“I believe the fundamentals of our economy are strong. Very Strong”

-John McCain during his run for President, 6/5/2008 (please enjoy the epic #timestamp on that assertion)

I once got beat up in a parking lot in Iowa on the 4th of July by a bunch of racist white kids … for being white.

I was the only white kid on our AAU basketball team and, apparently, in an acute bout of misguided ideology, beating up the lone Caucasian for his chosen associations probably seemed like a better option than taking on a whole team.

Misguided … and miscalculated. #RealTeams don’t divide across racial, socio-economic or any other lines and “lone white kid” ≠ alone.

The Iowan boys got a bigger fight than they were looking for. It didn’t end well for them.

Cross-walking that experience to a metaphor around misguided policy ideology and a potential end game for markets as the belief system around it crumbles is almost too obvious so I’ll just let it hang there in pregnant pause for a moment…

Back to the Global Macro Grind …

Interpretation and contextualization of macro data is duration specific and very much sensitive to the level of zoom.

Some argue that smaller-scale, short-term distortions in the reported data don’t matter.

Others argue that perception = reality, so “optics” are relevant and to the extent some meaningful percentage of market participants are unaware of existent underlying distortions, that collective ignorance – right or wrong – carries real consequences for market prices.

The reality is that both camps are probably right. And, again, it’s largely a matter of duration specificity.

To make this more tangible, consider the most significant recent example of pervasive, recurrent distortions in the reported domestic econ data. A phenomenon we previously termed “Lehman’s Ghost” that permeated through the fundamental data from 2009-14.

To review: Seasonal distortions became ubiquitous across the reported domestic macro data following the Great Recession as accelerated employment loss and the collapse in economic activity were, at least in part, captured as seasonal variation rather than as a bonafide shock.

Because many government statistical models use a 5-year look back to calibrate seasonal adjustments, that distortion echoed forward. The net effect was that seasonal adjustments acted as a tailwind augmenting the underlying data from September – February while reversing to a headwind depressing the reported, seasonally-adjusted data over the March-August period.

That shifting seasonality was perhaps most visible in the initial claims and NFP numbers but the impacts were pervasive with the reported macro data, equity market performance, investor sentiment and analyst estimates all following a similar annual, temporal pattern.

Neither were policy makers immune to the optical mischief of the distortion. Was it completely incidental that every QE initiative was announced in the Sept-Nov period in the wake of the peak negative impact of that distortion?

Back to the present: Due to severe weather in February of each of the last two years and the BEA’s attempt to resolve “residual seasonality” problems in the 1st-quarter data (recall: GDP was negative in the 1st quarter in 3 of the last 5 years), there’s a good chance seasonal adjustments serve to upwardly bias the reported macro data for February. Any prospective distortion will be nothing like the magnitude of “Lehman’s Ghost” but it’s worth a highlight.

At the same time, easier comps beginning in February will also act as a support to reported growth. Recall, Durable Goods, Capital Goods Orders and PPI growth (to name a few) all went negative in February of last year and have languished since. On CPI, where we’ll get the January update this morning, the energy price collapse saw its largest acceleration to the downside in Jan/Feb of last year, driving the easiest rate of change comps in both headline and core consumer inflation.

So, the hereto recessionary macro data looks set to collide with some interesting statistical/comp dynamics in the coming month(s). What do you do with that?

Rocks & Hard Places: Fortunately, the medium-term investment implications are largely the same under the competing scenarios.

- If the data continues to deteriorate, in spite of favorable seasonal and comp dynamics, lower-and-slower-for-longer and its associated allocations continue to work.

- If the data gets an optical boost – edifying policy makers conviction around their hawkish lean - we’d expect the further attempts at policy normalization to perpetuate the same deflationary and growth prohibitive forces that have characterized the last 8-months.

While the ultimate destination is the same under either scenario, the shorter-term investment path would probably be variant. Specifically, in the 2nd scenario, you’d likely see us get more active in risk managing the markets attempt at front-running the policy implications of the reported data for a data reliant Fed.

I was hoping to update our bearish view on housing a bit this morning but the macro musing above surreptitiously hijacked my time allotment.

I’ll probably provide that update next time but the punchline on the recent data is this: Less good is bad and the data flow across housing continues to weaken on the margin.

To close, I’ll leave you with our new colleague, former Fed Vice Chairman and Potomac Research Group Senior Economic Strategist Don Kohn’s, insider contextualization of the “increasing downside risks” reported in the latest Fed Minutes:

“In Fedspeak, downside risks often mean "I think I probably should lower my forecast."”

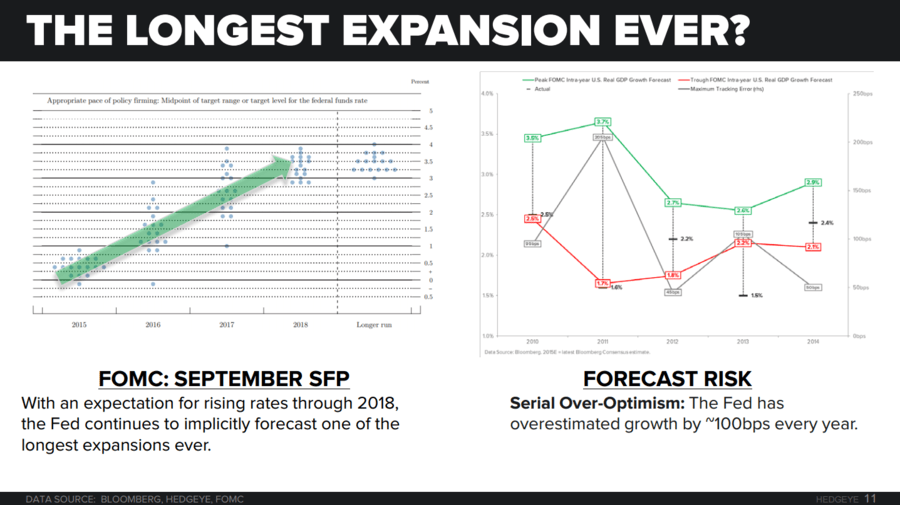

Policy makers have serially overestimated growth by ~100bps (i.e. by ~50% with growth only averaging ~2%) every year over the last half-decade (see Chart of the Day below).

Conspicuous forecast error is the post-crisis norm but how can policy be successfully normal-ized or calibrated with normal, conventional models that fail to fit the new, less Panglossian empirical normal?

Policy makers are smart and well intentioned and villainizing them is partly a literary tool. After all, to invoke emotion and elevate myself to macro protagonist one needs a ready and capable antagonist … but that doesn’t change the realities highlighted above.

For now, proactively front-running Fed forecast error, its policy implications and flow through impact to prices remains alpha’s new normal.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.61-1.86%

SPX 1811-1937

RUT

VIX 21.06-29.01

Oil (WTI) 26.01-33.02

Good luck out there today.

Christian B. Drake

U.S. Macro Analyst