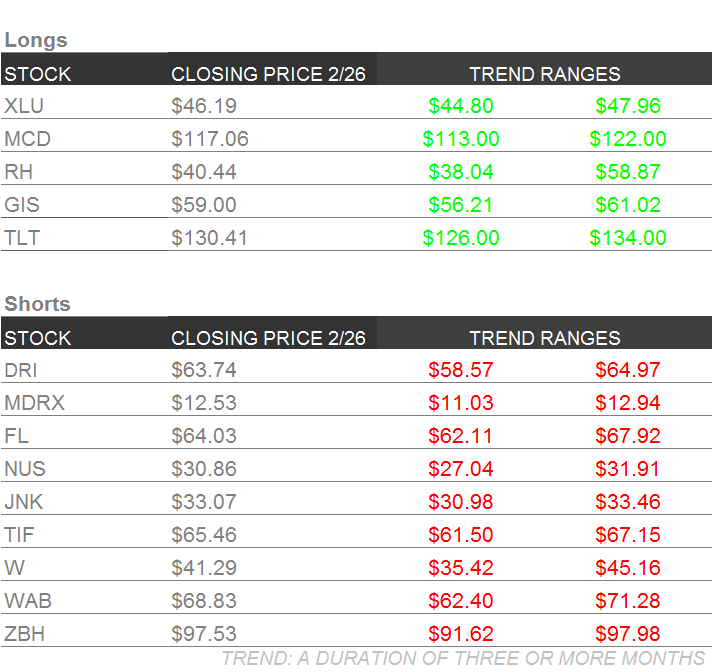

Below are our analysts’ new updates on our fourteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this. Hedgeye CEO Keith McCullough’s updated levels for each ticker are below.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

TLT | XLU | JNK

To view our analyst's original report on Junk Bonds click here and here for Utilities.

To quote Hedgeye Macro Analyst Christian Drake from Thursday’s Early Look:

“The yield curve flattens as the economy slows with policy and/or liquidity management driving the short-end higher and defensive positioning and/or discounting of lower future growth/inflation driving the long end lower. Lower lows in the yield spread ≠ the bond market pricing in ‘escape velocity’.”

A flattening in the yield spread (10yr Treasury yield – 2yr Treasury yield) continued this week into double digit basis point territory (currently at 96bps). YTD the yield spread has declined 44 bps while the 10yr Treasury yield has dropped 47bps.

On the other side of our Long-Term Treasuries (TLT) call, what should be concerning to junk bond bulls is that Junk Bond ETF (JNK) is down -2.6% YTD DESPITE the huge move in Treasuries. Bonds typically move higher when interest rates decline (present value effect of discounted cash flows – a cash flow in 3 years is worth more in today’s terms if the risk free alternative offers a lower return), unless of course poor growth and a dour outlook for the economy brings up the question of creditworthiness. That’s where we are now, and we expect our credit spread call to continue to play out.

As for growth, the Markit Service Sector PMI reading for February fell into contraction for the 1st time since the recession this week. Here's the why that is highly relevant:

- Services Consumption represents ~65% of household spending

- Services sector makes up ~45% of GDP

- The ISM Services Index has shown a similar trend – slowing in each of the last 3 months and, at the current index reading of 53.5, sits at its lowest level since the “polar vortex” lows of February 2014

Hitting on Friday’s revised GDP report (Q/Q SAAR Q4 GDP revised to +1.0% from +0.7%), a deep-dive into the number doesn’t support an incrementally stronger economy:

- Consumption was revised down marginally but net exports were up with the negative revision to imports outweighing the negative revision to exports. That’s good for the number but lower global trade activity is not a good sign for global growth;

- Much of the actual change in the revision was due to inventories, which contributed +0.31pts to the headline number

Find your preferred growth slowing vehicle wherever you can. Our's remains TLT in fixed income and Utilities (XLU) in equites.

MDRX

To view our analyst's original report on Allscripts click here.

We spoke with Northwell Health (Allscripts #1 Customer) and got some great detail around where Allscripts fits into their future plans. The discussion also further confirmation of our short thesis. Two big takeaways from our conversation were:

- The main reason why they are still with Allscripts is due to the high switching costs and;

- Limited cross sell potential as their IT budget is capped out and already committed to other vendors.

Here is some additional color:

- No plans to move away from Allscripts due to the enormous amount of capital invested in the system and high switching costs; happy with their products.

- IT Budget $250 million and capped out in terms of growth.

- Concerned about the future of Allscripts as there is a big slowdown in spending coming.

- Limited additional cross-sell potential. Already committed to Soarian for Enterprise Rev Cycle and InterSystems for population health; don't see efficiency in remote hosting.

- Touchworks and Sunrise NOT integrated on the back end, requires the purchase of dbMotion, which is expensive to implement.

- Added 3 hospitals over last 18 months on Sunrise through acquisitions for an incremental $3-4 mill in maintenance revenue to Allscripts.

- IT outsourcing agreement for $80 million a year, $10-20 million a year in software related subscription and maintenance revenue.

Bottom line: The MDRX risk/reward is less favorable since we first added it as a Best Idea Short in the mid-$14s, but we still see downside below $10 on slowing bookings growth.

