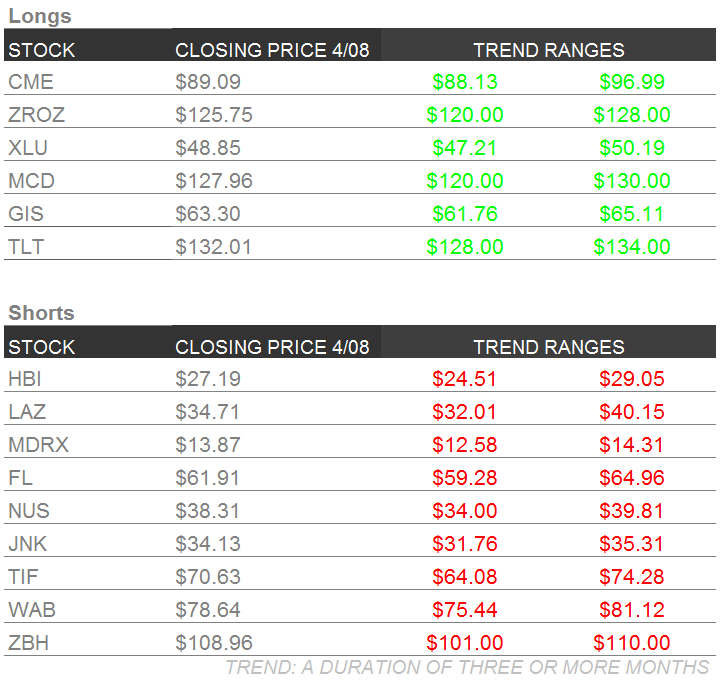

Below are our analysts’ new updates on our fifteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this. Hedgeye CEO Keith McCullough’s updated levels for each ticker are below.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

TLT | XLU | ZROZ | JNK

To view our analyst's original report on Junk Bonds click here, here for Utilities and here for Pimco 25+ Year Zero Coupon US Treasury ETF.

