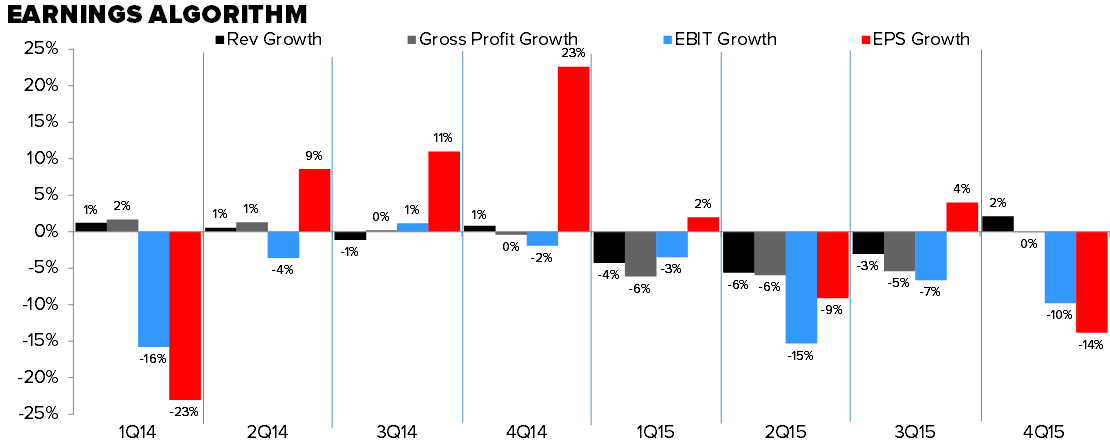

We’re adding PVH to our short bench – not because this quarter was horrible at face value (EPS -14% yet Manny ‘beat expectations’), or because it’s up 36% since January. But because we think the poor quality of earnings is validation that this business is seriously growth-constrained going forward. It arguably has only one highly defendable piece of the business, and that’s CK fragrances, and even that’s been losing share in recent years. How we’re doing the math, fragrances’ $1.4bn in retail revenue accounts for about 18% of EBIT. That leaves over 80% of earnings and cash flow that we have a tough time arguing will grow or improve margins without a meaningful capital investment. Could PVH simply do another deal? Yes, it’s possible. But to see a company with a $10bn EV and $3bn in debt do a sizable transaction so late in the economic cycle would be downright frightening. It would also validate that it’s got no game in its core business. The key thing for us today is to drill down whether it is a short right now, or in another six months based on a) the puts and takes of the near-term model and b) how management ‘works the street’ (or at least tries to – it’s getting old) as it relates to expectations. Regardless, there’s nothing we could hear on the call that is likely to change our long term view on this business, or the limited prospects for its brands.

Much more to come on this one.