“A leveraged business is much more difficult to run than a long-only business.”

-Myron Scholes

Myron Scholes is a Canadian who hails from up in my neck of the woods (a small town in Northern Ontario called Timmins). He’s famous in Economics circles for his Black-Scholes model (Nobel Prize in 1997) and infamous for his role at Long-term Capital Management.

The aforementioned quote came from his interview in Efficiently Inefficient where Lasse Heje Pederson asked him about the main takeaways from his experiences at Salomon Brothers and LTCM.

“It is necessary to plan for shocks and losses across positions that are held at times of shock… it’s tough because you are dealing with three things simultaneously: the assets you acquire; the business that you’re in; and how you actually finance activities.” (pg 268)

Back to the Global Macro Grind…

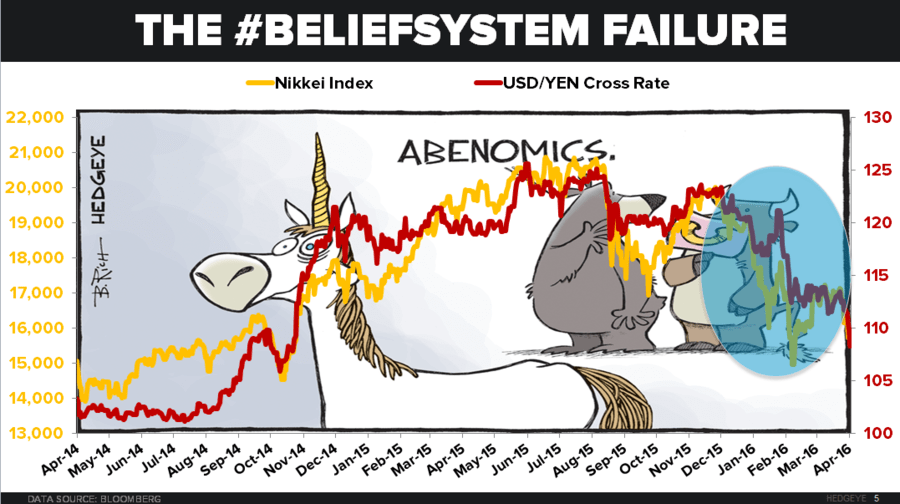

Is the business of risk managing macro markets in what was the Golden Age of Central-Market-Planning tough? Very. Especially at this stage of the game when all of the “rules” of the #BeliefSystem start to break down, the Levered Business of carry trading gets scary.

We’ll get into much more detail on how the #BeliefSystem is breaking down in both Japan and Europe on our Q2 Global Macro Themes Call at 11AM EST, but at a basic level here were some basic rules that levered macro strategies used to get paid by:

- BOJ (Bank of Japan) prints, devalues, and prints => Yen falls => Japanese Stocks rise

- ECB (European Central Bank) says “whatever it takes” => Euro falls => European Stocks rip

Sound familiar? All Janet Yellen has to do at this stage of the game in the USA is Devalue The Dollar and stocks, commodities, and junk bonds, that are inversely correlated to that go straight up (to lower-highs).

But what if you’re short Yens and/or Euros and long Nikkei and Italy’s MIB Index, with leverage?

A: You’re out of business

Yen Bulls (there aren’t many) are lovin’ Yellen right now. While the Japanese Yen (vs. USD) is signaling immediate-term TRADE overbought at $108 (within a bullish intermediate-term TREND), what is it going to take for the BOJ at their meeting on April 28th to change TREND?

A: I don’t know (they don’t either)

In Europe this morning, overlord Draghi issued the ECB’s Annual Report and said (I couldn’t make this up if I tried), “we will not surrender.” And you know what the Euro (vs. USD) did on that?

A: It went down 10 basis points

Now if you have friends that are in the business of only being long US Equities, this is a good thing (for now). But what happens when more and more and moaarrr dovishness is needed to keep the US Dollar from going up?

A: Eventually the USA ends up in the same place as Japan and Europe

Never, Keith. ‘We are the best house in a bad neighborhood… Auto sales were strong… but now gas prices are stronger’ … or something like that will be the perma bs case. Reality is that eventually it gets to your country’s banks.

How does that happen?

- Central-market-planners have to keep devaluing their currencies…

- But they have to cut long-term interest rates to all-time lows, in doing so…

- Eventually, instead of ZIRP, they get NIRP (negative interest rate policy)…

And a lot of businesses (lots of banks) don’t make money in that scenario.

In other words, to keep the game going this way, Janet Yellen’s Fed will have to eventually reduce the probability of ANY rate hike to 0%, long-term Yields will break to all-time lows, and Jamie Dimon will have to try to create his own CNBC “double-bottom”, buying back stock as JPM fundamentals look the way every other bank in Japan and Europe does under a negative yield regime.

This is why I pivoted from bearish on Energy (XLE) to most bearish on Financials (XLF) when we did our Q1 Macro Themes Call. It’s also why I signaled “buy more” Utilities (XLU) on yesterday’s pullback.

Our Best Ideas are levered to the Fed coming around to our #LateCycle US economic view. If you ran a fund that was only long Utes and short Fins in 2016, you’d want leverage on that P&L too!

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.69-1.81%

SPX 2025-2077

RUT 1069-1130

Nikkei 152

USD 94.01-96.04

EUR/USD 1.11-1.14

YEN 108.33-111.99

Oil (WTI) 35.04-40.25

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer