“We are just an advanced breed of monkeys on a minor planet of a very average star. But we can understand the Universe. That makes us something very special.”

-Stephen Hawking

In a crazy stock market year like this, it feels somewhat appropriate that it is the Chinese Year of the Monkey. After all, how better to characterize the volatility of global stock markets than comparing them to one of the most frivolous, yet human like animals in the wild kingdom?

Here at Hedgeye, we’ve also used the word "monkey" to refer to the use (by some stock market operators) of 200 and 50-day moving averages to determine buy or sell points on stocks and markets. This positioning occurs despite any supporting evidence that breaking above or below a moving monkey average is actually predictive of a future move.

According to the Chinese Fortune Calendar:

“Therefore, we will deal with more financial events in the year of the Monkey. Monkey is a smart, naughty, wily and vigilant animal. If you want to have good return for your money investment, then you need to outsmart the Monkey”

That sounds like an appropriate 2016 analogy to us.

Back to the Global Macro Grind…

As stock market operators, one of the biggest risks you’ve faced over the last 9 months or so has been the risk of consensus. According to a Bloomberg report this morning:

- Stocks with the most hedge fund ownership in the Russell 3000 have declined -31% since July 2015 compared to the SP500, which is down -2.8%;

- An index tracking the companies with the most concentrated ownership have declined -45% since July 2015; and

- Finally, hedge funds have been net sellers of $3.5 billion in equites this year. More than any other asset managers.

Talk about negative Alpha!

In all seriousness, there is a reason why we attempt to quantify buy side consensus in our best ideas. It's because if you are on the wrong side of a concentrated hedge fund bet that is unwinding, the stock is mostly definitely not going to see support at a "moving monkey" average.

On the macro front, our colleague Darius Dale has been closely investigating the consensus view of emerging markets. He's hosting a conference call tomorrow titled, “Is this a Generational Buying Opportunity in Emerging Markets?” No surprise, China will be a major focus of his call.

According to Darius, the key questions to focus on are whether the Chinese economy, its banking system and the yuan are as vulnerable to collapse as consensus believes? Many investors seem to be of the view that China requires a material devaluation of the RMB to stave off banking crisis and/or outright economic collapse. Some investors actually believe each of those outcomes is inevitable. If you’d like to join the call, please email .

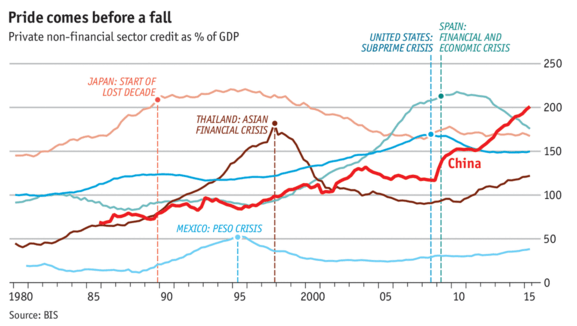

Last week, The Economist published a chart, which we’ve republished in our Chart of the Day below highlighting private lending within the Chinese economy, and compares it to other economies before their deleveraging and crash. Based on this chart and measure, a Chinese crash seems inevitable. But like most things that appear in the mainstream media, the better question to ask might be whether this is already baked into consensus?

Over on the oil front, the recent price move seems to imply that the worst is behind oil. With drilling activity at an all-time low in the U.S., there is some credence to that story, but like most simple models, U.S. drilling is, but, one factor in the global supply and demand story. A few things to note this morning:

- Iranian production climbed last month by the most in almost two decades following the end of sanctions. Iran increased output by 187,800 bpd to 3.13M in February, the biggest monthly gain since 1997; and

- OPEC is revising downwards demand for its oil produced by its members as production outside OPEC remains ever resilient; and

- The spread between Treasuries and high yield debt of energy companies has narrowed by about a 1/3 in the last month. The implication is that the market for energy financing is opening ever so slightly based on the recent crude rally.

Needless to say, we’ll stick to our bearish view of crude oil. Supply and demand fundamentals aside, it is going to be very difficult for oil to rally in the face of a U.S. central banking that is on the margin more hawkish than its global peers. A strong dollar is not good for the global commodities that are priced in it, like, say, oil.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.76-2.00%

SPX 1

VIX 16.01-21.15

USD 95.83-97.66

Gold 1

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research

Credit: The Economist