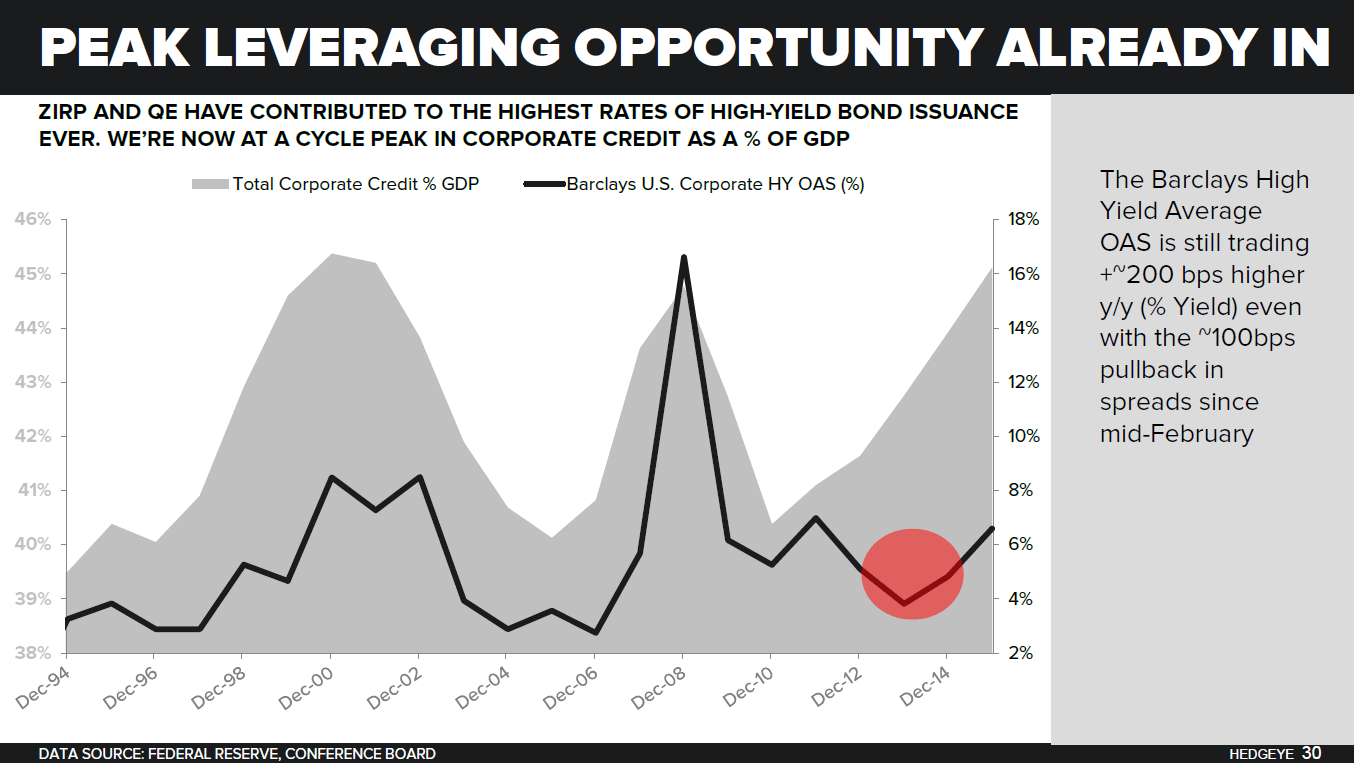

We outlined our expectation and outlook moving into Q2 on Thursday in our quarterly macro themes presentation for institutional clients. The first of the three themes was labeled #TheCycle:

“With the recessionary industrial data ongoing, employment, income and consumption growth decelerating, corporate profits facing a 3rd quarter of negative growth and Commercial and Industrial credit tightening, the domestic economic, profit and credit cycles are all past peak and continue to traverse their downslope. With this cyclical backdrop, the U.S. economy faces its toughest GDP comp of the cycle in 2Q16”….

The takeaway is that the economy faces a difficult GDP comp (growth rate) in Q2 within the continued late-cycle slowdown. That's why our favorite sector for U.S. #GrowthSlowing, Utilities (XLU), remains the best performing sector year-to-date, up 12.9%, versus 0.2% for the S&P 500.

If you want evidence that “profit and credit cycles are all past peak” take a look at the problems faced by less creditworthy borrowers:

- There were 4 more corporate defaults this week

- Year-to-date, there have been 40 corporate defaults, which is the highest level since 2009

- 14 of these defaults have been in oil & gas and 8 from metals, mining, and steel

- 34 of these corporate defaults have been in the United States

This credit cycle update came despite the 10 year Treasury yield declining from 2.25% to start the year to 1.72% currently. In performance terms, that translates into Long Bonds (TLT) +9.5% and Pimco 25+ Year Zero Coupon US Treasury ETF (ZROZ) +15.0% YTD.

