Hedgeye and the Potomac Research Group are proud to present our first annual Spring Health Policy Conference. This special, invite-only event will be held at The Benjamin Hotel in New York City on Monday, April 4th, 2016 from 9:30am - 4:00pm.

~ CLICK HERE FOR THE FULL INVITE ~

RSVP TODAY to to attend. Please note that space is limited.

Our lineup of health policy experts will offer an insider's view on their policy outlook and how as practitioners policy is influencing their decision making process.

This exclusive event will be moderated by Hedgeye Healthcare sector head Tom Tobin and feature in-depth presentations and panel discussions. There will be ample opportunity for interaction throughout the day.

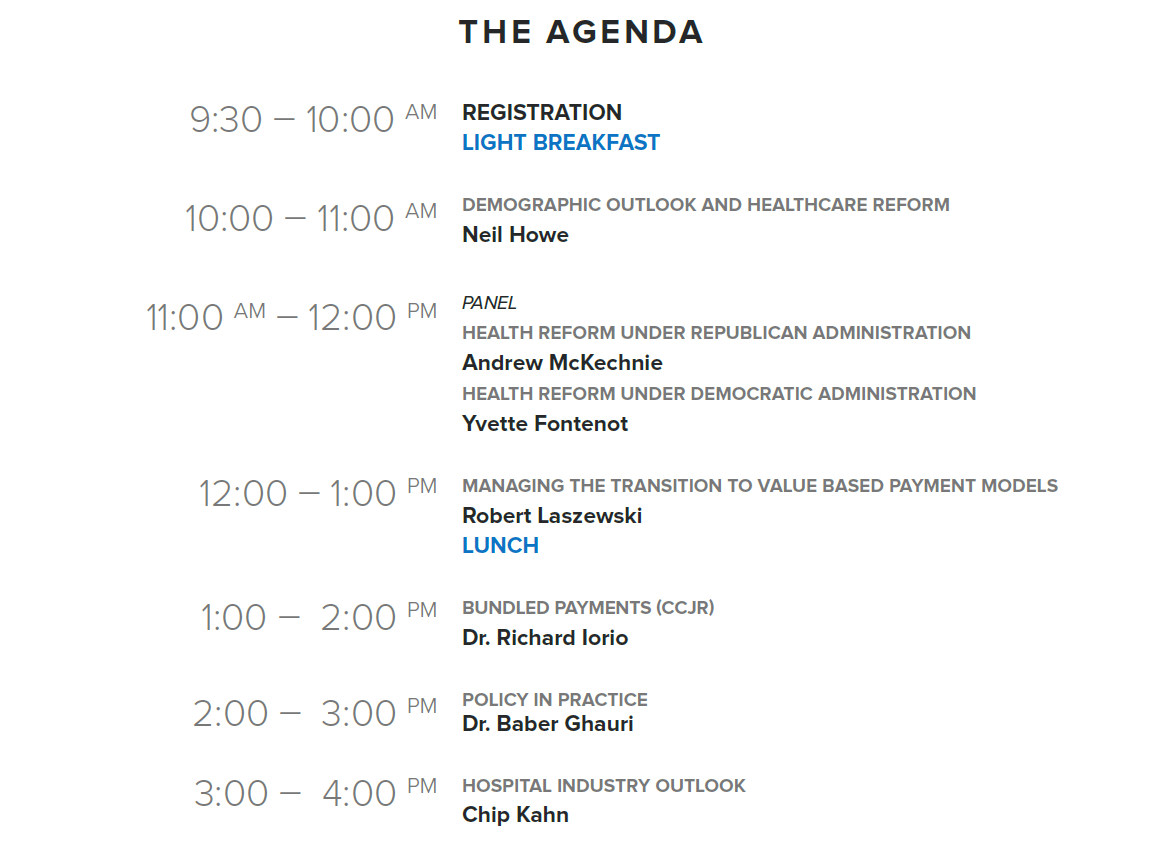

SPEAKERS AND TOPICS

CHIP KAHN - Hospital Industry Outlook

Chip Kahn, President and CEO of the Federation of American Hospitals, will shape the regulatory environment for hospitals heading into the Presidential election. Mr. Kahn’s extensive health policy expertise and lengthy Capitol Hill experience make him one of Washington, D.C.’s most effect and accomplished trade association executives.

NEIL HOWE - Demographic Outlook & Healthcare Reform

A historian, economist, and demographer, Neil is also a recognized authority on global aging, long-term fiscal policy and migration. He is a senior associate to the Center for Strategic and International Studies (CSIS) in Washington, D.C., where he helps direct the CSIS Global Aging Initiative.

ANDREW MCKECHNIE - Health Reform Under Republican Administration

Andrew McKechnie, former policy advisor to the Senate Finance Committee, will discuss Republican efforts to repeal the Affordable Care Act and what the law may look like under a Republican controlled White House. Mr. McKechnie was a key negotiator in bipartisan efforts to pass health reform in 2009, with an area of expertise in Republican politics and strategy.

YVETTE FONTENOT - Health Reform Under Democratic Administration

Yvette Fontenot is a partner at Avenue Solutions, a democratic government affairs firm that offers strategicadvice, policy development, and counsel in federal legislative and executive areas. She previously held theposition of Deputy Director of the Office of Health reform at the Department of Health and Human Services(HHS) and has helped to draft and implement the Affordable Care Act (ACA).

ROBERT LASZEWSKI - Managing Transition to Value Based Payment Models

Robert Laszewski, president of Health Policy and Strategy Associates (HPSA), will address the issues facing key stakeholders (Hospitals, MCOs, Physicians and Pharma) as we the transition to value based payment models focused on delivering better quality at a lower cost. HPSA is a policy and marketplace consulting firm specializing in assisting its clients through the significant health policy and market change afoot.

DR. BABER GHAURI - Policy in Practice

Dr. Ghauri, Interim East Division CMIO for Trinity Health, will discuss how policy influences the decision making process of the second largest nonprofit health system in the nation. Dr. Ghauri’s has a deep background in medical informatics and will also discuss how Trinity is using technology to pursue quality and value initiatives.

DR. RICHARD IORIO - Bundled Payments (CCJR)

Richard Iorio, MD, is the William and Susan Jaffe Professor of Orthopaedic Surgery at New York University Langone Medical Center Hospital for Joint Diseases and Chief of Adult Reconstruction at NYU Langone HJD. Dr. Iorio was involved in the Medicare pilot program that led to expansion of the of bundled payment initiative for total knee replacements.