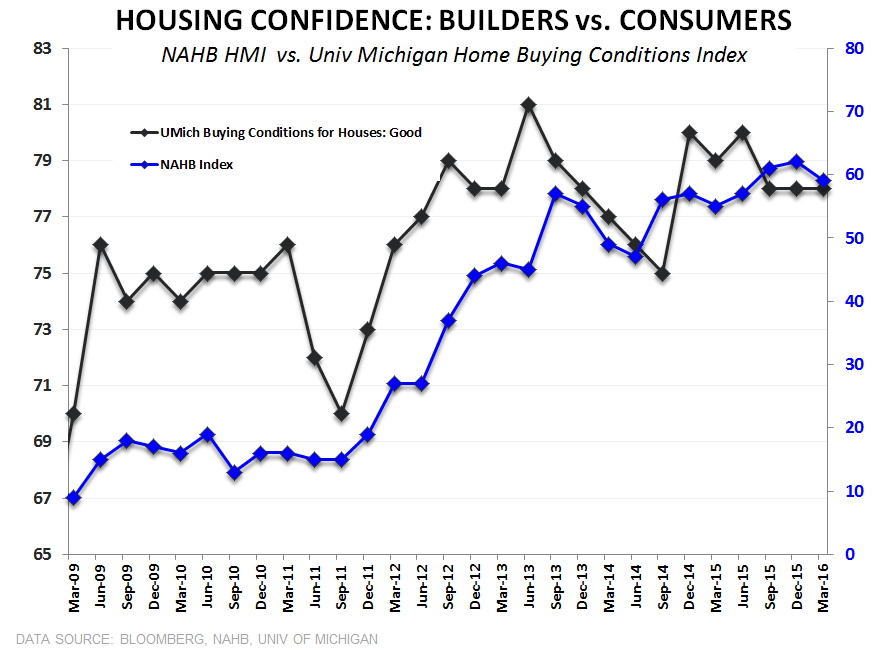

Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

Today's Focus: March NAHB HMI (Builder Confidence Survey)

Builder Confidence in March was static at 58 against unrevised February estimates, holding at 9-month lows and marking a 5-month past the cycle peak of 65 recorded in October.

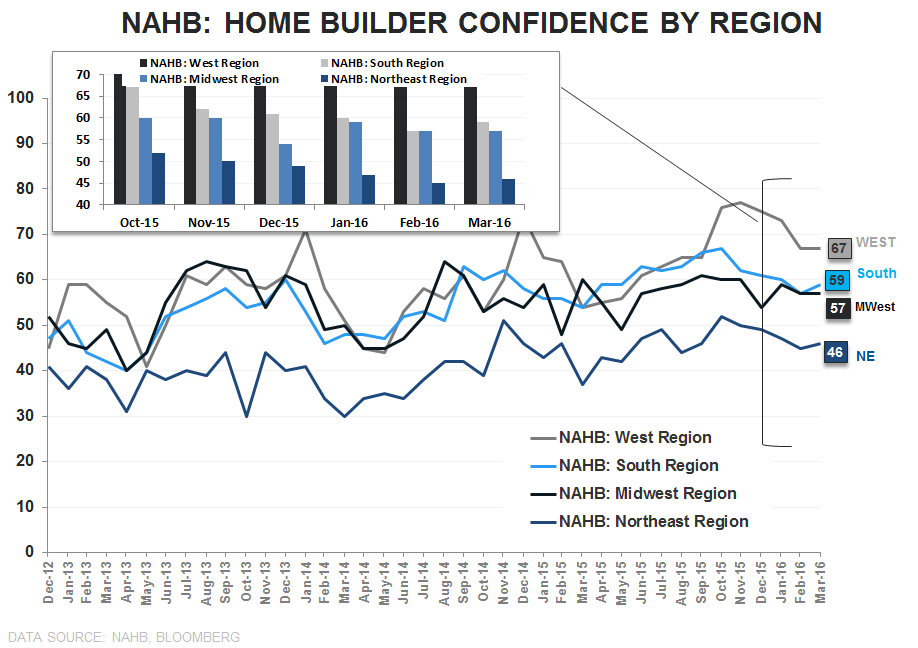

Across the Survey Indicators, Current Sales held flat at 65 while the -3pt decline in Forward Expectations was offset by a +4pt gain in Current Traffic. Geographically, the West and Midwest regions were flat sequentially with +1pt and +2pt gains in the Northeast and South, respectively.

Top-down, falling mortgage rates and an ebb in market volatility helped offset the prevailing reality that demand is slowing, supply remains constrained and labor and lot supply issues remain unlikely to resolve in the near-term.

Commentary was largely generic with a nod to continued consternation around lots and labor and the broadly positive fundamental backdrop:

NAHB Chairman Ed Brady: “Confidence levels are hovering above the 50-point mid-range, indicating that the single-family market continues to make slow but steady progress. However, builders continue to report problems regarding a shortage of lots and labor.”

And from NAHB Chief Economist David Crowe: “While builder sentiment has been relatively flat for the last few months, the March HMI reading correlates with NAHB’s forecast of a steady firming of the single-family sector in 2016. Solid job growth, low mortgage rates and improving mortgage availability will help keep the housing market on a gradual upward trajectory in the coming months.”

In short, nothing particularly remarkable in the March release as Builder Confidence remains past peak and the larger demand trend across both the new and existing markets remains one of deceleration.

Looking to February Housing Starts data tomorrow, we expect the number to be strong from a rate-of-change perspective as we lap the depressed, severe weather comps from last February – for reference, even if we were flat with the disappointing January numbers, Starts would be up >+22% year-over-year given the base effect. Similar comp dynamics exist for March as well. We’ll get EHS for February on Monday and expect sales to be down sequentially and slowing on a year-over-year basis as the trend in closed activity recouples lower to the trend in Pending Home Sales.

About the NAHB HMI:

The Housing Market Index (HMI) is based on a monthly survey of NAHB members designed to take the pulse of the single-family housing market. The monthly survey has been conducted for 30 years. The survey asks respondents to rate market conditions for the sale of new homes at the present time and in the next 6 months as well as the traffic of prospective buyers of new homes. The HMI is a weighted average of separate diffusion indices for these three key single-family series. The HMI can range from 0 to 100, where a value over 50 implies conditions are, on average, improving, a value below 50 implies conditions are worsening, and an index value of 50 indicates that the housing market is neither improving nor worsening.

Joshua Steiner, CFA

Christian B. Drake