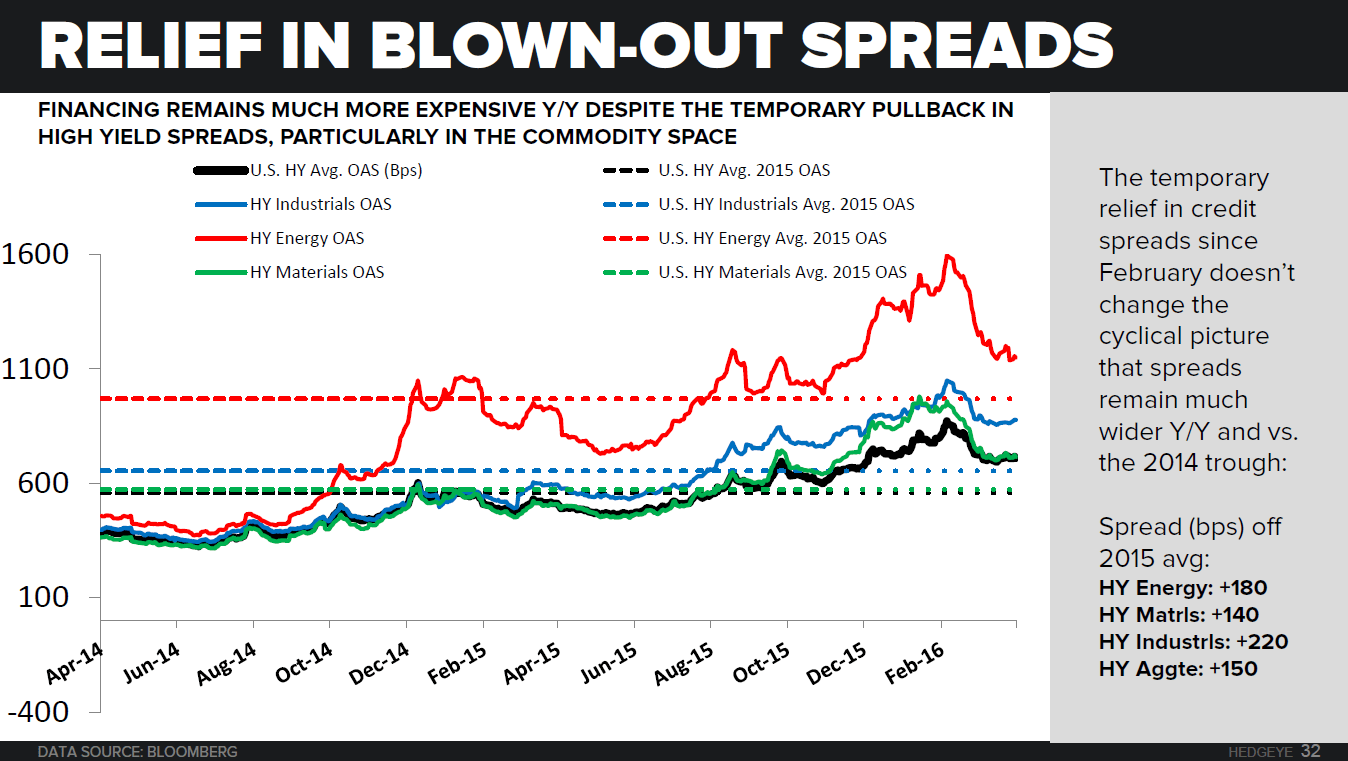

While Junk Bonds (JNK) may be essentially flat on the year, after a pop from the February lows, we continue to advise that you steer clear of the aforementioned bulleted risks (40 defaults!). With regard to relief in high yield credit spreads from the February highs, we want to call-out the fact that credit spreads are still much wider than 2015 averages and well off the 2014 lows in spreads and cross asset volatility.

As a result of the widening in spreads at peak earnings, it’s no surprise that high yield issuance is down -61% Y/Y YTD and CMBS is down -43% Y/Y YTD. Once this train gets going (the backside of the credit cycle), it doesn’t typically reverse. That's a cyclical reality.

MDRX

To view our analyst's original report on Allscripts click here. Below is an excerpt from a recent institutional research note on Allscripts (MDRX) written by Healthcare analysts Tom Tobin and Andrew Freedman.

MDRX | THOUGHTS ON THE NETSMART DEAL

Takeaway: Deal makes little strategic sense given core market overlap, Netsmart's small presence within health systems and lack of a clear end game.

intent and end game...

Allscripts announced a Joint Venture with GI Partners to acquire a 51% stake in Netsmart from Genstar Capital. Netsmart is a provider of EHR and other IT solutions to the behavioral health and post-acute care market. Based on the structure of the deal and what we know about Netsmart, we can't help but view Allscripts' role as more than a liquidity vehicle for GI Partners' inevitable exit. We think the deal makes little strategic sense given the core market overlap, Netsmart's limited share in health systems and lack of clear end game. Management is looking for a way to engineer top-line growth and appease activist shareholders... but if the turnaround story is in full force, then why not buy back a ton of stock?