Click here to watch a video of Healthcare analysts Tom Tobin and Andrew Freedman covering MDRX and updates on other companies they cover, including:

- MEDNAX (MD) is the acquisition model broken

- Hologic (HOLX) 3D update

- Allscripts Healthcare Solutions (MDRX) field notes

- Recession tracker

NUS

To view our analyst's original report on Nu Skin click here.

On February 22, 2016, Nu Skin (NUS) entered into a settlement term sheet in the potential settlement of a previously reported putative securities class action consolidated lawsuit. This litigation was brought against the company and certain of the company’s officers on behalf of the class consisting of persons or entities that publicly traded the company’s common stock during the period from May 4, 2011 through January 17, 2014 and were allegedly damaged thereby.

Additionally, NUS received notification that on February 25, 2016 the Tokyo District Court issued its ruling on a dispute between the company and the customers authority in Japan. As a result of the District Court’s decision, the company plans to take a non-cash charge of approximately $32 million or approximately $0.36 per share, in Q1 2016, which was not reflected in the company’s previous guidance.

WAB

To view our analyst's original report on Wabtec click here.

Wabtec's (WAB) expectations for its Freight segment, its highest margin business, is unrealistic in our view. The expectation of flat revenue in the Freight segment is also not particularly reasonable given a book-to-bill at around 0.80, peaking PTC sales, weak international markets, and sizeable expected declines in rail car & locomotive deliveries.

While it is possible that further draws on backlogged orders, large share repurchases, and incremental acquisitions might get WAB to guidance, markets are unlikely to care. In our view, the freight rail market is entering a long downcycle and WAB’s changed behavior serves as confirmation.

TIF

To view our analyst's original report on Tiffany click here.

There have been some recent news articles and reports about how millennial trends and preferences are going to hurt or help Tiffany's (TIF) sales in the coming years. Some state increased online options will take people away from Tiffany, others think later marriages means more dollars spent on Tiffany rings. We're not sure either is correct, and neither is relevant over the near term.

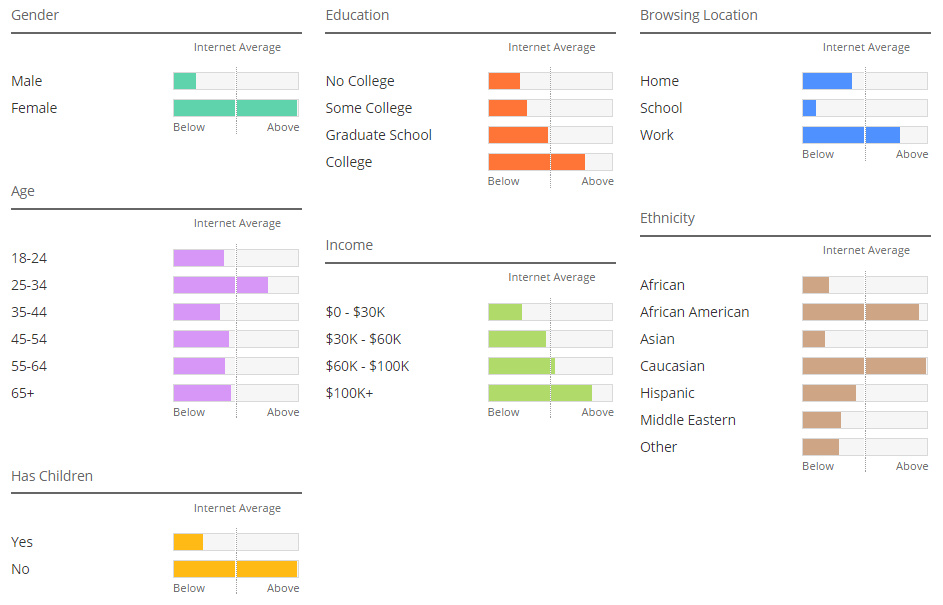

Below you can see how Tiffany's visitation demographics compare to those of the internet as a whole. The breakdown: female, well educated, mid-20s to mid-30s, and skews higher in income.

Our call on the stock in not centered around generational trends, though, if we had to weigh in on the subject we’d argue that TIF has far less cultural relevance than it did 20 years ago. The facts are -- TIF is highly exposed to the economic cycle with a working capital intensive model and operational leverage that leads to the type of earnings volatility we’ve seen in a weak consumer environment. We still think earnings expectations remain too high.

W

To view our analyst's original report on Wayfair click here.

Three key points on Wayfair's earnings:

Real Growth Slowed

At face value the revenue growth at Wayfair is astounding. However, excluding the impact of increased holiday promotions, 4Q direct revenue grew at about 91%, which is a tick down on the 2-year average growth rate.

No Profitability

The question is not can Wayfair take share and grow revenue, but rather can they do it profitably? Wayfair added $339mm in revenue year-over-year, but only $9mm in incremental EBIT. A 2.6% incremental margin, down from last quarter. Despite growing direct revenue 98%, the company still lost money.

