Takeaway: While Cat Financial’s year-end credit metrics were better than our expectations, we still expect an impact from lower equipment values and increasingly stressed customers. The Cat Channel appears to be holding units off the market with unrealistic pricing. Borrower flexibilities with respect to negative equity and skip payment options may be forestalling the eventual impact of weaker end-markets. Of course, we may also be misreading Cat Financial’s exposures and are continuing a dialogue with management. While we will not dismiss the disconfirming evidence of favorable portfolio metrics lightly, we still expect an eventual negative impact from pending mine closures, oil & gas bankruptcies, and equipment auctions.

Overview

As we went through CAT’s 10-K, we were struck by steady to improving credit trends at Cat Financial. Relevant used equipment values have generally been falling, and credit quality in many key customer categories has been deteriorating (e.g. mining, coal, oil & gas, emerging markets). We view CAT’s reporting as having become more aggressive as the company now risks falling below the key $3.50 EPS compensation threshold. Switching pension accounting methods and changing receivable loss allowance calculations can add to reported profits. The credit trends at Cat Financial could be part of the same ‘efforts’. They also may be a byproduct of a captive finance subsidiary’s role in stabilizing used equipment pricing, which can often prove costly. Perhaps Cat Financial can navigate the current environment adequately. We review some details below.

Used Equipment Pricing Is Pretty Clearly Down

While it is challenging to determine exact pricing trends in used equipment (i.e. collateral for equipment financings) the changes we track have mostly been negative. We see more equipment for sale and generally lower prices.

Perhaps unsurprisingly, oil and gas equipment is piling up.

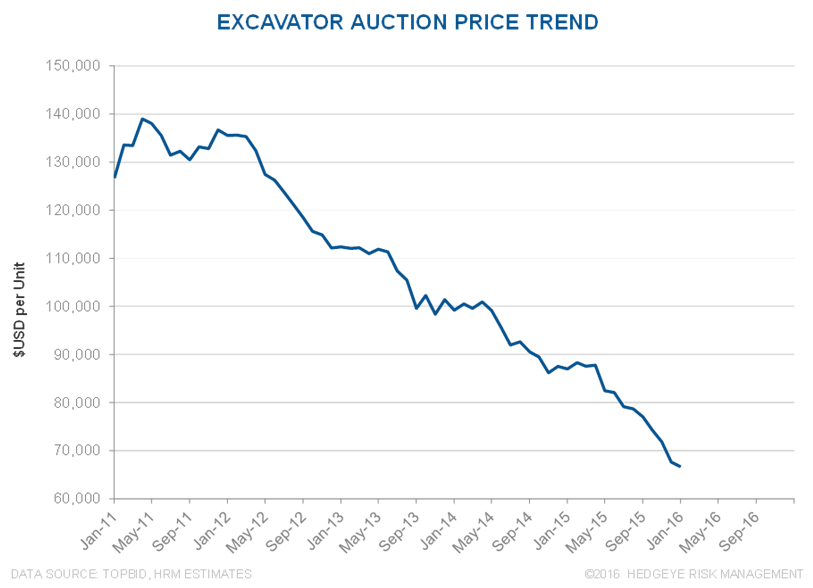

Construction Equipment, Too: Used equipment pricing pressure isn’t limited to mining and oil & gas equipment. While we think this chart overstates used excavator price weakness, it seems pretty clear that excavator auction prices have declined in recent years.