Faced with market share losses, a looming slowdown in EHR spending and a declining stock price, management is under pressure to find new avenues for growth. At this stage in the 'turn around' story, the biggest mistake Allscripts could make would be to pursue a large acquisition of a competitor. Not only would it result in more integration problems that the new management team has spent years correcting, but it would also mark a deviation in strategy that would likely scare away existing customers. In this context, the Netsmart deal makes sense as it limits the integration risk and, unlike a traditional JV structure, allows the economics to flow through the P&L. However, we believe this will prove to be a short sighted move that adds little in the way of shareholder value long-term.

OVERLAP IN CORE MARKET

With the exception of the post-acute offering, Netsmart competes in most of the same product categories as Allscripts. Netsmart has an EHR (myEvolv) and PM system that targets behavioral health providers, but those providers could just as easily use Allscripts Pro or athenahealth. Netsmart also has a HIE solution (Allscripts dbMotion), a suite of payer solutions (Allscripts Payerpath) and care coordination offering. As a result of this overlap, the JV and Allscripts have entered into non-compete agreements, which effectively limits the addressable market and cross sell opportunity of both Allcripts and Netsmart.

small presence within health systems

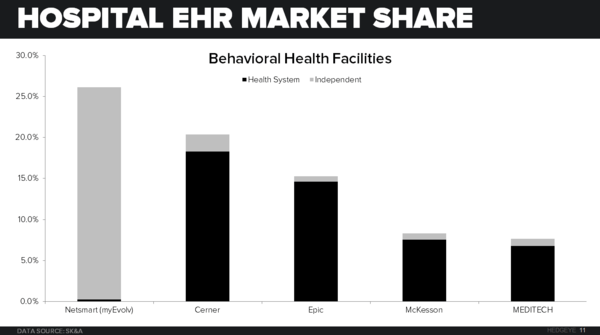

While we appreciate the importance of having a comprehensive post-acute and behavioral health offering in a fee-for-value world, we also appreciate the preference among CIOs to have an integrated solution across the continuum of care. Behavioral Health facilities owned by Health Systems comprise 75% of the market, of which Cerner and Epic control 65%. Meanwhile, Netsmart has little-to-no market share among health systems, but commands 30% share of independent hospitals. It is our expectation that a large portion of remaining Independent facilities will be acquired by Health Systems that will likely rip and replace Netsmart with their own system.

What is the end game?

GI's end game and motives are clear. GI will likely seek to exit their investment sometime in the next 3-5 years. For Allscripts, however, the end game really comes down to three options:

- Double Down - Acquire Netsmart Outright

While it may look like an attractive option on paper, in practice it will likely be another integration disaster. Also, any cross-sell opportunity would be limited by the overlap in product offerings and quality of the Netsmart install base. From a cost perspective, management would be forced to allocate resources to support yet another set of disparate systems. Management is aware of these risks and a likely reason why they structured the arrangement as a JV and with non-compete agreements. - Cash Out - Sell off JV Stake

Allscripts could go the route of the private equity investor and cash out entirely. However, this also assumes they can grow the business, pay down debt to increase the equity value and find a buyer. The problem with this option is that it would immediately result in a decline in revenue and earnings given they would be disposing of a consolidated entity. While Allscripts would have some cash in its pocket, management would be left with the growth problem they had before and without a Homecare business that generated approximately $15-20 million in revenue. - Status Quo - Find a Partner

This is the more probable outcome given a lack of alternatives. Either GI commits to the arrangement for a longer period of time or GI finds a buyer for their stake when they are ready to exit. Allscripts would be in the same financial and strategic position, assuming no change in terms.