Losing Advertising Efficiency

One main issue was the reduced efficacy of advertising dollars. Revenue dollars generated per advertising dollar grew 13%, much lower than 3Q at 24%.

Takeaway: W continues to spend and build an infrastructure for a $90bn total addressable market that does not exist. We continue to believe that this company will never run a profitable business.

Click here to watch, "Under 60 Seconds: Wayfair's Earnings Report | $W"

RH

To view our analyst's original report on Restoration Hardware click here.

In light of the recent blow to Restoration Hardware (RH) shareholders, Hedgeye Retail Sector Head Brian McGough sent a detailed update on the company ahead of this weekend's newsletter. Click here to read that research note.

ZBH

To view our analyst's original report on Zimmer Biomet click here. Below is an update from Healthcare analyst Tom Tobin.

Zimmer Biomet (ZBH) increased their dividend this week to $0.24 for the quarter. At this rate, ZBH’s dividend yield stands at just under 1%. So, as a short seller pays the dividend, it adds a wrinkle into the calculus of the remaining short call here. If we check in on our time series data, the answer of whether to stay short remains yes. The BIG RISK is a US Recession, which according to the Hedgeye Macro Team is creeping closer by the week.

Unemployment Claims, Consumer Confidence, and S&P 500 company earnings, all appear to not just be in the final stages of expansion, but also the beginning stages of contraction. For the US Knee market, this is a negative, as close to half of all knee replacement surgeries are performed on people under the age of 65.

A US Recession would exacerbate our negative view of the contraction coming for the US Medical Economy, as the benefits of the ACA wane and we enter the #ACATaper. We’ve seen good evidence that the newly-insured consumed above average levels of medical care and, in one study, 6X the number of knee replacement surgeries per capita as matched against a cohort that was continuously insured.

The #ACATaper may be slow to develop, but we are seeing the signs so far in 2016. It appears the first data series to break our way has been Medicaid per enrollee spending, which is now declining year-over-year for the first time since the start of the ACA. Note: At the same time, enrollment is flat.

JOLTS has flattened sequentially and gone negative in rate of change terms, but we expect numbers to contract sequentially, which has not yet happened, but I think we’re close.

Lastly, the PPI for Artificial Joints, which we believe is driven by the mix of knees and commercially insured patients, has flatlined as well. Since this leads ZBH’s volume/mix by 2 quarters, we’re watching the monthly trend closely for evidence of a 2H16 deceleration and decline.

Keith re-shorted ZBH in Real-Time Alerts this week. I like that call.

MCD

To view our analyst's original report on McDonald's click here.

McDonald's (MCD) McPick 2 is no longer $2, it is $5. The new menu will include the Big Mac, Quarter Pounder, Filet-O-Fish, chicken nuggets and fries. Although the total dollar value is higher than most value meals versus competitors, it is arguably a better value because of the premium items you are getting. Only time will tell whether this value menu works out for them, but they are truly in testing mode, as they work to figure out a long-term national value menu.

FL

To view our analyst's original report on Foot Locker click here.

Three key points on Foot Locker earnings:

Comparable Sales Weakening

Q4 saw a great 7.9% comp. But Feb comparable sales are trending to low-single digit growth against an easy compare all while Management is guiding to mid-single digit comp growth for the year. That wipes away the leverage in the model.

Profitability

Incremental EBIT margin is down to 36% from the mid-70s rate seen in the first half of 2015. Now FL is working against those tough compares as top-line is likely slowing.

Growth Levers Limited

FL grew out of the recession by closing underperforming stores, and selling more Nike product (~78% of sales) in those remaining. This was in the middle of the biggest multi-year surge in Volume and ASP-boosting Nike product since the early 1980s. Now that is ending.

Takeaway: As good as 4Q was, most metrics look sequentially worse to us. This is a multi-year short call, and we think it’s starting to play out.

Click here to watch, "Under 60 Seconds: Foot Locker's Earnings Report | $FL"

GIS

General Mills (GIS) hit an all-time high this week when it reached $60.18 on Thursday. Although this would not be a great entry point, it is also not a reason to get out if you have a long-term view. Nothing has changed in our fundamental story and we have no reason to lose faith in our thinking to date.

Over the course of the past few years, GIS has made strategic acquisitions within the natural & organic / wellness space (we call it the string of pearls approach). Although they are not largely meaningful to top or bottom-line right now, they are changing the way the company thinks about its broader portfolio.

We continue to believe GIS is one of the best positioned consumer packaged foods companies due to its strong brands and best-in-class people and organization.

DRI

To view our analyst's original report on Darden Restaurants click here.

No update on Darden Restaurants (DRI) this week but Managing Director Howard Penney reiterates his short call. Remember the broader thesis:

- "Having pulled all the levers to create shareholder value, it’s now down to the facts about how Darden's core business is performing. There are cracks in the Olive Garden story (which makes up 56% of sales) and the brand is not as healthy as consensus believes."

- "To date, Olive Garden has done 32 remodels (out of 400), and is far behind schedule on a massive remodel project. Clearly, no one wants to remodel the Olive Garden concept because it would be disastrous for earnings."

- "What we know now is that Olive Garden is not fixed and management does not currently have a plan to rectify the situation."