Editor's Note: This is an excerpt from a research note sent to subscribers on Thursday. For more information on our institutional research please email sales@hedgeye.com.

This week we want to take a step back from the high frequency claims data and take stock of where we are in the cycle, and consider what policy tools the Fed has at its disposal.

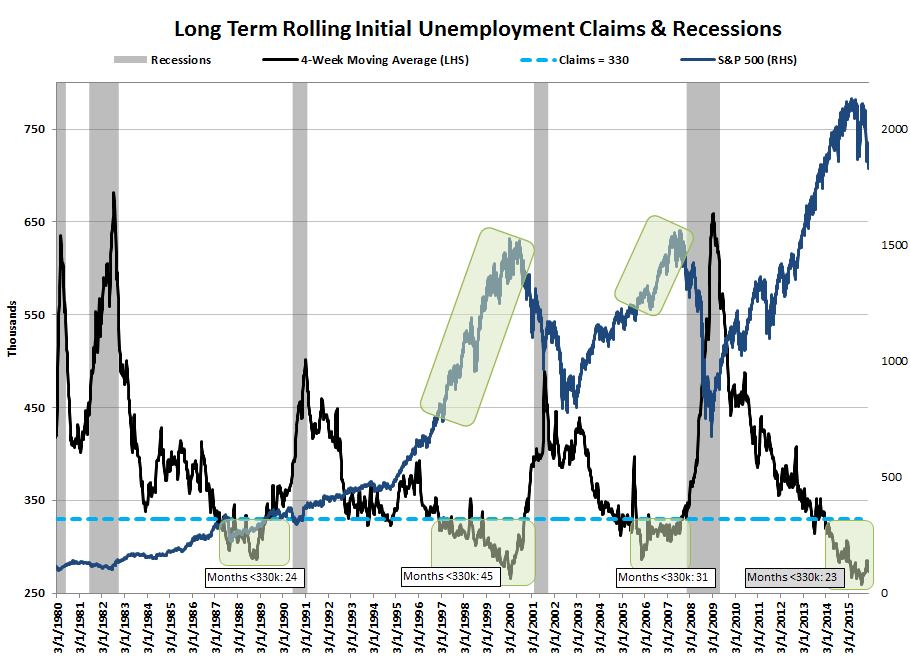

Where are we in the cycle?

As the chart below shows, we're now in month 23 of initial jobless claims running at a sub-330k level. The last 3 cycles have seen the expansion last 24, 45 and 31 months at a sub-330k level, with an average of 33 months. Coupled with the slew of weak economic data coming from the industrial/manufacturing/energy side of the economy, we think it's a better than bad bet that economic contraction isn't far away.

What can the Fed do about it?

We think the cycle being late warrants asking the question: What can the Fed do?

The table below shows that the Fed's average response to the past seven recessions has been a -750 bps rate cut. However, it is facing a significant shortfall in its accommodative ability with the Fed Funds rate currently sitting at around 0.36%. In other words, it's one and done to get back to zero, and then it's QE or NIRP. As we show at the end of this note, the yield spread is already at a post-crisis low (108 bps), which is ratcheting up the pain for banks. 2016 was supposed to be the year when this pressure finally turned tailwind, but instead it's increasingly looking like the opposite is the most probable course for 2016 and beyond.