WAB

To view our analyst's original report on Wabtec click here. Hedgeye Industrials analyst Jay Van Sciver presented his updated Wabtec (WAB) Black Book this week in which he reiterated his short call on the company. Below is a chart and key excerpt:

Shares of WAB have rebounded from their February lows, providing what we expect to be an attractive exit/short opportunity. Wabtec management has not lowered 2016 guidance, despite what we expect will prove a very challenging operating environment (see chart below). Instead, WAB has initiated the largest buyback in the company’s public history just past what we see as an obvious cyclical peak.

HBI

We added Hanesbrands (HBI) to the short side of Investing Ideas this past week. Click here to read our Retail analyst Brian McGough's full stock report.

NUS

To view our analyst's original report on Nu Skin click here.

Hedgeye Consumer Staples analyst Howard Penney has no update on Nu Skin (NUS) this week but reiterates his short call. Below are a few key takeaways from Penney's original stock report on NUS:

- "Multi-Level Marketing (MLM) companies should not be public companies. NUS can only grow its revenues by recruiting new distributors into the system... At market saturation, all this is really illusory: there’s not enough addressable market left, and not enough margin so that a new distributor can actually make a profit."

- "Until recently, VitaMeal has been the secret weapon of NUS: the ultimate pyramid scheme within a pyramid scheme, and presented as a charity. The unwinding of this product could have significant implications for NUS financially."

- "NUS is under investigation by the SEC. Given how significant VitaMeal is to the earnings of the company and the significant conflicts of interest that it appears to present, we think it’s just a matter of time before the SEC expands its investigation into the company’s business practices."

ZBH

To view our analyst's original report on Zimmer Biomet click here. Below is a brief update on Zimmer Biomet (ZBH) via Healthcare analyst Tom Tobin and the key takeaways following our Healthcare Policy conference for institutional investors this week.

We had a great Healthcare Policy conference this week in NYC that was attended by institutional investors. The speakers covered a number of topics ranging from the upcoming presidential election, to long term Medicare solvency, and Millennial attitudes toward risk, to name a few. Our notes from our speaker who covered the new reimbursement policy for Total Knee Replacement are below but the key takeaway is that the trend is negative for ZBH and the other orthopedic device manufacturers, even though management’s public comments suggest it isn’t.

On another note, Blue Cross Blue Shield released a study of the newly insured under the ACA showing a massive increase in inpatient admissions, doctor visits, and specialty services demand. We know from other work, that this had a positive impact on ZBH.

However, at our conference, an expert on managed care suggested that the only reason the Public Exchanges have enrollees at all is because the insurance companies are subsidizing the losses on these members. His view was that insurance companies were nearing the end of supporting ACA members and, without significant changes in policy, were likely to exit the business. This, of course, would leave millions of people uninsured again, which is a horrible outcome, but one that will get some attention from both Democrats and Republicans before it happens.

Conference Takeaways on Orthopedics

- CCJR Implementation is likely to delay procedures on high co-morbidity patients with high re-admission risk (10-20% of patients). That's a headwind to volume until it resets. Currently, using Perioperative Orthopedic Surgical Home (POSH) Scores, or “modifiable risk factors” which are used to restrict access until a patient is “controlled.”

- 50% of cost savings is going to come from post-acute and rehab – NYU 63% SNF/Rehab in 2012 -> 22% in 2014 and reduced average LOS by 50%. Cost savings on implant is “absolutely” coming as post-acute savings are captured.

- Procedure volume will consolidate among “winners” while “losers” exit total joint as CMS reimbursement moves from primarily based on reported individual hospital costs to 100% regional procedure cost trends.

- Generic Implants are coming sooner than some think. There is no clinical difference and they are high quality. Total knee implants should cost $1,500. There are prospective offerings in the pipeline (DJO, JNJ, MDT) but reluctant to make NYU the first adopter, as it has to be a US manufacturer. High single digit declines in implant price seem reasonable.

CME

We added CME Group (CME) to the long side of Investing Ideas this past week. Click here to read our Financials analyst Jonathan Casteleyn's full stock report.

TIF

To view our analyst's original report on Tiffany click here.

