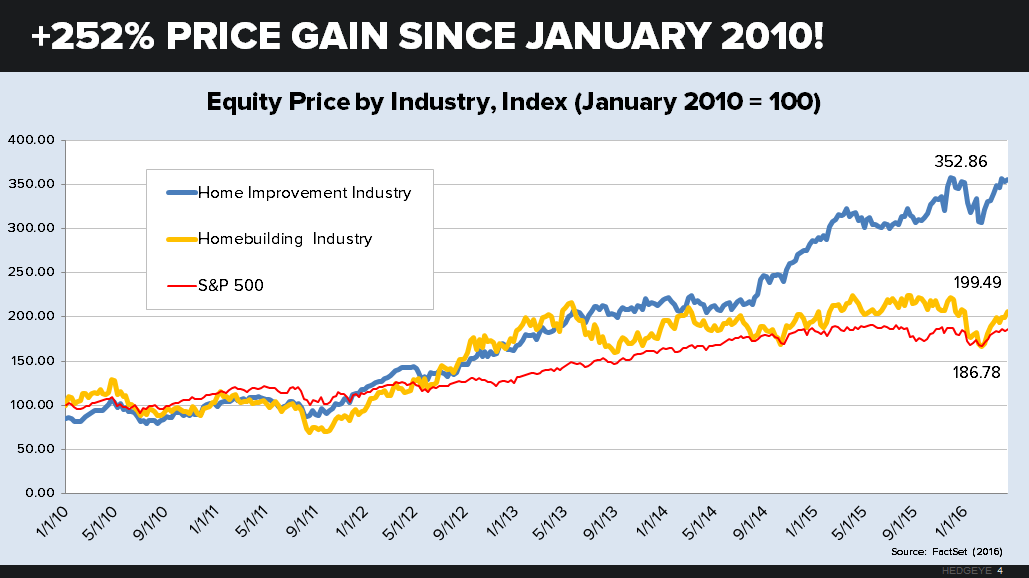

Equity prices in the industry reflect this boom—and the big chains are really riding the wave.

Lowe’s stock prices have more than doubled over the past four years. Home Depot shares have nearly tripled in value. Lowe’s plunked down $2.3 billion to acquire the Canadian giant RONA. And thanks to home services platforms like Pro.com, even more industry revenue gets funneled to the big guys.

WHY IT’S HAPPENING: DRIVERS

The rising average age of homes. While sprawling infrastructure projects once lowered the average age (and created new housing demand) by demolishing wide swathes of residences, those days are long gone. About 63 percent of the nation’s houses are at least 30 years old, up from 47 percent in 1995.

Today’s homes, moreover, are better constructed, allowing for indefinite improvements rather than knocking down and rebuilding. Thus, in some ways, home remodeling is actually replacing new home sales.

Falling mobility rates. A dwindling share of Americans move each year (a trend that kicked off in the 1980s). Falling mobility is partly due to an aging population and partly due to lower mobility at each age. More and more homeowners are in their current properties for the long haul—and are incentivized to spend on home remodeling.

Economic recovery. Homeowners who put off large discretionary projects during the Great Recession finally have the cash to take on those projects. Discretionary spending on remodeling is on the rise for the first time in a decade.

Generational change: aging-in-place Boomers. Boomers account for almost half of all dollars spent on home remodeling.

They’re aging in place, working longer in retirement, and putting up their adult children who are just fine sticking around the nest.

Generational change: DIY Xers. Most Gen-Xers will gladly save money by buying an imperfect or under-finished home—and then fixing it up on their own over time. They value personalization and often trust their own talents more than those of a homebuilder. In home remodeling (as in any other area of their lives), Xers wonder why they should call a professional when they can do the job themselves.

Generational change: cohabiting Millennials. Every Millennial who lives with mom or dad is one less buyer of a new home and one more excuse to remodel an existing home.

Even when they do move out, Millennials tend to stay nearby—enabling them to get parental advice or funding when remodeling their own homes or to help their parents when remodeling theirs. When Millennials remodel, they need someone to show them the way: Lowe’s recently released how-to tutorials on Vine for Millennial DIYers. N2Care even builds “granny pods” so that Millennials can have their aging parents within reach.

BROADER IMPLICATIONS

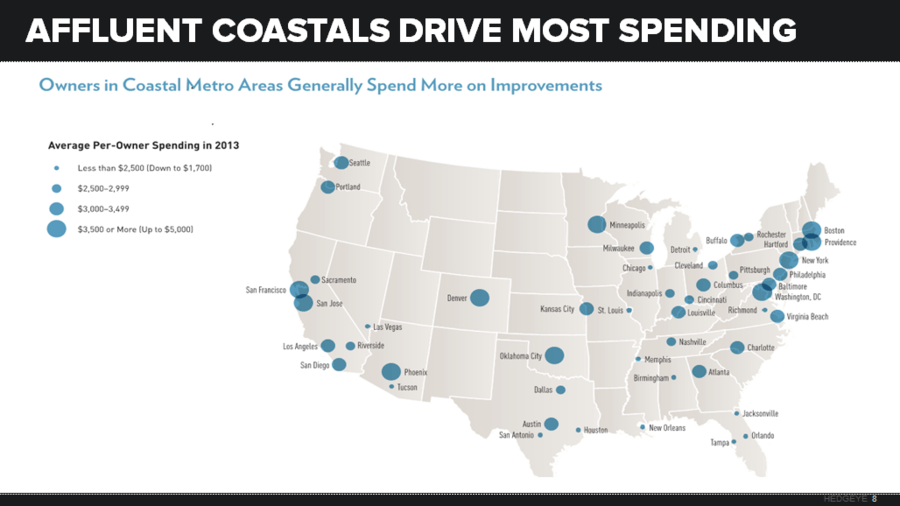

Affluent Boomer demand is fueling the industry’s growth. High-end Boomers unfazed by the Great Recession have spent heavily on home improvement even while banks foreclosed on younger and poorer consumers. Affluent coastal metro areas in the Northeast (in cities like Boston, New York, and Washington, D.C.) and in the West (Seattle, San Jose, and Phoenix) continue to be hotbeds for these big spenders.

Airbnb property owners are renovating their rented spaces. Private residences are taking over a growing chunk of the accommodation market. Homeowners who never had to worry about hotel industry regulations are now rebuilding stairways, constructing windows, and adding insulation to bring their properties up to code. Not to mention the cosmetic upgrades (like repainting and installing new countertops) designed to boost appeal.

Home remodeling firms are betting big on technology. Lowe’s and Microsoft have teamed up to create an in-store augmented reality experience that will allow shoppers to “try out” different cabinets, finishes, and more before buying. IKEA has created an online VR app that allows website visitors to customize a sample kitchen. And Home Depot carries scores of smart home products, from learning thermostats to precipitation-driven irrigation systems.

TAKEAWAY

Remodeling firms should be mindful of the generation they’re targeting:

- Boomers are building onto their homes to make room for the kids (and grandkids). They also need “universal design” accessibility upgrades, from wheelchair ramps to widened hallways.

- Xers spend heavily on no-frills DIY. This generation is the most price sensitive.

- Millennials want high-touch (as well as high-tech) services. They are looking for an expert to show them the way.

For more, watch Neil Howe in the associated About Everything video.