Cat Financial Credit Metrics Moving The Other Way

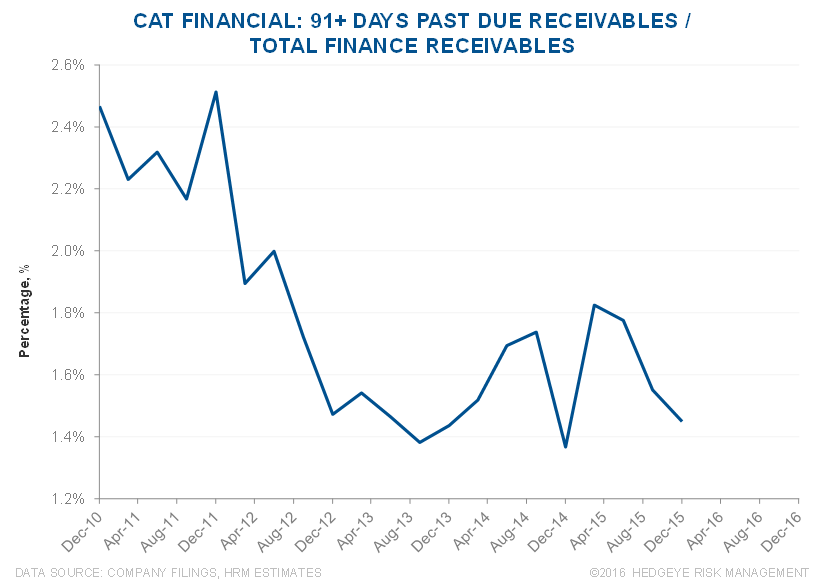

Usually, we would expect used equipment values to correlate with customer creditworthiness, and for both to correlate with Cat Financial’s portfolio metrics. Interestingly, that is not what we saw in the 2015 10-K.

Dubious Allowance For Credit Losses: The allowance for credit losses is down, but this is largely because CAT changed the calculation in 3Q 15 (reviewed here http://app.hedgeye.com/feed_items/47347). From the 10-K “The decrease in allowance rate is primarily a result of changes in our estimate of the loss emergence period and loss given default.” As we see it, allowance is not sequentially comparable; such historically low reserve levels in the present environment seem dubious at best.

Write-Offs Somewhat Elevated: We would also note that 2H 15 saw a modest increase in write-offs, which help can improve other portfolio measures by removing troubled loans.

91+ Days Past Due Looks Better: The past due payments improved sequentially, which is a noteworthy positive. While higher write-offs help, it is a surprising trend relative to our expectation.

Regional Data Mixed: Latin America & Europe were worse year-on-year, but North America and Asia/Pacific improved.

Total Past Due Also Improved: While partly from larger write-offs, total past due also improved sequentially and YoY.

Non-Accrual Status: The year over year increase decelerated, albeit on a smaller portfolio.

Skip Payments & Consigning Negative Equity Equipment

Perhaps Just Delayed: We would note that Cat Financial generally offers the option to skip payments: “Skip payment plans (up to 3 per year) are available on monthly payment schedules”*, and the ability to offset negative equity in specific equipment with positive equity in a customer fleet. That said, these factors were also true a year ago.