Tiffany's (TIF) ecommerce traffic trends have not looked good to date in the first quarter. Y/Y Traffic Rank (which measures unique visitation and page visits/user) continues to deteriorate, now even worse than seen in 4Q when TIF reported an ugly -9% comp. E-commerce only accounts for 6% of sales at TIF, but it’s a good barometer for brand relevance. Management guidance assumes some gradual improvement throughout the year but management's outlook has been overly optimistic over the past 6 quarters. If e-commerce traffic trends are any indication, the business may be weakening yet again.

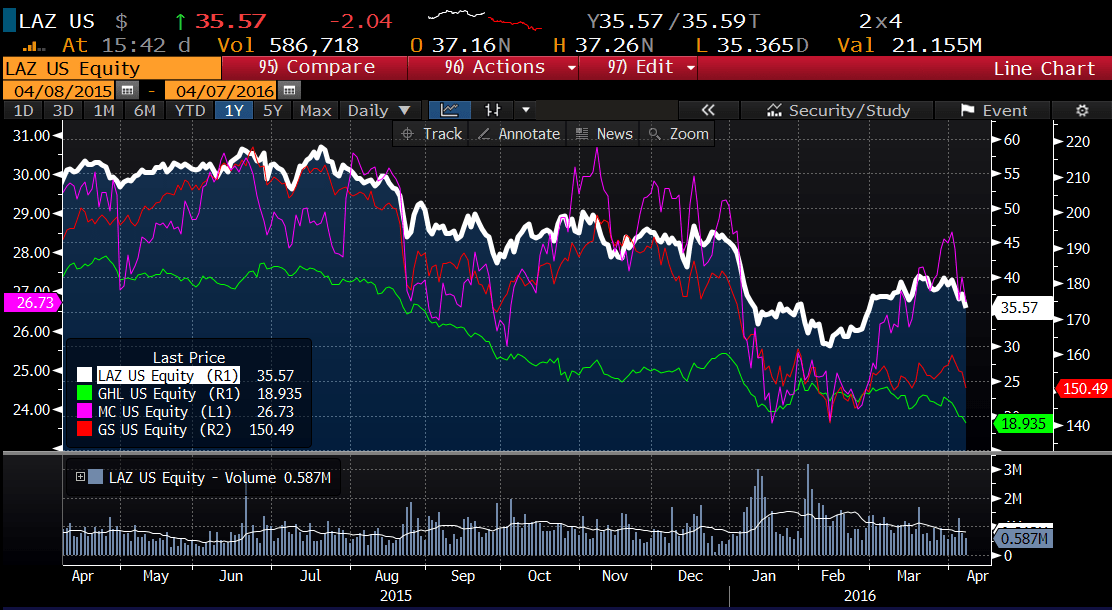

LAZ

To view our analyst's original report on Lazard click here.

The merger and acquisition (M&A) advisors had a tough week with two unexpected negative catalysts running through markets. In a surprise move, the U.S. Treasury released a new iteration of tax inversion parameters on Monday aimed at being even more stringent than the most recent cut from 4Q 2015. Basically, what had been an advantageous strategy for a U.S. company to acquire a foreign competitor and then relocate to the lower foreign tax jurisdiction took a major hit as the U.S. Treasury issued new rules that all but disallowed the practice.

Within 24 hours, the $160 billion Pfizer/Allergan deal, which would have reincorporated to Allergan’s lower tax regime in Ireland, was called off by both entities. The other unexpected event was the pending oil field services deal between Halliburton and Baker Hughes being flagged by the Department of Justice as anti-competitive.

While Baker/Halliburton have publicly responded in contest to the DOJ lawsuit, both of these developments have serious trickle down impacts for the merger advisors involved. The Pfizer deal, at a potential $100 million advisory ticket, will be a substantial lost opportunity for Goldman Sachs, Morgan Stanley, and JP Morgan, however sentiment and forward fees for the entire M&A advisory group will only shrink as the inversion practice is de-emphasized.

