Editor's Note: In this complimentary edition of About Everything, Hedgeye Demography Sector Head Neil Howe discusses why "we’re entering a new era in which simplicity — not choice — is the hallmark of a cutting-edge brand."

WHAT’S HAPPENING

For the last half-century, America has fallen into a growing love affair with choice. It blossomed in the 1980s with supermalls, megamarts, and big-box retail, and amped up further in the 1990s by promises that you could always “have it your way”—even if that meant choosing your way through thousands of sizes, colors, styles, and tastes.

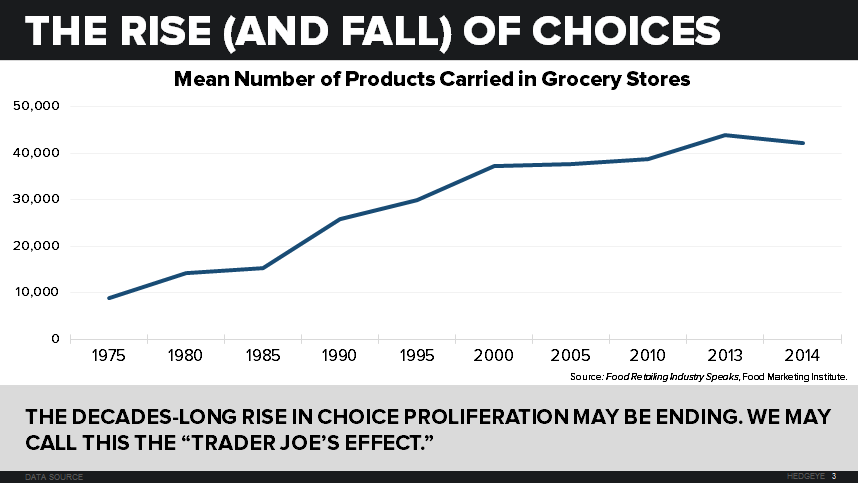

Today, Starbucks offers a mind-boggling 87,000 different beverage blends. The average American supermarket in 2014 carries nearly five times more items than in 1976.

But apparently, this romance is cooling. A countermovement toward simplicity is underway.

Look at some of these trends:

- Last year, Walmart reduced its average number of store displays by 15 percent.

- British grocery chain Tesco slashed its inventory by 30 percent.

- Paintmaker Glidden drastically thinned its color palette from 1,000 to 282.

- Procter & Gamble reduced its range of Head & Shoulders shampoos by nearly half.

Other changes aim to streamline the decision-making process. Tesco now groups typical meal ingredients together to save shoppers time. Sites with large inventories like Netflix offer recommendations to nudge users along. Travel companies like Expedia and Four Seasons Hotels curate high-end bundled vacations.

We’re entering a new era in which simplicity — not choice — is the hallmark of a cutting-edge brand (think Apple, Tesla, Chipotle, or Google’s home page). And a clutter of endless choices is now a symptom of a troubled brand (think JC Penney, McDonald’s, or Yahoo’s homepage).

WHY IT’S HAPPENING: DRIVERS

Choice fatigue

In his paradigm-shifting 2004 work, The Paradox of Choice, psychologist Barry Schwartz wrote that, beyond a certain point, “choice no longer liberates, but debilitates.”

When choice builds up, consumers are bogged down. The average American now makes 70 decisions a day. Should we really spend so much time worrying about what to order from Starbucks?

Schwartz cites research (on products such as jam, chocolate, and 401(k)s) showing that consumers faced with fewer options are actually more likely to settle on one.

Growing desire for authoritative brands

Faced with endless choice, consumers often feel that companies don’t care about their time — or, even worse, that companies don’t understand their own products enough to know which one is clearly superior. Americans today want brands that they trust will give them what they want without choosing. They want brands that cut down on options, effectively deciding for the consumer.

Generational change

When choice was shiny and new, Boomers were all for it. In response to a society that wallowed in Pleasantville sameness, young Boomers pushed for a bigger range of choices that allowed them to live life on their own terms and express their inner values.

Generation Xers followed suit. They learned to rely on themselves from an early age and equated choice with survival. Letting institutions choose for you was unthinkable. More options meant more freedom.

For Millennials, however, unlimited choice offers diminishing returns. When faced with countless options, this generation fears “missing out” (FOMO) on the best one. Millennials trust their favorite brands to pre-select the best products for them. They want the authoritative, in loco parentis brands that Boomers rebelled from. They’re relieved when their employer offers an opt-out default benefit plan, because they feel someone cares enough to recommend a “best” course of action.

BROADER IMPLICATIONS

Businesses should break their inventory down into manageable chunks. Retailers with diverse product lines can limit choice simply by separating items into categories, such as brand, color, size, or flavor. E-tailers should offer robust search and filter functions, while highlighting some (but not too much) useful information about each product.

Millennials in particular appreciate companies that pare down the field for them. Default options are often characterized as paternalistic—yet this can be a positive attribute in the minds of young consumers. In scenarios with high trust and low knowledge (think health care, tourism, and retirement savings), fewer choices can be reassuring.

TAKEAWAY

If you’re in search of the next cutting-edge brand:

- Don’t look for the firm that only knows how to proliferate option clutter.

- Do look for the firm that knows how to simplify the complex — and augment its value by boldly choosing for you.