*https://www.catfinancial.com/en_US/solutions/finance/loan.html

Keeping Used Prices High & The Role Of Captive Finance Subsidiary

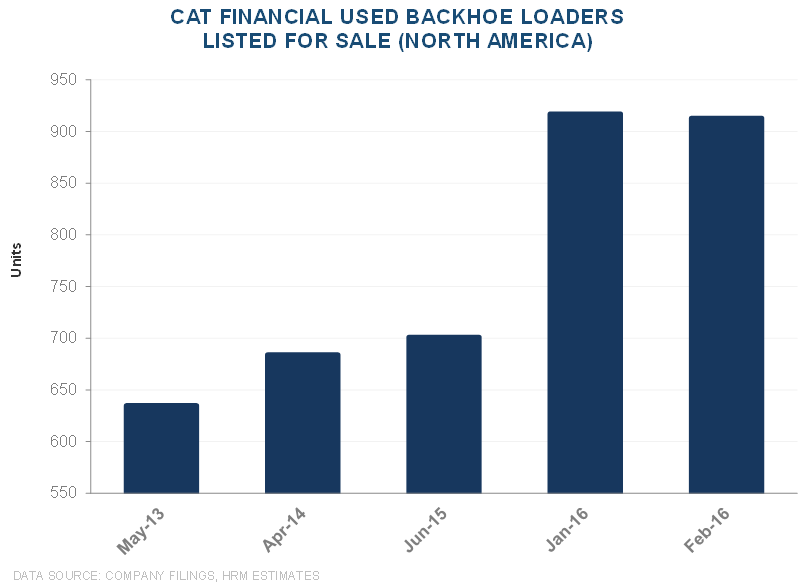

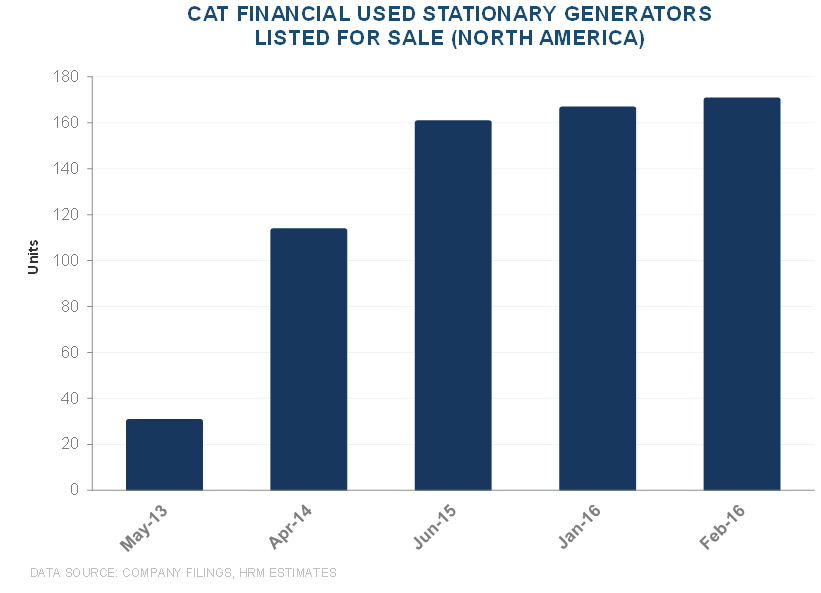

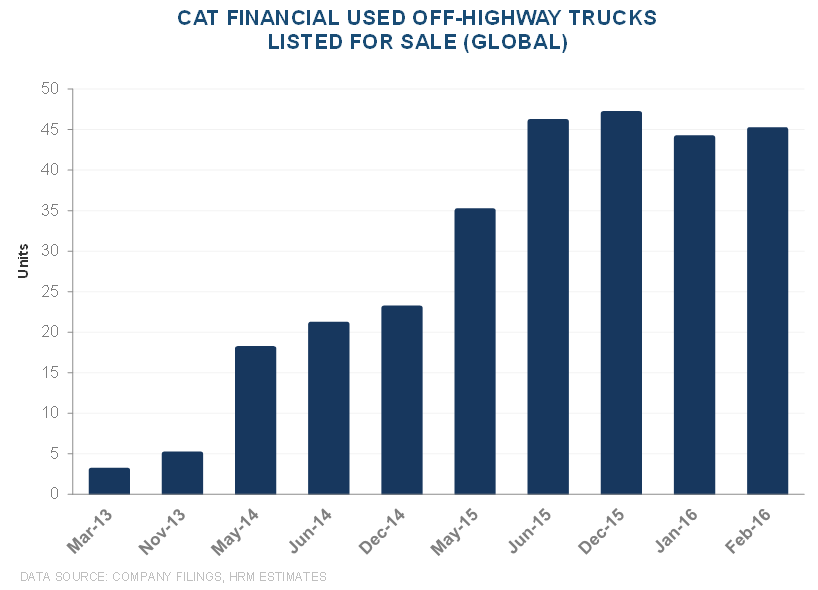

Accumulating Equipment For Sale (Charts Below): As we have previously noted, used equipment appears to be piling up at CAT Dealers. Equipment counts and sale durations do suggest to us that CAT is trying to hold prices up in the aftermarket. Critically, only about 10% of CAT machines are sold by non-CAT auctioneers. Maintaining aftermarket prices is a standard theoretical role for a captive finance subsidiary, partly so used equipment doesn’t compete with new sales. In the face of prolonged end-market downswings, these efforts can prove costly.

Auction Results vs. Cat Asking Prices: Comparing used mining trucks is a bit difficult given specific features, rebuilds, and maintenance histories, but we do not see auction prices that in any way correspond to the asking prices on the CAT Used website. For example, CAT Used lists the price of a 1999 785C with 61,823 hours (although some zero hour components) at $1,350,000. That mining truck has been offered at that price in Winchester, VA since at least 2014, when demand for mining equipment was stronger. Given the coal/mineral mining capital spending environment, it would seem that the likelihood of remarketing the truck at all is low, let alone at a 2014 price. Looking at Ritchie Bros. auction results, a 2005 785C with 36,759 hours sold for $105,000 in April 2015. Even since then mining equipment demand has weakened. Similar comparisons show up for many of the rock/off-highway trucks on the CAT Used site – this one is no way unique.