Our short idea, Lazard (LAZ), has substantial exposure with 50% of M&A revenues in the U.S. and 35% in Europe, meaning they have been a prime beneficiary of inversion clients shifting between domestic and foreign geographies. Shares of leading M&A advisors have been in a decided downtrend over the past 12 months as the market comps lower. We think this will continue with higher corporate credit costs and the new rule sets promulgated this week.

MCD

To view our analyst's original report on McDonald's click here.

Hedgeye Restaurants analyst Howard Penney has no update on McDonald's (MCD) this week but the stock hit another all-time high. As we continue to reiterate, the company has all the style-factors that we like – high market cap, low beta and liquidity. Stick with it.

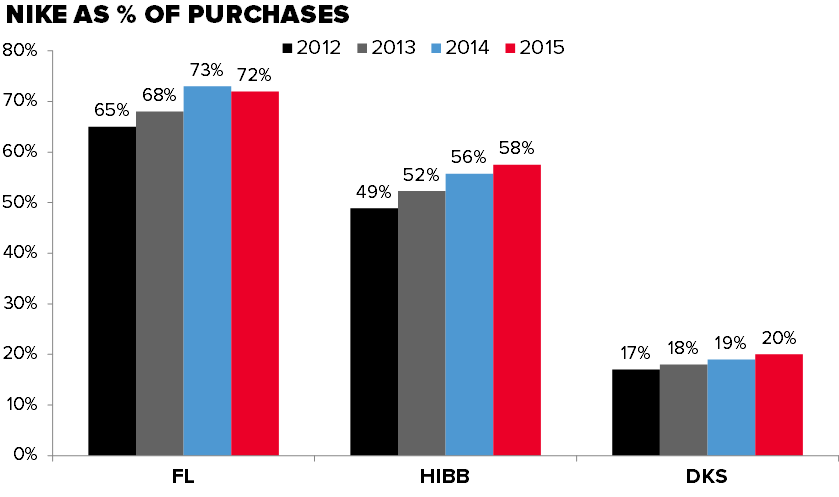

FL

To view our analyst's original report on Foot Locker click here.

Three of the four biggest public Nike distributors have released 10k's to date, and the Nike growth trends (measured by Nike as a % of purchases) have shown signs of a top. The headline, of course, is the deceleration of Nike sales within Foot Locker (FL) from 73% to 72% in 2015. But, just as important is the measured Nike growth within HIBB, up 180bps Y/Y vs. 340bps in both 2014 and 2013 and DKS up just 100bps despite a renewed emphasis on footwear and additional floor space allocated to apparel from underperforming categories like hunt and golf.

Nothing that any of these retail partners sells drives more traffic and boosts ASP more than something with a Swoosh on it. Unfortunately for Nike’s partners, incremental Swoosh growth is coming from Nike direct, putting an end to the nine year tailwind experienced by the industry.

GIS

IS ZBB A FAD?

Zero-based budgeting supporters and adversaries are starting to make their philosophies on that matter more pronounced. ZBB is purely focused on improving near term profits, while likely sacrificing key functions of a corporation. A couple questions were raised on General Mills' (GIS) 3Q16 earnings call regarding ZBB, one being, with ZBB do you sacrifice food quality or safety?

This is a very important question to raise, and those companies that go too far could be putting their quality in jeopardy. Consumer trust and loyalty are vital to the success of a brand and if that is broken you know what can happen (see Chipotle as an example). The big question is, will these expanded margins ZBB companies are achieving be sustainable, or, in a couple years, will we see them reversing course, reinvesting in their brands to catch up with those that invested intelligently from the beginning? We are in the camp that the 3G way is untested in the consumer packaged food sector, and is an unsustainable model for the long term prosperity of a company.

GIS has been on an amazing run, up 12.0% since going on Investing Ideas on May 26, 2015, versus the S&P 500 which is down -3.7% over that same period. We continue to like the name in the long-term, given their strong brands and management team.