Without great media fanfare stateside, the European Commission (EC) issued two important statements last week concerning taxation:

1. Called out Belgium for its "excess profit" scheme that gives preferential tax treatment to multinational corporations

2. Issued updated rules to align the tax laws in all 28 EU countries in order to “fight aggressive tax practices by large companies”.

For investors with exposure to multinational corporations in Europe that may have been receiving favorable tax packages, the impact from the new Anti Tax Avoidance Package could have significant consequence. Below we briefly review the background of preferential taxation for multinationals in Europe and discuss the implications of the newest changes.

Background: Countries throughout the EU have incorporated different tax schemes to encourage multinationals to domicile and do business in their borders for many years. Competitiveness has become an increasingly important issue for member states since the Eurozone was hit by the fallout of the global economic recession and the Eurozone ‘crisis,’ beginning with issues around Greece’s sovereign credit rating that was first called into question around 2008.

Since then, the proverbial periphery (Greece, Spain, Italy, Portugal and Ireland) in particular was asked to implement austerity measures, which translated into freezing spending and balancing their budgets to produce surpluses. They also enacted market reforms to make themselves more competitive — simplifying tax codes, opening up markets to foreign investment, lowering wages, slashing welfare, and giving less protection to workers so it was easier to fire them.

What specifically was carried out varies across states, but what’s notable is that multinational companies across many member states received preferential tax treatment and selective subsidy compared with other companies.

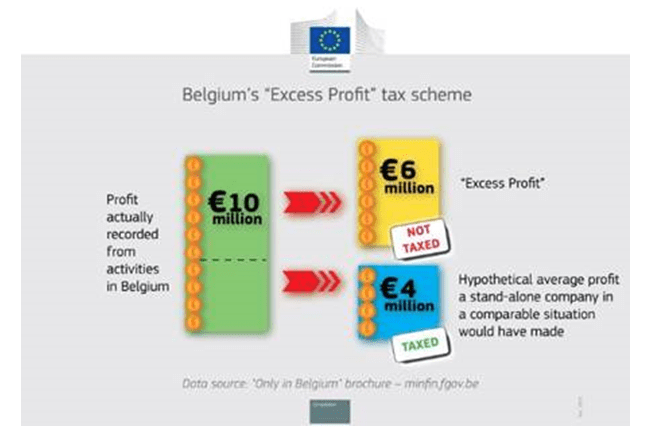

Belgium is Flagged: Last week the EC called out Belgium for its "excess profit" scheme (which has been in place since 2005) that gives preferential tax treatment to its multinational corporations. Specifically, the EC called on Belgium to recoup approximately €700 million in owed taxes from 35 multinational companies. Of those companies the list includes the likes of Anheuser-Busch Inbev and British American Tobacco.

The “excess profit” scheme allows multinationals to discount profits that stem from the benefits of being a multinational, including cost synergies or reputation, from their tax bill. The image below reproduced from the EC shows, in very basic terms, just how favorable the scheme is for multinationals over non-multinationals, which did not get to participate in the excess profit scheme.

For reference, the Belgian Government is considering appealing this decision.

EC Leveling the Playing Field: Beginning in 2015, the EC reports that it began using new investigative tools, including broader tax transparency sharing across the member states (introduced by Regulation 734/2013) to determine which countries are/aren’t in fair tax compliance in its quest to level the business “competitiveness” playing field across member countries and for large and small business alike.

Belgium joins Ireland, the Netherlands and Luxembourg, all of which that have been investigated (and continue to be) by the EC for their tax structures with multinationals.

The EC decided in October 2015 that Luxembourg and the Netherlands have granted selective tax advantages to Fiat and Starbucks, respectively. And the EC has three ongoing investigations into tax concerns regarding Apple in Ireland, and Amazon and McDonald's in Luxembourg.

This follows an announcement two weeks ago that Google agree to pay £130 million in back taxes owed in the UK.

Broader Implications: In updated statements last week the EC submitted a new Anti Tax Avoidance Package (to be signed off by the member states), which amounts to updated language and frameworks to police and level the tax playing field across the entire 28 member through increased transparency.

One line that jumped out to us: “There is no attempt to interfere with countries' sovereign right to decide their own corporate tax rates. However, countries also have a right to protect their tax bases against aggressive tax planning and unfair tax competition.”

Essentially the new measures intend to focus most on leveling the tax playing field within a country between a multinational and all other large and small business, however it appears that the door has been left open for tax “haven” countries (those who with a lower corporate tax rate vs other member states intend to attract foreign business to their borders) who also could be compliant with the EC’s tax standards.

We suspect that all member states will be reviewed for their tax structures in the coming months and years. Just which countries are up next on the block is hard to say. Ireland, Netherlands, and Luxembourg were countries that had particular “reputations” as notable tax havens (with preferential treatment) within the EU.

With “competitiveness” at the sovereign level an ever hot topic, we’ll continue to update you as we learn more about the EC’s reach across the member states.