Raises A Number Of Questions: How is collateral valued if equipment doesn’t receive a bid? Is this the reason Cat Financial dropped the word “liquidation” from the recent 10-K? Where would used equipment values settle if Cat wanted to sell more quickly? How does it make sense to, presumably, shorten the loss emergence period when equipment is accumulating and lingering?

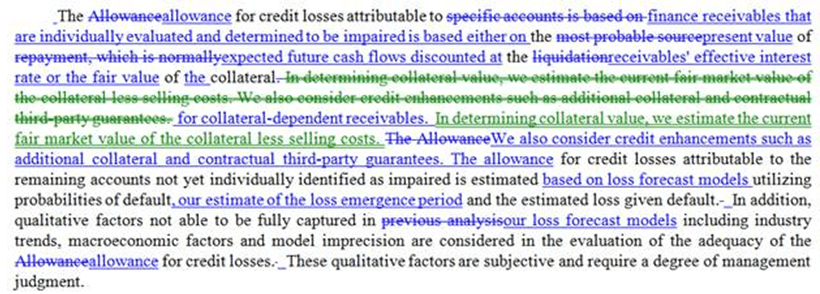

Liquidation vs. Fair Value: We questioned CAT management on a seemingly important language change in the 2015 10-K. The allowance for credit losses on receivables that merit individual evaluation switched from consideration of “liquidation of collateral” to the PV of effective interest or the “fair value”. In the context of unsold equipment, the change seemed material to us. When queried, Cat Financial responded with: “The disclosure regarding methodology of allowance for credit losses attributable to specifically evaluated finance receivables does not represent a change in methodology but rather additional disclosure of the methods that we use for evaluation. The methods disclosed in 2015 are standard practice under US GAAP for evaluating impairment of finance receivables.” Presumably, then, Cat Financial has already been using fair value… The word “liquidation” was removed from the filing.

Accumulating Used Equipment In Cat Channel

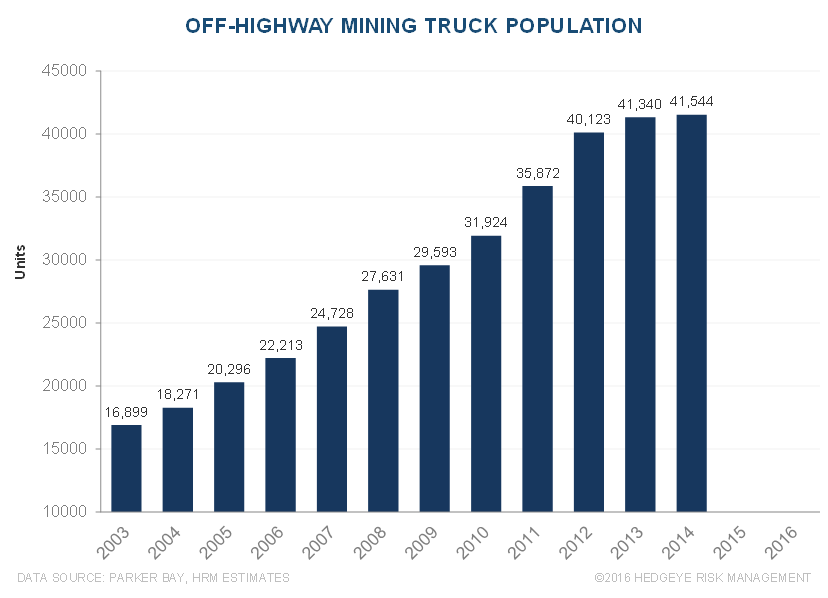

Closures, Bankruptcies Still Coming: As we understand it (see here for call with Michael Currie http://app.hedgeye.com/feed_items/47572), mines will start to move from idling to closures this year. Permanent closures, which mostly have been avoided so far, should involve significant equipment liquidations. Oil & gas hedges will also expire, creating further pressure in an increasingly saturated used equipment market.

Upshot: While Cat Financial’s year-end credit metrics were better than our expectations, we still expect an impact from lower equipment values and increasingly stressed customers. The Cat Channel appears to be holding units off the market with unrealistic pricing. Borrower flexibilities with respect to negative equity and skip payment options may be forestalling the eventual impact of weaker end-markets. Of course, we may also be misreading Cat Financial’s exposures and are continuing a dialogue with management. While we will not dismiss the disconfirming evidence of favorable portfolio metrics lightly, we still expect an eventual negative impact from pending mine closures, oil & gas bankruptcies, and equipment auctions.