So... the Train Wreck most causal to stocks crashing?

> Earnings <

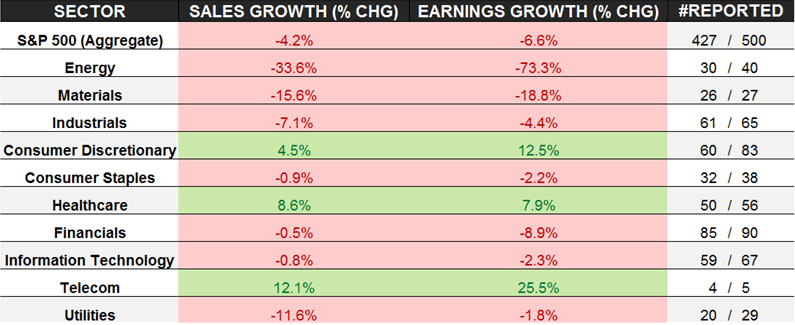

*Note: 7 of 10 S&P Sectors have negative y/y earnings - the narrative that its all Energy = lie

A question every investor should have the answer to right now:

Here's where we're at on the Old Wall: Ex-out whatever doesn't fit your narrative - high quality journalism.

And here's the year-to-date reality.

We've been clear as crystal about what we think: Markets are headed for a crash. (Watch the video below.)

Sure, ex-financials the Dow Bro isn't down as much YTD. But that's not risk management. That's fantasy.