A quick question for perma-bulls. After 600-plus rate cuts globally, what do we truly have to show for it? Sluggish growth, deflating asset prices, and a central planning edifice on the brink of collapse?

That sounds about right.

Here's another question. What happens when it all implodes?

We're getting a glimpse of that now in Japan. In late January, the BOJ announced it would pursue negative interest rates. Macro markets didn't like that. In direct opposition to the BOJ's intent, the Yen has strengthened 5.2% and the Nikkei has fallen -5.3%.

Whoops!

The response from central planners is getting a little desperate. Last week, then came BOJ members calling for “greater cooperation among G7 partners in order to ‘soothe’ market jitters.” That's unlikely. The ECB added that it “is ready to do its part” while Fed officials have been making the media circuit rounds parlaying the idea that "all is well."

Nope.

What does this all mean? Hedgeye CEO Keith McCullough has been grappling with this same question, about what happens when the last ounce of central-planning credibility is finally exhausted. In the Early Look this week, McCullough wrote:

"We have a social “science” experiment (or ideology) called central-market-planning (or QE)… which could easily implode if the #BeliefSystem that humans can bend and smooth economic gravity crashes."

Here's what the Fed's crashing credibility looks like via analysis from our Macro team sent to subscribers this morning:

"Gold loves nothing more than down dollar and interest rates. With consensus positioned for a stronger USD and a series of rate hikes into 2016, gold has sniffed out growth slowing data and market turmoil. In consequence, Gold and Silver are leading CRB divergences YTD at +16.6% and +10.3% YTD against a weaker USD (-1.3% YTD).

The 10-Year Treasury yield continues to price in slower growth, backing off -51bps on the year, at 1.74% this morning. While the Fed continues to play hardball on the direction of policy in 2016, the market trades skeptical."

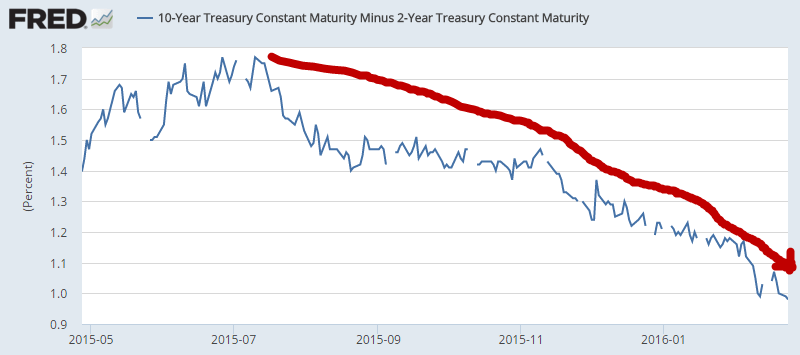

Take a look at the significant compression of the 10yr-2yr Treasury yield spread (i.e. #GrowthSlowing):

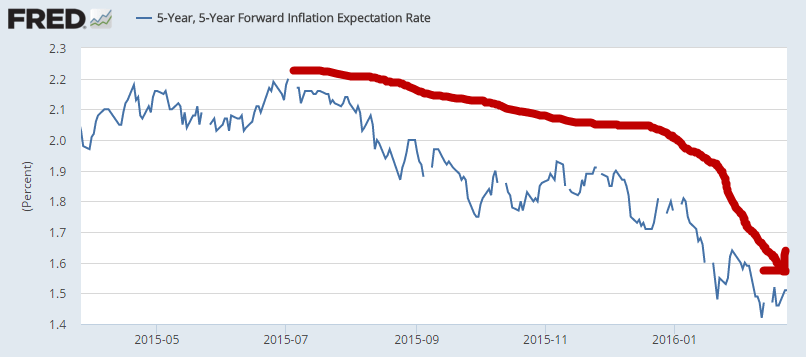

... Or (crashing) market-based measures of future inflation expectations (i.e. macro markets don't believe Fed rhetoric that #Deflation is "transitory"):

No matter. We're sticking with our process and we'll continue to front run the Fed's and Wall Street's delusional forecasts.

While we're on the subject, here's an excerpt of Keith on The Macro Show...