It goes without saying that this is one of the more polarizing quarters for Amazon in quite a while. But let’s put aside the stock move for a minute and look at what’s changed fundamentally – after all, with the sell-off the stock is trading about in line with where it was just two days ago.

- The irony with all of this is that the quarter itself was very good. Sales grew by 25%, in its core business – what we’ll call US Retail – 60% of sales (it’s actually North America EGM + Media). This is a BIG plus for those out there that think that AMZN can one day capture 10% of total US Retail Sales. That’s a $500bn number. You may balk at it. We might too. But people believe it, and as long as they do, they’ll hold this stock forever.

- AWS also looked relatively solid. Yes, it decelerated to 69% (from 78% last quarter) but is well above a rate we need to make this model work.

- International is a clear hole we can poke in the quarter, as we saw growth of only 12%. Keep in mind that AMZN has about 33% share of US Online Spending, but only about 8% in its more developed non-US regions. While there’s a big opportunity for AMZN to grow outside our borders – potentially fueling one of the next multi-year legs of growth – it’s not acceptable for a company like this to see Int’l sales go from 45% to 33% over the past economic cycle.

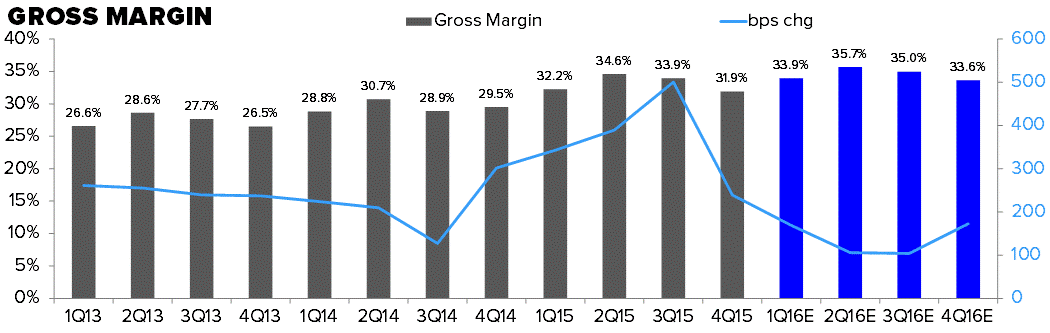

- That brings us to the only thing we’re really concerned about, which is AMZN’s profitability to the extent we are, in fact, headed into a recession. Roughly 65% of its total sales are in the US. At the same time, we just saw gross margin improvement decelerate materially, suggesting tougher GM compares 2-3 quarters out. If we have down gross margins, sales erode on the margin due to the economy, then the only thing that could sustain AMZN’s EBIT line is cuts to SG&A growth. If there’s anything we know (and respect) about AMZN, it’s that the company will spend money how, where, when and on what it so chooses. In fairness, this is a $100+bn revenue company that is producing over 50% returns on incremental cash. From where we sit, Bezos has earned a hall pass to do pretty much whatever he wants (that hall pass can be revoked if returns go the other way).

Hedgeye has a very bearish view on the US economy, so we’re concerned about the guide in another 13 weeks. The SIGMA chart below supports this, as it’s the first time AMZN has been in a negative Sales/Inventory position in seven quarters. Unless estimates come down materially when they hit by the end of the weekend, we’re more on the bearish side from a near-term perspective. Though from a TAIL duration 3-years or less, we still like the story a lot.

Charts include consensus estimates:

Gross Margin expectations remain high.