“Whoever fights monsters should see to it that in the process he does not become a monster. And if you gaze long enough into an abyss, the abyss will gaze back into you.”

-Friedrich Nietzsche

Last night in the Democratic debate between Hillary Clinton and Bernie Sanders, we had a good old fashioned brouhaha. The Brooklyn Brawler version of Bernie Sanders showed up and, in truly fitting fashion with the NHL playoffs just starting, dropped his proverbial mitts going after Clinton. Fortunately for Clinton and her supporters, it is too little too late.

As it relates to the National polls, Sanders is basically in a statistical tie with Clinton. Still, she has an almost insurmountable lead in delegate count. Currently, including super delegates, Clinton has 1,758 and Sanders has 1,069, meaning she only needs 32% of the future delegate to clinch the nomination. So inasmuch as Clinton might be feeling The Bern, her path to the nomination is almost assured.

On the Republican side, as we’ve known all along, the race is likely going to come down to the wire and could very well result in a contested convention. Currently, Trump has 743 delegates while Kasich and Cruz have 688 combined. To clinch the nomination ahead of the convention, Trump will need 57% of the remaining delegates. It is certainly possible that he accomplishes this, but it is also far from an easy path and if it does happen it's going to be troublesome for the GOP.

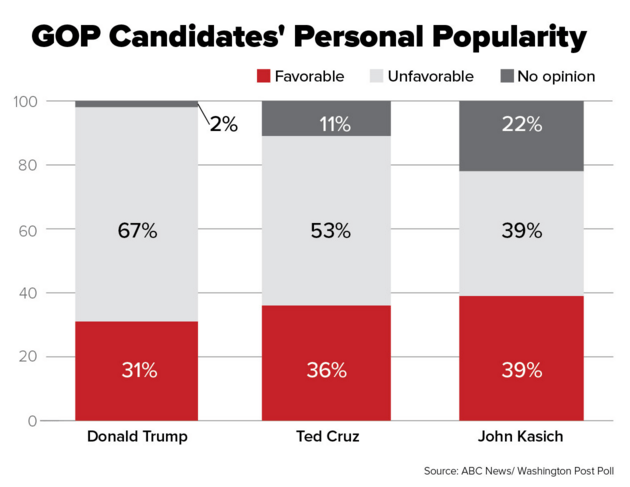

Even though a SuperPac led by Karl Rove is now making noise that Trump could beat Clinton, the fact remains that in head-to-head polls Clinton lambasts Trump by more than 10 points. The issue with Trump is his favorability ratings, which are, to put it simply, very unfavorable. According to a recent poll by ABC, almost 67% of the population views Trump unfavorably. Only former Klu Klux Klan leader David Duke has had higher unfavorable ratings as a Presidential candidate.

One thing we can all be certain of is that the political brouhaha we saw last night is only likely to accelerate heading into the general election this fall, especially if it comes down to Trump versus Clinton.

Back to the Global Macro Grind …

The notable “positive” economic news that came out over night was that Chinese growth was inline at +6.7% year-over-year. This is a sequential slowdown from the 4th quarter of 2015, which grew at +6.8% y-o-y. And as we show in the Chart of the Day, this continues the ongoing trend of slowing growth in China and is the slowest quarterly growth rate in seven years.

On the truly positive side, March industrial production in China was +6.8%, which was better than consensus and a sequential increase from February. March retail sales were also better than expected at +10.7% year-over-year. The truly blow out number in the Chinese data released overnight though was on government spending. Specifically, for the month fiscal spending was up 20.1% year-over-year!

As we’ve seen in the U.S., governments can outspend their revenue for a long, long time, so this massive growth in government expenditures isn’t necessarily a bad thing just yet. But we should still note that fiscal revenue was up only 7.1% year-over-year and the gap between fiscal expenditures and revenue was more than $500 billion yuan for March. No matter how you slice it, that’s a lot of yuan in deficit spending.

Meanwhile in Japan, the central bankers are, wait for it, considering expanding ETF purchases. You know you are down a deep dark hole of central planning when the tool that your central bank is considering using is to buy more ETFs. Although, given the recent ratcheting down of growth rates in the U.S. by various regional Fed banks, perhaps the days of Janet calling up her trading desk and getting long a few $100 billion in SPOOs is not far off. (Incidentally, the Bank of Japan already owns roughly 50% of the Japanese ETF market, but who's counting.)

Speaking of buying equities, one leg of the bull market thesis on the U.S. stock market went away in Q1. Specifically, the number of companies buying back stock fell to the lowest level since 2012. That said, there was still more than $182 billion in announced buybacks in Q1. Unfortunately, the amount of buybacks is set to drop more dramatically in line with corporate cash flow generation, which is likely to be flat in Q2 and down in the back half of the year.

One area of the economy which is definitely in a full blown recession is what we commonly call the Old Wall and specifically the revenues and earnings of the traditional investment banks. This morning, Bloomberg highlighted Goldman Sachs and the story is dire. The consensus revenue estimate for Goldman for Q1 is down -37% year-over-year!

This is also not a Goldman specific story by any stretch of the imagination as the revenue and earnings of its peers are on similar trajectories. In a year when politics are garnering most of the headlines, perhaps the larger watershed moment is the rapidly shrinking revenues of the Old Wall. Rest assured, though, Hedgeye continues to hire, so if you have any reformed Old Wall analysts that are looking for a transparent and accountable platform, have them email me at .

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.68-1.82%

SPX 2035-2091

VIX 13.00-19.40

USD 93.81-95.31

YEN 106.94-111.17

Oil (WTI) 38.36-43.99

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research