Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more.

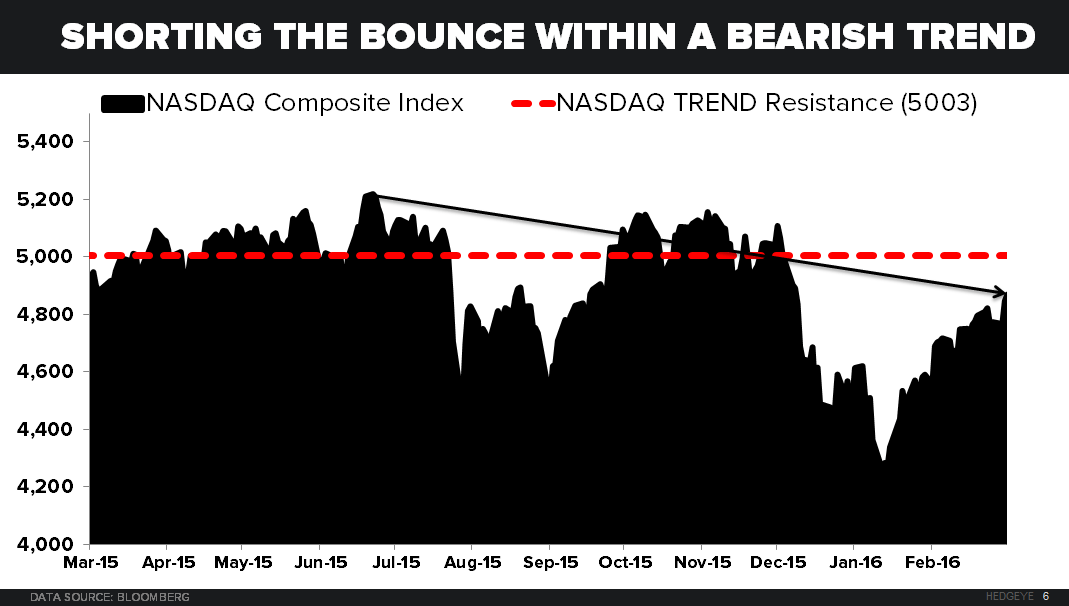

"... I shorted it in Real-Time Alerts yesterday and here’s why:

- We have the most bearish forecast on Wall Street for US Growth for Q2

- I want to be short High-Beta, High-Multiple, Over-Owned Growth in Q2

- My immediate-term TRADE signal said short some within its developing bearish @Hedgeye TREND"